Autonomous Finance Meets Complex Selling: Why Immutable Audit Trails Are Now Non-Negotiable for CFOs in 2026

In this article: The Boardroom Diagnostic · Why 2026 Made This Existential · Shadow Pricing · The Convergence · What Immutable Audit Trails Means · The Playbook · Why Legacy CPQ Fails · CFO Risk Diagnostic · Where servicePath Fits · Third-Party Proof · FAQ · What To Do Next

Executive Summary

Every CFO has seen the symptoms: margin leakage on renewals nobody can explain. Forecast misses traced back to deals that looked clean in the CRM but fell apart in billing.

Audit friction because nobody can reconstruct how a price was approved. And now, AI tools generating pricing recommendations with zero accountability trail.

In every case, the root cause is the same. Immutable audit trails are missing. Nobody can connect what was configured, priced, and approved to what was ultimately sold.

Consequently, the mistake is treating these as separate problems. They are not.

They usually come from the same upstream failure: when the deal was configured, priced, revised, and approved, nobody preserved a trustworthy record of what happened. Everything after that moment is either evidence or assumption. And finance cannot govern assumption.

However, I have spent nearly a decade deploying CPQ into enterprises that sell complex technology. In fact, every single implementation has uncovered pricing that could not be traced to an approved decision. Every one.

The pattern is always the same. Renewals carry terms nobody can explain. Managers approve discounts verbally but never log them. Reps make configuration changes mid-deal in spreadsheets that never sync back.

The rep who made the original call has moved on. The manager who approved it does not remember.

Speed was never the real problem

I want to be honest about something. When I joined servicePath™ as CEO nearly a decade ago, I thought the problem was speed. Get the quote out faster, win the deal. That is what every CPQ pitch says.

What I learned, deal after deal, customer after customer, is that the real problem was never speed. It was memory. Enterprises do not lose money because quotes are slow. They lose money because nobody can prove what was in the quote, who changed it, or why.

Speed without memory is just faster chaos.

And the faster your AI generates configurations, the faster you create undocumented financial commitments if the system does not preserve every decision along the way.

Our co-founders, Mike Molson and Ian Cross, built servicePath™ on a simple insight. Service providers lacked the tools to adapt to rapid technology and pricing changes. What I brought to that foundation was the finance lens. Every configuration decision is a financial commitment. And every unrecorded decision is a latent liability that immutable audit trails would have prevented.

Most enterprises are building AI-powered revenue engines on sand. This is not a CPQ feature gap. It is a revenue architecture problem. And in 2026, three forces have made it existential.

Daniel Kube is CEO of servicePath™, the sole Visionary in Gartner’s 2026 Magic Quadrant for CPQ Applications. He has spent nearly a decade deploying CPQ into enterprises selling complex technology services. Follow Daniel on LinkedIn.

The Boardroom Diagnostic

Before reading further, answer one question honestly:

Can your organization reconstruct every material pricing decision from quote to contract to revenue recognition, without calling the salesperson who made the deal?

If the answer is no, or “it depends on who you ask,” then every section of this blog describes a risk you are currently carrying. If the answer is yes, you are ahead of most enterprises I work with. Either way, keep reading.

Why 2026 Made This Existential

Your two top priorities are at war with each other

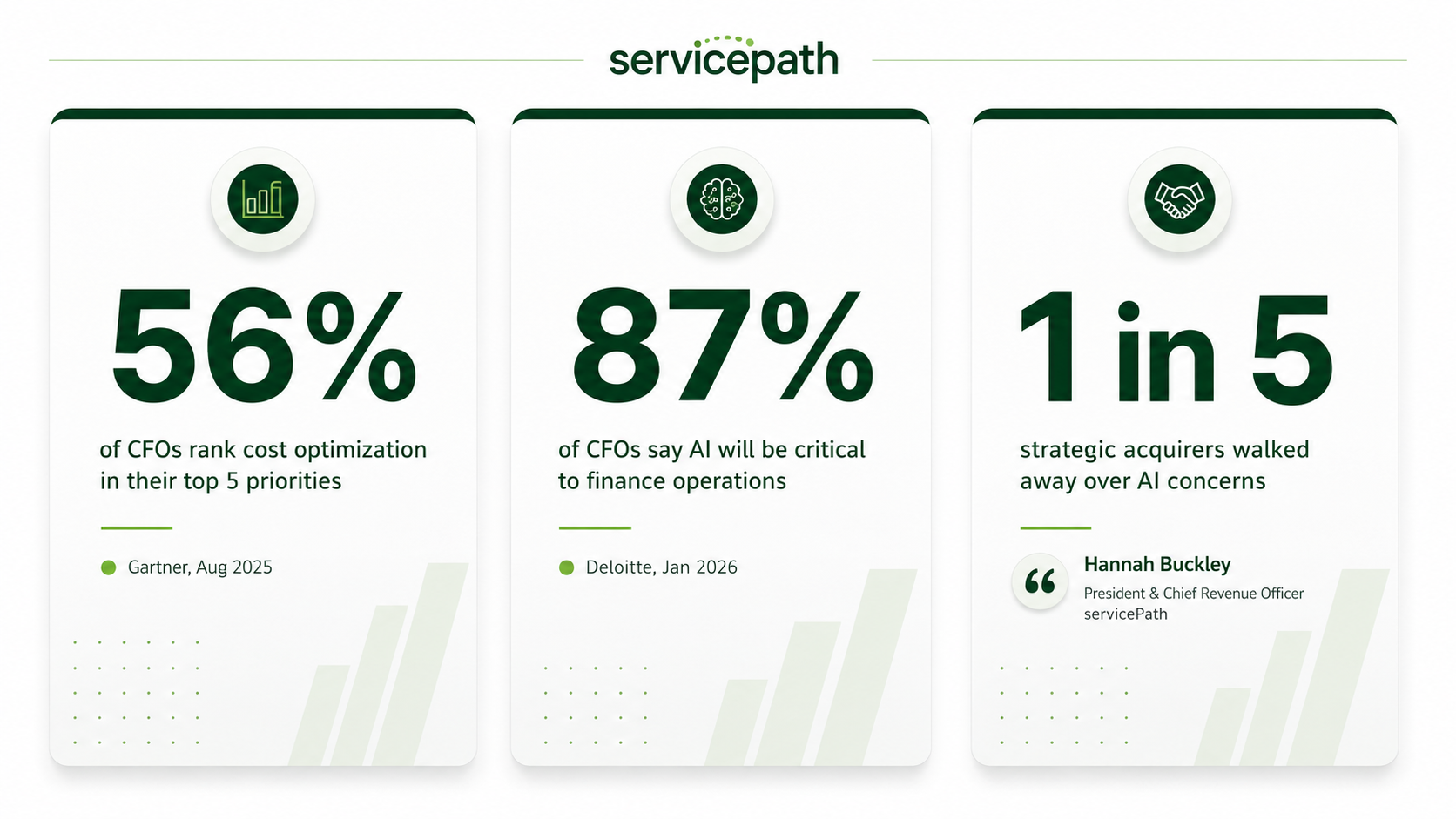

Gartner’s August 2025 CFO survey found that 56% of CFOs rank cost optimization in their top five priorities. Simultaneously, 51% rank forecast accuracy. Those two goals are in direct tension when your deal data is unreliable. Meanwhile, pricing strategies are rising in importance amid economic pressures, making governed deal data even more critical.

Dennis Gannon, VP Analyst at Gartner: “Growth goals are ratcheting up for the year ahead, but the expectation is that CFOs will hold the line on all the cost optimization they’ve done in 2025” (CFO.com, December 2025). You cannot hold a line you cannot trace back to the deal that created it.

“Many CFOs are looking to advanced technologies not only to improve efficiency within finance, but to help their organizations respond more quickly to changing market and customer dynamics. In 2026, uncertainty will likely remain the new normal.” — Steve Gallucci, U.S. leader of Deloitte’s CFO Program (Deloitte Q4 2025 CFO Signals, January 2026)

AI is making decisions nobody can explain

Deloitte’s Q4 2025 CFO Signals found that 87% of CFOs expect AI to be important to finance operations. Moreover, 54% are prioritizing AI agent integration. Yet Gartner found only 36% feel confident they can achieve meaningful AI outcomes. Gartner called it “more of an accountability problem internally” (CFO Brew, December 2025). Without immutable audit trails, that accountability gap only widens.

The 2026 Gartner Hype Cycle for Agentic AI confirms “rising enterprise concern about accountability, control and economic sustainability.”

Consider this scenario. An AI agent suggests a pricing configuration. Nobody records what it recommended, what rules it followed, or whether a human approved it. At that point, you have created a financial commitment with no forensic trail.

“To capture the margin upside, CFOs need to align AI and technology investments to business outcomes, supported by strong governance, explainability and data readiness.” — Mike Helsel, Senior Director Analyst, Gartner Finance Practice (Gartner, April 2026)

(

(

Acquirers are walking away over this

Global M&A reached $4.9 trillion in 2025 according to Bain’s 2026 Global M&A Report. Notably, one in five strategic acquirers walked away from a deal. The reason: concerns about the anticipated impact of AI on the target’s business. In addition, seventy-five percent now assess AI impact during diligence.

As CFGI’s 2026 CFO Outlook put it: “Treat transaction readiness as a standing operating capability.”

In practice, this means that when an acquirer opens your data room and finds deal pricing that cannot be traced to governed approval chains, that is not a footnote. That is a valuation discount or a broken deal.

Specifically, the companies feeling this most acutely are those scaling complex portfolios across Oracle, SAP, and Salesforce ecosystems. Large MSPs integrating hardware, software, services, and usage-based models face the same pressure.

One wrong discount path or untracked configuration change cascades into audit nightmares, delayed closes, and eroded margins. Immutable audit trails in CPQ would catch these failures at the source.

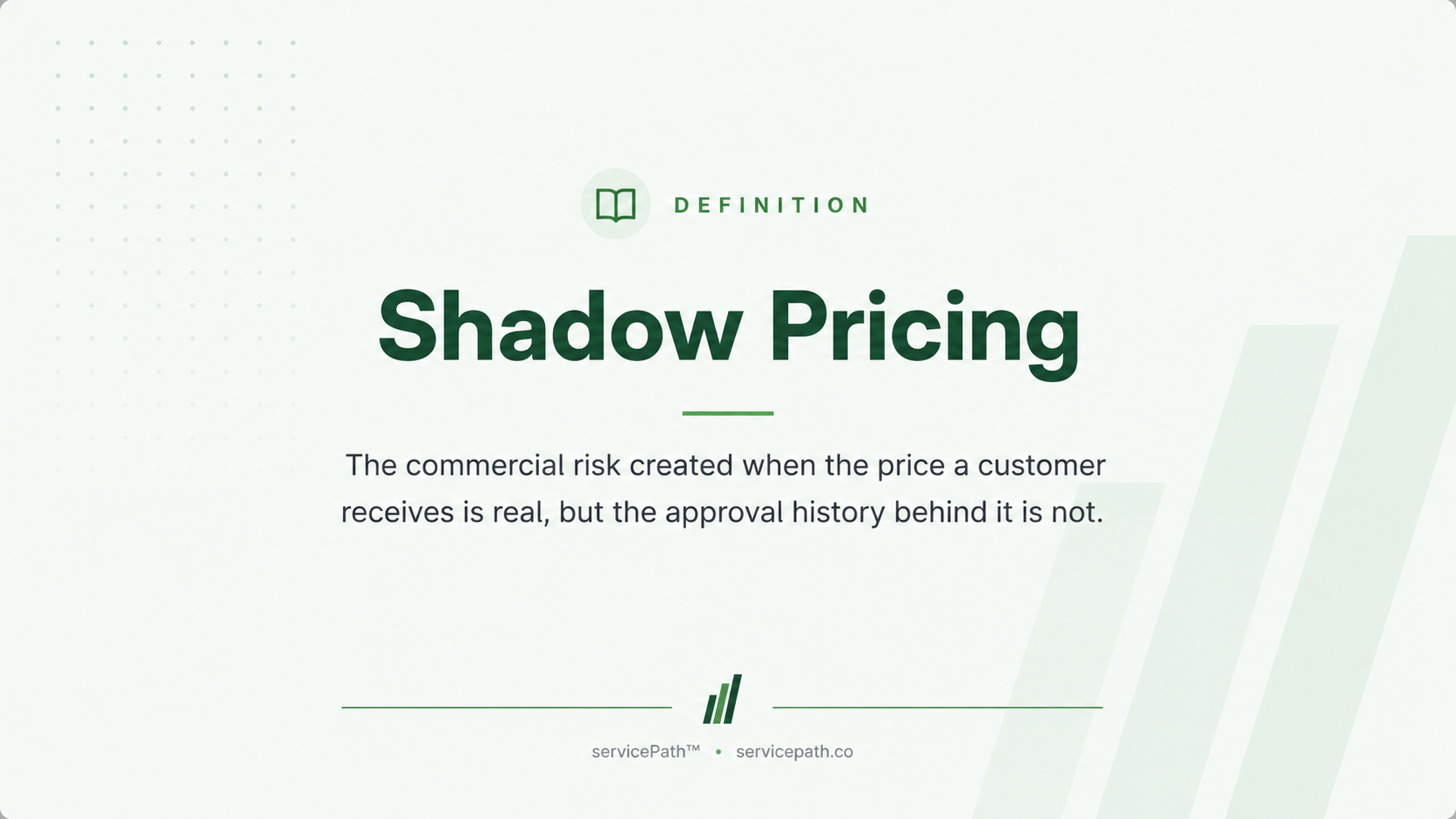

Shadow Pricing: The Risk Your Systems Cannot See

I want to name the specific commercial risk that sits behind all of this: shadow pricing.

Shadow pricing is the commercial risk created when the price a customer receives is real, but the approval history behind it is not.

The $1.2 million renewal nobody could explain

A sales rep is working a $1.2 million managed services renewal. The customer pushes back on pricing. The rep pulls up the original quote in the CRM, but the CRM only shows the final version, not the six iterations that preceded it.

The original discount was 12%. Somewhere during the initial negotiation, it became 18%. Nobody knows who approved the change from 12 to 18, or whether it was even formally approved.

As a result, the rep, under pressure, matches the 18% for the renewal. Finance books the deal at the rate-card margin assumption. The actual margin is six points lower.

Multiply that by a hundred renewals across the portfolio, and you have a margin gap that shows up in the P&L but cannot be diagnosed because the configuration history does not exist.

Not fraud. Not negligence. Just architecture.

That is shadow pricing. Not fraud. Not negligence. Rather, it is the predictable consequence of running a revenue process where deal decisions are made in one system, approved in another, and recorded in neither.

Furthermore, it emerges in predictable ways. A rep models a custom discount in a spreadsheet that gets verbally approved. Nobody records it in the CPQ.

The team processes a renewal at legacy rates because nobody can reconstruct the original deal terms. These are exactly the scenarios immutable audit trails are designed to prevent.

The financial damage

MGI Research puts hard numbers on the downstream damage: revenue leakage exceeding SEC materiality thresholds of 5% of revenue or 10% of EBITDA creates potential ASC 606 violation risk.

But the damage goes deeper. MGI found that when revenue goes unbilled while associated costs are fully recognized, reported gross margins understate economic margins.

Management then raises prices believing margins are inadequate, when true margins already meet targets. Ultimately, you end up solving the wrong problem because the data told the wrong story.

Worse, the gap destroys trust between sales and finance, because neither side can prove its version of what happened.

The compliance chain reaction

Revenue recognition under ASC 606 requires judgment at the contract level: performance obligations, transaction prices, allocation, recognition timing. PwC flags that these decisions “can influence pricing strategy, sales operations, and overall company valuation.”

SOX audits require demonstrable controls. GDPR adds data governance requirements for customer-facing pricing data in European operations. When configurations are not tracked with version history, every one of these judgments becomes an educated guess.

We have explored this further in our posts on CPQ trends for 2026, legacy CPQ risks, and AI governance in revenue processes. The pattern is clear: precision without immutable audit trails is just faster chaos.

The Convergence: One Architecture Problem, Not Four

Here is what I need every CFO reading this to understand: the audit trail gap is not four separate problems. This is one structural failure manifesting in four places simultaneously.

The same missing configuration history that causes margin erosion on renewals is the same gap that creates ASC 606 compliance risk. Equally, that gap lets AI-generated pricing decisions go unrecorded. And an acquirer will find the same gap during diligence. Immutable audit trails close all four gaps at once.

Four budgets solving one problem they cannot see

I have watched companies try to solve these individually. First, they hire a revenue recognition consultant to fix the ASC 606 exposure. Then they bring in an AI governance framework to address agentic risk. Next, they run a margin recovery project to claw back deal leakage. Finally, they clean up the data room for a potential transaction.

Four initiatives. Four budgets. Four timelines. And none of them work, because they are all downstream of the same root cause: the moment a deal was configured and priced, nobody recorded what happened in a form that could be trusted later.

Fix the architecture at the point of deal origination, and you fix all four. Ignore it, and they compound on each other every quarter.

The numbers confirm the gap is widening

Bain’s 2026 B2B Growth Agenda found that 42% of companies missed revenue targets in 2025, up from 32% in 2024. That widening gap is not a sales execution problem. It is a governed-data problem masquerading as a pipeline problem.

“Volatility is now a constant condition for B2B companies, not a temporary disruption. The gap between ambition and performance is widening, and closing it requires faster, more adaptive execution and a fundamentally more responsive commercial system.” — Jamie Cleghorn, Global Head of Bain’s Customer Practice (Bain & Company, March 2026)

(

(

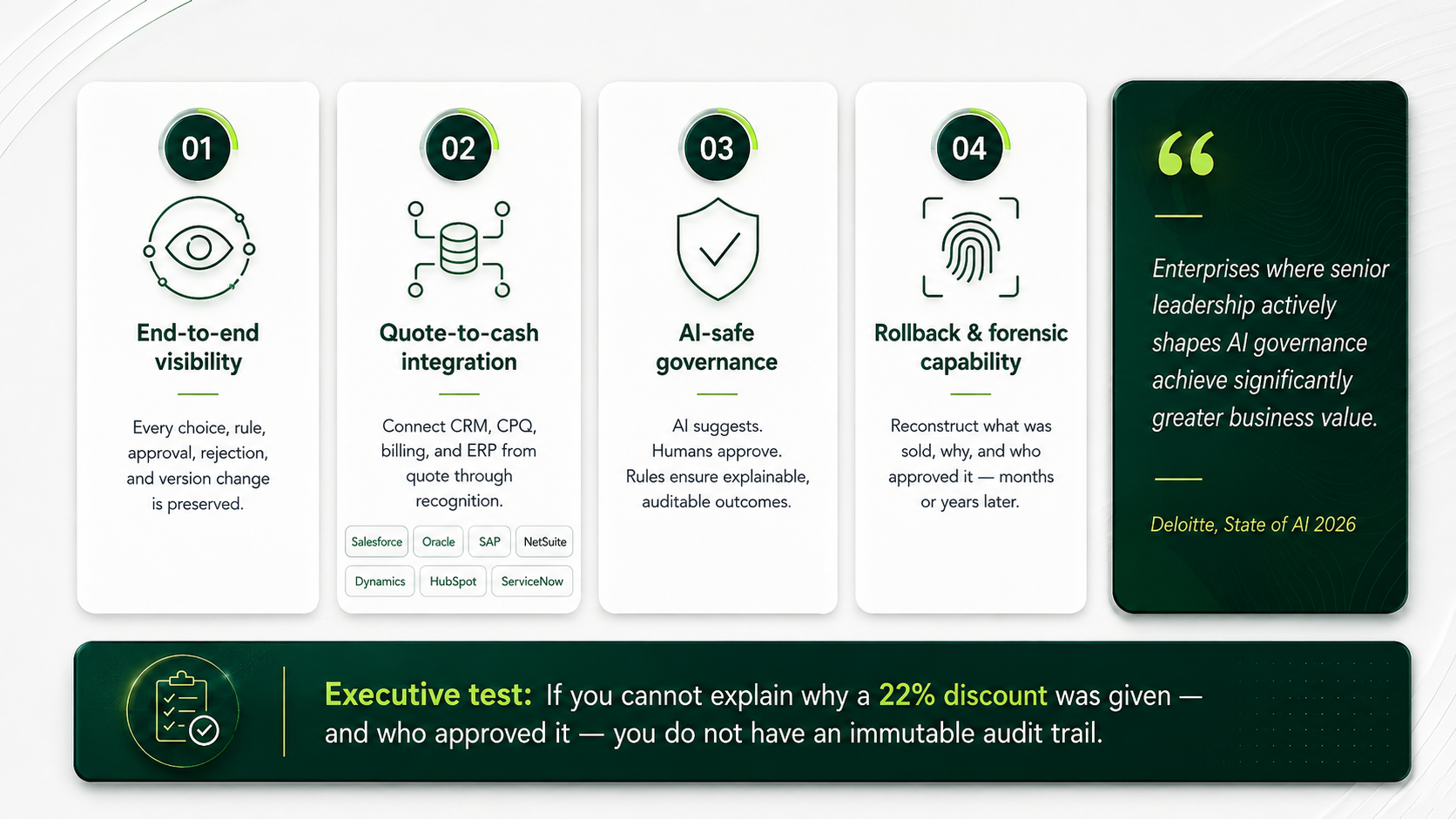

What “Immutable Audit Trails” Actually Means for CPQ

This term gets diluted. It is not a transaction log. Let me be precise.

End-to-end visibility

Every configuration choice, pricing rule application, approval, rejection, and version change, timestamped, user-attributed, preserved. Not just the final quote but the 14 iterations that produced it, including the three that were rejected and why.

Integration across quote-to-cash

The trail flows through CRM, billing, and ERP (Salesforce, Oracle, SAP, NetSuite, Dynamics, HubSpot, ServiceNow), connecting what was configured to what was contracted, invoiced, and recognized. For more on this integration architecture, see our Revenue Engine glossary.

AI-safe governance

Deterministic, rules-based guardrails that produce explainable, auditable outputs even when AI assists. AI suggests. A human approves. The system records both.

Deloitte’s State of AI 2026: “Enterprises where senior leadership actively shapes AI governance achieve significantly greater business value.”

Rollback and forensic capability

Reconstruct exactly what was sold and why, months or years later. If your system cannot answer “why did we give Customer X a 22% discount on this line item in March 2024, and who approved it?” you do not have an immutable audit trail. You have a log file.

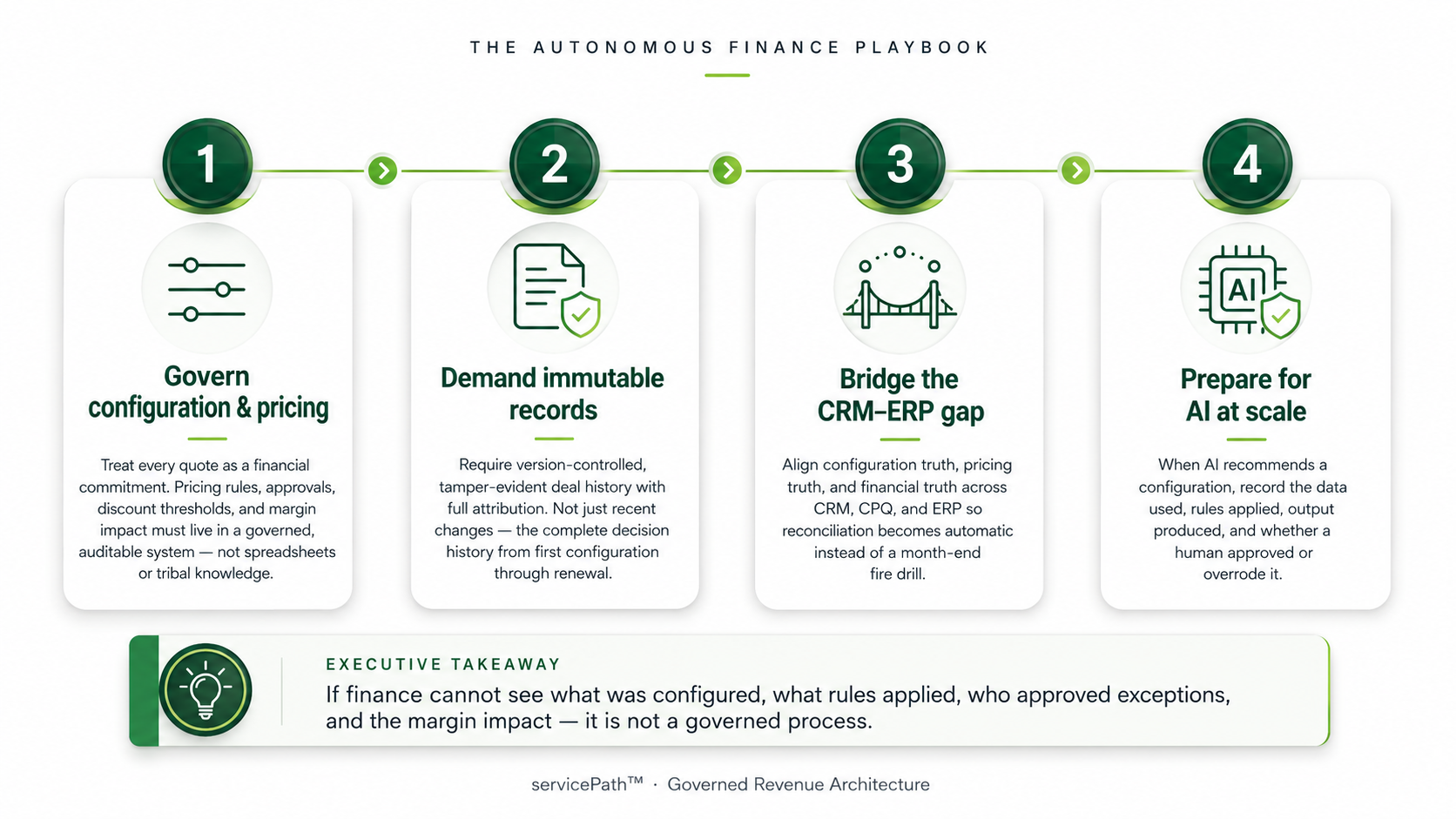

The Playbook: Four Steps to Governed Revenue Architecture

Step 1: Treat configuration and pricing as governed financial processes

Configuration is not a sales activity. It is a financial commitment. Every line item carries cost, margin, revenue recognition, and contractual implications.

As a result, pricing rules, approval workflows, discount thresholds, and product eligibility logic must live in a governed, auditable system.

Not in tribal knowledge. Not in spreadsheets. Not in the heads of senior reps who have “earned the right” to deviate.

I have a simple test I give every CFO I work with: can you walk into your system today and see, for any active deal, exactly what was configured, what pricing rules applied, who approved any exceptions, and what the margin impact is?

If the answer requires calling someone or opening a spreadsheet, you do not have a governed process. You have a trust-based process. And trust does not survive personnel changes, audits, or acquisitions.

Step 2: Demand immutable records as a core architectural requirement

Logging captures events. Immutable records preserve the complete state of a deal at every decision point. There is a difference between “we can see the last five changes” and “we can reconstruct the full decision history of every deal from first configuration through renewal.”

Accordingly, specify this during vendor selection, not implementation. If your CPQ vendor cannot demonstrate version-controlled, tamper-evident deal histories with full attribution, that is a disqualifying gap, not a roadmap item.

Step 3: Bridge sales and finance systems with shared truth

The most common architectural failure I encounter is what I call the “CRM-ERP gap.” Sales commits a deal in CRM. Finance recognizes revenue in ERP. Nobody can reconcile the two.

The reason is straightforward: the configuration details that determine revenue treatment never made it from one system to the other intact. Immutable audit trails in the CPQ layer bridge this gap.

Therefore, the bridge is not an integration project. It is an architectural commitment where configuration truth, pricing truth, and financial truth are the same truth. When those three are aligned, reconciliation stops being a month-end fire drill and starts being automatic.

Bain’s pricing projects typically boost margins by 415 basis points. But that precision requires governed data flowing from quote through cash. Without it, dynamic pricing becomes dynamic risk.

Step 4: Prepare for AI at scale

Gartner predicts 90% of finance functions will deploy at least one AI-enabled solution by end of 2026. When an AI agent recommends a configuration, the system must record what data it consumed, what rules it applied, what it produced, and whether a human approved or overrode it.

Above all, the question is not whether AI will touch your revenue process. It is whether you will be able to explain what it did when an auditor, an acquirer, or a board member asks. If the answer is “we would need to check,” you have already lost the argument.

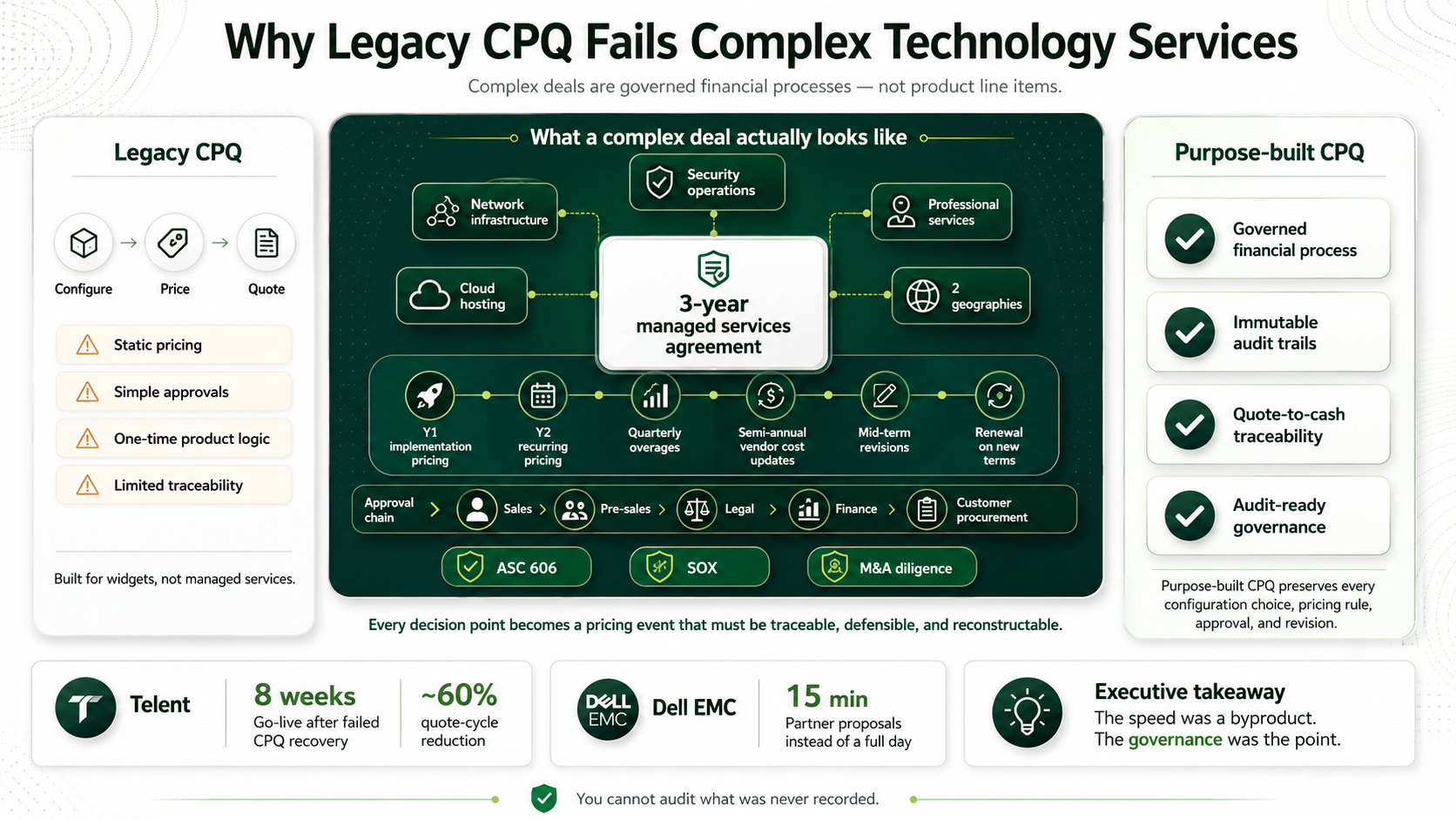

Why Legacy CPQ Fails Complex Technology Services

Most CPQ platforms were built for product-centric sales: configure a widget, price it, quote it. However, that model breaks for managed services, cloud, SaaS, and hybrid technology portfolios.

In these environments, the “product” is a multi-year service commitment. It includes usage-based components, mid-term revisions, co-termination logic, vendor cost pass-throughs, and margin structures that vary by region, channel, and customer tier.

What a complex deal actually looks like

For example, consider a three-year managed services agreement bundling network infrastructure, cloud hosting, security operations, and professional services across two geographies.

Year 1 implementation pricing transitions to recurring operational pricing in Year 2. Usage-based overages are billed quarterly. Vendor costs update semi-annually.

The approval chain touches sales, pre-sales engineering, legal, finance, and the customer’s procurement team. That deal will be revised mid-term at least twice. It will renew with different terms.

Consequently, every one of those decision points creates a pricing event. That event must be traceable under ASC 606, defensible under SOX, and reconstructable during M&A diligence.

A product-centric CPQ treats that as a line item. By contrast, a purpose-built CPQ treats it as a governed financial process with immutable audit trails at every stage.

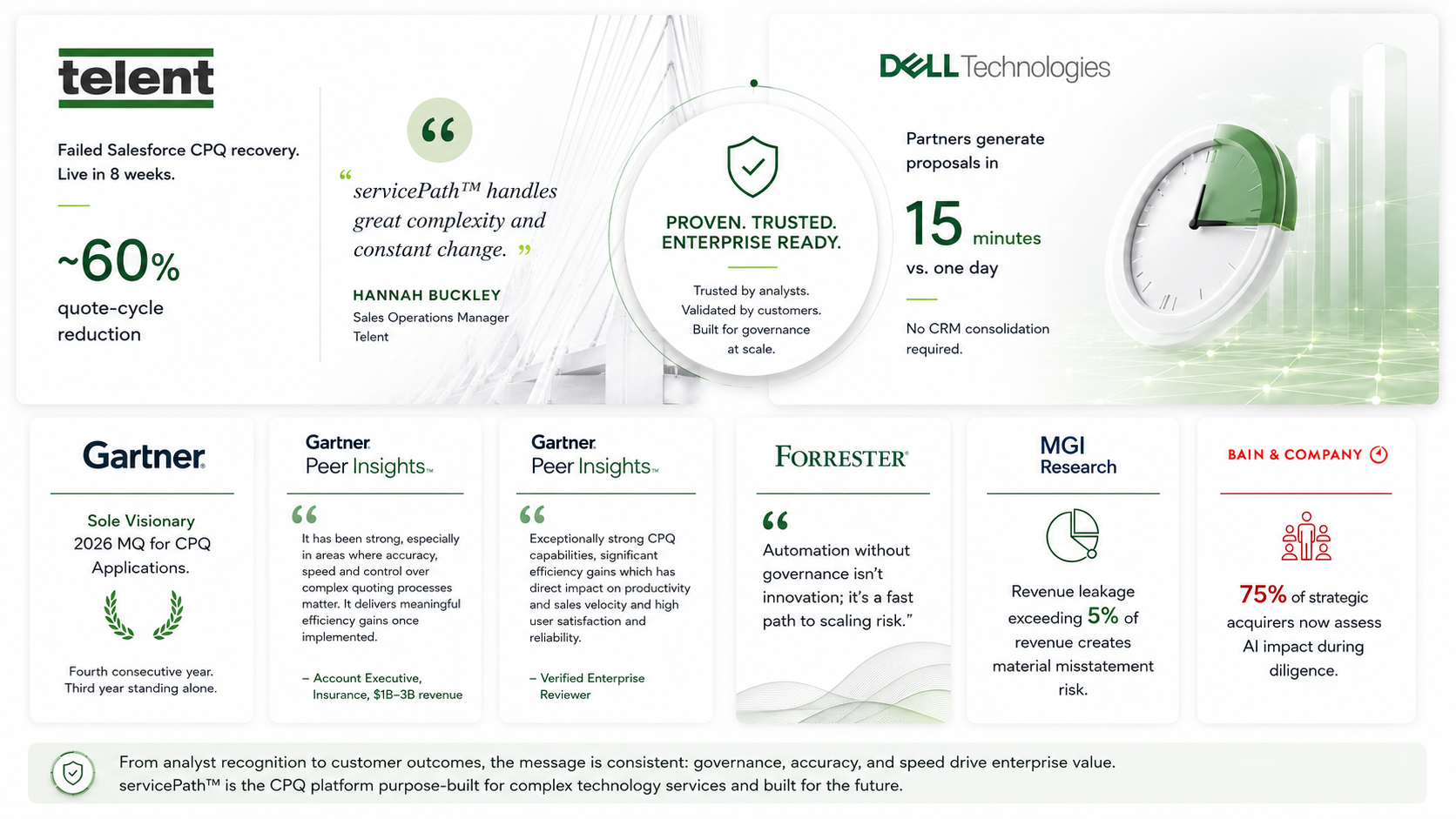

What Telent and Dell EMC discovered

When Telent came to us, they were recovering from a failed CPQ implementation and quoting from spreadsheets. Hannah Buckley, their Sales Operations Manager: “a huge challenge is constant change in technology and pricing. Most CPQ solutions are built for simpler environments and are not engineered to account for this rate of adjustments.”

Telent went live with servicePath™ in 8 weeks with approximately 60% quote-cycle reduction.

For context, the cost of a governed CPQ implementation is typically a fraction of one quarter’s margin leakage from ungoverned pricing. Dell EMC transformed their partner ecosystem so partners generated proposals in 15 minutes instead of a day, without requiring CRM standardization.

The speed was a byproduct. The governance was the point.

I want to be direct about what those outcomes actually represent, because the numbers alone do not tell the full story. In Telent’s case, the speed improvement was secondary to the governance improvement.

Before servicePath™, Telent had no way to trace a pricing decision back to its origin once a deal moved past the quote stage. After go-live, every configuration choice, every pricing rule, every approval, and every revision was preserved and attributable. The speed was a byproduct of having the right architecture. The governance was the point.

Every implementation we have done in nearly a decade has uncovered pricing that could not be traced to an approved decision. Every one. The CFO’s role is shifting to what Workday calls “decision-auditor”: ensuring governance frameworks validate AI outputs and maintain accountability. You cannot audit what was never recorded.

The CFO Risk Diagnostic

Where servicePath™ Fits

servicePath™ is the sole Visionary in Gartner’s 2026 Magic Quadrant for CPQ Applications, marking the fourth consecutive year in the Visionary quadrant and the third year standing alone out of 16 vendors evaluated.

It exists because most of the CPQ market was built for product companies, and organizations selling managed services, SaaS, telecom, field services, financial services, and XaaS needed something architecturally different.

servicePath™ pioneered RIAC (Revenue-IT Architecture Convergence): pricing orchestration across multiple CRMs without forcing consolidation.

AI within deterministic guardrails. Service Contracts with complete lifecycle audit trails. Codeless configuration. Dell EMC, Telent, TierPoint, Park Place Technologies, Telefonica in production. Salesforce has ended sale of legacy CPQ and 6,000+ organizations face architecture decisions.

Where servicePath™ may not fit

servicePath™ is not the right choice if you sell simple product-centric SKUs with flat pricing and no service component. Companies that need CPQ natively embedded inside Salesforce with zero external architecture should look elsewhere (servicePath™ integrates with Salesforce via its cloud-based Multi-CRM Adapter, syncing data bidirectionally while operating as an independent orchestration layer.

Sellers work inside their CRM; servicePath™ enforces pricing rules, governance, and audit trails across all instances). Similarly, when deal complexity is low and quoting volume is the primary concern, lighter tools may fit better. The same applies when you have no CRM and need a combined CRM-CPQ

Third-Party Proof

Gartner: Sole Visionary, 2026 MQ for CPQ Applications. Fourth consecutive year. Third year standing alone.

Gartner Peer Insights (Feb 2026): “It has been strong, especially in areas where accuracy, speed and control over complex quoting processes matter. It delivers meaningful efficiency gains once implemented.” — Account Executive, Insurance, $1B-3B revenue

Gartner Peer Insights: “Exceptionally strong CPQ capabilities, significant efficiency gains which has direct impact on productivity and sales velocity and high user satisfaction and reliability.” — Verified Enterprise Reviewer

Telent: Failed Salesforce CPQ recovery. Live in 8 weeks. ~60% quote-cycle reduction. Hannah Buckley: “servicePath™ handles great complexity and constant change.”

Dell EMC: Partners generate proposals in 15 minutes vs one day. No CRM consolidation required.

Forrester Q2 2026: “Automation without governance isn’t innovation; it’s a fast path to scaling risk.”

MGI Research: Revenue leakage exceeding 5% of revenue creates material misstatement risk.

Bain 2026 M&A Report: 75% of strategic acquirers now assess AI impact during diligence.

Frequently Asked Questions

Why are immutable audit trails specifically important for complex technology services?

Because the deals are not static. A managed services contract undergoes mid-term revisions, vendor cost changes, usage true-ups, and renewal negotiations over multiple years. Each change creates a pricing decision that must be traceable.

Under ASC 606, allocating transaction prices across performance obligations requires knowing what was configured at what standalone selling price. Without that history, revenue recognition becomes guesswork. Guesswork at scale is how restatement risk accumulates silently.

Can AI-driven pricing be auditable?

Only within a deterministic framework. The key principle: AI suggests, humans decide, the system records both.

Forrester: “success depends less on algorithms and more on process discipline and trusted data.” If you cannot reproduce the reasoning behind an AI-recommended price six months later, you have a suggestion engine with no memory, not an auditable system.

What should we evaluate first if migrating off Salesforce CPQ?

In short, architecture, not features. The question is whether your next CPQ is a CRM plugin or an independent orchestration layer.

If you run multiple CRMs, plan acquisitions, or sell complex services with margin governance requirements, you need a platform that sits above any single CRM instance. The migration is the moment of maximum leverage. Do not waste it on a lateral move.

The Bottom Line

Gartner’s “Autonomous Finance” vision for 2026 is not about removing humans from finance. It is about giving finance teams trustworthy data infrastructure to make faster, better decisions. That infrastructure starts at the moment of configuration: the instant a rep selects a product, applies a price, and requests approval.

Complex selling will only get more complex. AI will not simplify it. It will accelerate it. The winners will be those who impose precision and unbreakable visibility now, at the point where revenue originates: the deal. Not downstream. Not in reconciliation. Not in a quarterly cleanup exercise. At the moment the commitment is made.

I have said this to hundreds of CFOs over nearly a decade, and it has never been more true than it is right now: every signed quote is a financial promise. If you cannot prove how that promise was constructed, you cannot govern the revenue it creates.

What To Do Next

Book a Revenue Architecture Diagnostic — Bring us one complex quote, one renewal, and one exception approval path. In 30 minutes, we will show you whether your revenue process is built on evidence or assumption.

Read Our Case Studies — See how enterprises like Telent, Dell EMC, and Scanco solved the governance gap with servicePath™ CPQ+.

Explore Our Research — Deep dives on Revenue Architecture 2.0, Salesforce CPQ End of Sale, and CPQ Trends 2026.

We will be at Gartner Finance Symposium/Xpo in National Harbor, May 27 to 29. Reach out to connect on-site.

Connect with Daniel on LinkedIn or visit servicepath.co

Related reading from servicePath™: Revenue Architecture 2.0 | CPQ Trends 2026 | Legacy Salesforce CPQ: What EOS Means | Salesforce CPQ End of Sale 2026 | Gartner 2026 MQ for CPQ | SteelBrick Sunset Field Guide

Glossary: Audit Trail | CPQ AI | Revenue Engine | Service Contracts | Salesforce CPQ | Configure Price Quote