When Your CPQ Becomes Your Ceiling: The 2026 Revenue Architecture Decision

Salesforce CPQ End of Sale 2026 did not feel like a crisis when it was announced on March 19, 2025. Most of the 6,000+ affected organizations filed it under “deal with later.” After all, End of Sale isn’t End of Life—existing systems keep running, support continues, and the projected End-of-Life window sits comfortably in 2029-2030.

But here’s what that timeline obscures: the real deadline isn’t when Salesforce pulls support. It’s when your revenue infrastructure becomes the constraint preventing you from competing in an AI-native market.

That deadline is closer than most executives realize.

Salesforce CPQ End of Sale 2026: The Strategic Question

The surface question is straightforward: migrate to Revenue Cloud, deploy a composable alternative, or wrap legacy CPQ with AI agents to buy time?

The strategic question is different: Can your revenue architecture scale the business you’re building, or is it optimized for the business you used to run?

Consider what’s changed since CPQ was designed:

The CPQ market is growing 15%+ annually—from $3.63 billion in 2026 to a projected $7.55 billion by 2031. But that growth masks a fundamental shift in what enterprises are buying.

By end of 2026, 40% of enterprise applications will feature task-specific AI agents. By 2028, AI agents are projected to outnumber human sellers by 10:1. Yet fewer than 40% of sellers report productivity gains from AI.

The disconnect isn’t the technology—it’s the integration architecture. Legacy CPQ can’t feed AI agents the real-time pricing signals they need. Batch processing. Monolithic design. Data locked inside the CRM, inaccessible to the orchestration layer where AI actually operates.

Meanwhile, 94% of CIOs expect major changes within 24 months, 82% of organizations have adopted API-first approaches, and 70% of enterprises are moving to composable architectures.

Translation: The infrastructure that powered revenue operations in 2020 is now the bottleneck preventing AI-enabled velocity in 2026.

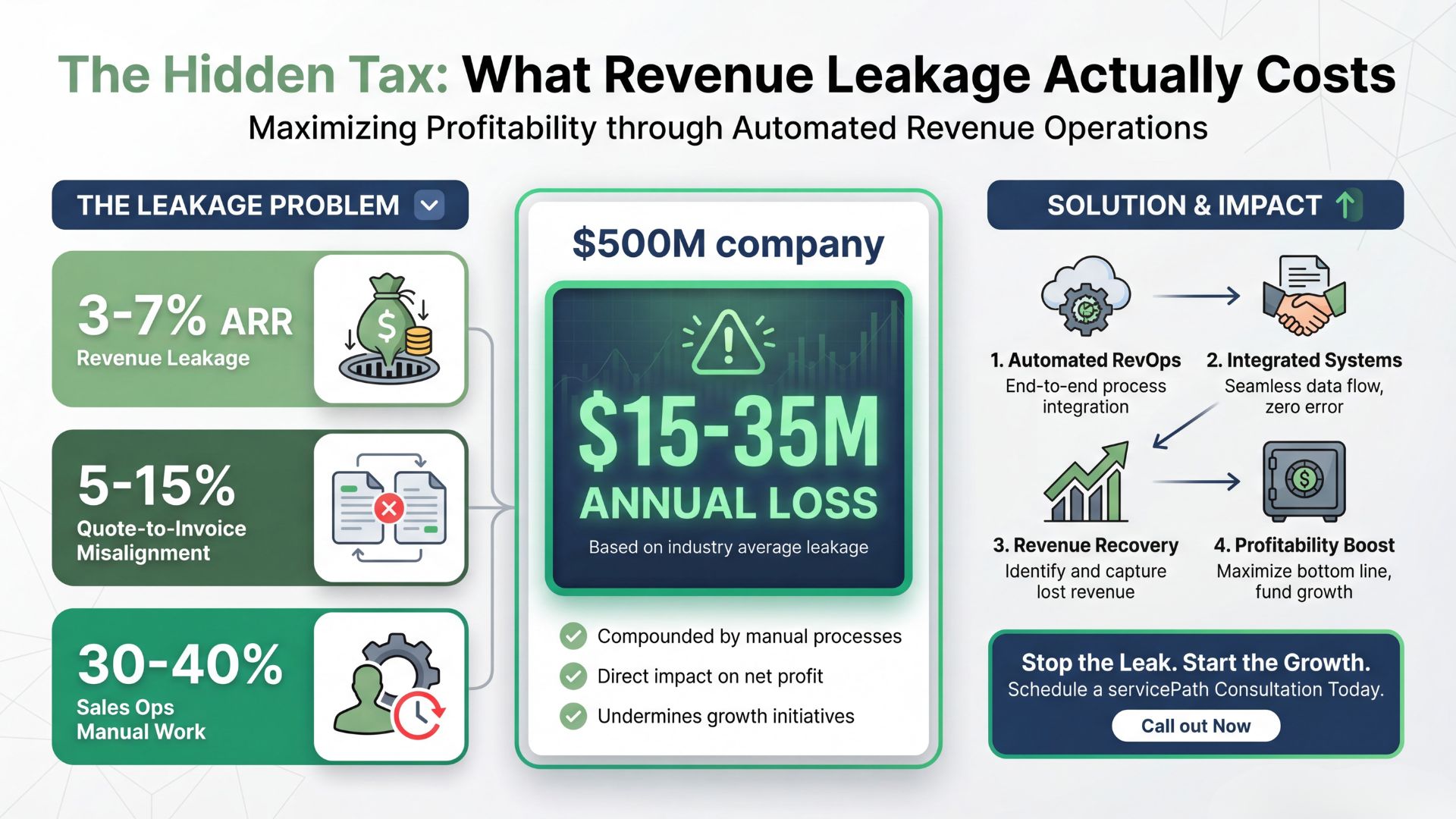

The Hidden Tax: What Revenue Leakage Actually Costs

Let’s ground this in numbers.

Revenue leakage among legacy CPQ users runs 3–7% of ARR. Quote-to-invoice misalignment costs 5–15% of potential revenue. Sales operations teams spend 30–40% of their time on manual workarounds.

For a $500 million revenue company, that’s $15–$35 million annually—before factoring in opportunity cost.

But here’s what those percentages don’t capture: strategic mobility.

How long does it take you to launch a new product bundle? To test hybrid pricing in a new market? To enable cross-selling after an acquisition?

If the answer involves months of developer time, data migration projects, or “we’ll get to it in Q3,” you’re not just losing revenue to leakage. You’re losing the ability to move at market speed.

First-year technical debt on legacy CPQ: $400K–$800K. It compounds annually. And unlike financial debt, you can’t refinance your way out—you have to rebuild.

Three Salesforce CPQ End of Sale Migration Paths

Over the past 18 months, I’ve watched dozens of enterprises navigate Salesforce CPQ End of Sale 2026. Three strategic patterns have emerged—not as technology choices, but as bets about where enterprise architecture is headed.

Path 1: The Bridge Strategy

The approach: Wrap legacy CPQ with AI agents and microservices to buy 12–18 months of migration runway.

Who’s choosing this: Mid-market companies with complex catalogs, limited M&A activity, and executive teams that need time to align on a long-term play.

The promise: Research shows 25–30% improvements in quote accuracy and 40% reductions in sales cycles with intelligent wrappers.

The reality: You’re adding integration layers on top of a foundation that’s already showing cracks. Every AI wrapper increases the complexity of your eventual migration. The technical debt doesn’t disappear—it just gets more expensive to unwind.

This strategy works for exactly one scenario: buying time to build consensus on real modernization. If that’s not your explicit goal, you’re deferring the decision—not making it.

Path 2: The Revenue Cloud Bet

The approach: Full migration to Salesforce Revenue Cloud Advanced.

The economics: ~$200/user/month base pricing, +$125–$200/user/month for CLM, plus billing modules. Implementation costs range from $10,000 to $150,000+ depending on complexity. 6–12 months for complex deployments with data-model cleanup required. Note: Salesforce raised prices ~6% in 2025, affecting 2026 TCO calculations.

Who’s choosing this: Single-CRM organizations with deep Salesforce investment, tolerance for data-model redesign, and confidence that Salesforce will remain their system of record for the next 5+ years.

What works: If you’re committed to Salesforce as your revenue control plane and you’re willing to do the data cleanup, Revenue Cloud is engineered for enterprise scale. It’s a known quantity with mature support infrastructure.

The strategic question: What happens when you acquire a company running HubSpot? Or Microsoft Dynamics? Or an M&A target that’s already mid-migration to something else?

If the answer is “18–24 month integration timeline,” you’re building a sophisticated monolith that can’t keep pace with an acquisition-driven growth strategy. Beautiful architecture. Wrong era.

Path 3: The Composable Bet

The approach: Deploy API-first, AI-native CPQ that orchestrates pricing across multiple CRMs without forcing consolidation.

The proof points: Telent went live in 8 weeks with ~60% quote-cycle reduction after replacing a failed legacy implementation. Dell EMC scaled their partner ecosystem without requiring CRM standardization. One financial services company achieved 90% reduction in time-to-quote after migration.

Who’s choosing this: Multi-CRM enterprises, M&A-active companies, and organizations that treat speed-to-market as a competitive differentiator rather than an operational metric.

The advantage: Day 1 cross-selling in M&A scenarios. $250K–$500K+ in avoided migration costs per transaction. 70% faster synergy capture.

The bet: You’re wagering that composability—not consolidation—defines the next decade of enterprise architecture. That bet looks increasingly credible. 82% of organizations have adopted API-first approaches. The composable applications market is projected to reach $11.8B by 2028.

But it requires rethinking how you build revenue infrastructure. If your instinct is to consolidate everything into one system of record, this path will feel uncomfortable—even if the data suggests it’s right.

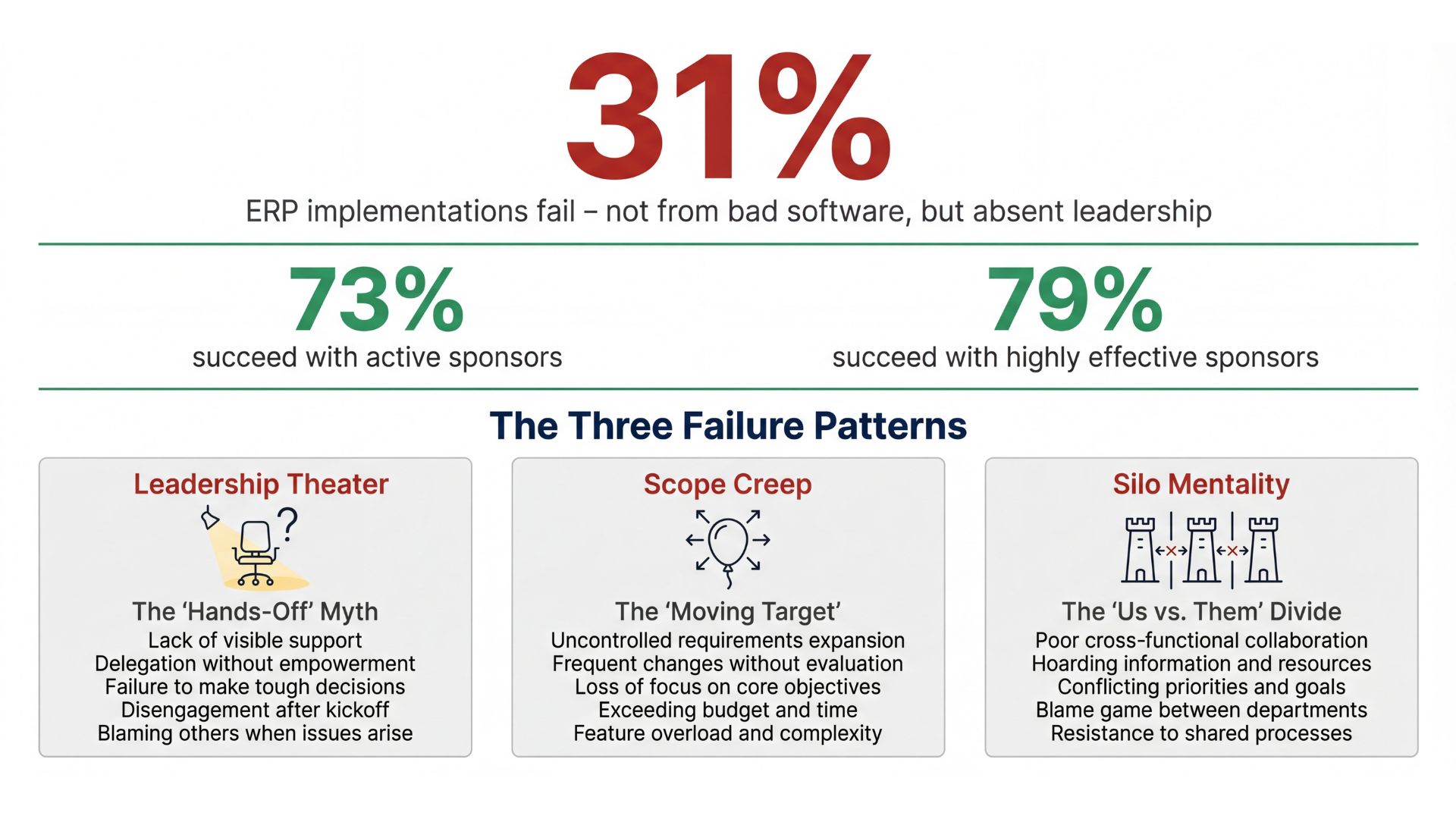

Why Projects Fail (And It’s Never the Software)

31% of ERP implementations fail due to lack of executive sponsorship—not bad data, not wrong vendor selection, not inadequate budget. Sponsorship.

73% success rate with active sponsors. 79% when sponsors are highly effective.

Here’s what that means in practice:

Leadership theater: The sponsor shows up for kickoff, gets their photo with the vendor, then delegates execution to a director who has no authority to make trade-offs when reality hits.

Data debt denial: “The migration will clean up our data” is enterprise wishful thinking. It never happens. Data quality is a prerequisite for migration, not an output of it.

Checkbox training: One 90-minute demo for 200 people instead of role-based reskilling over 90 days. Then executives wonder why adoption stalls at 40%.

MIT found that 95% of enterprise gen-AI pilots fail to deliver measurable P&L impact. The cause isn’t the AI technology—it’s integration gaps and sponsorship failures.

The pattern is consistent: The technology works. The humans don’t.

The C-Suite Lens: What Each Role Should Actually Care About

For the CRO: This Is About Market Velocity, Not Quote Velocity

Your competitors aren’t winning because they have better sales reps or more aggressive pricing. They’re winning because their revenue architecture lets them test new models, launch hybrid bundles, and iterate based on market feedback—without opening developer tickets.

25–30% improvements in quote accuracy and 40% reductions in sales cycles aren’t just efficiency gains. They’re the difference between being first-to-market with a new pricing model and spending six months watching competitors test what you can’t ship.

The question isn’t “Can we quote faster?” It’s “Can our revenue architecture support the business model we’ll need in 2027?”

If you’re still trying to force 2026 go-to-market strategy into 2020 infrastructure, the answer is no.

For the CFO: Revenue Leakage Is a P&L Line Item You’re Not Tracking

3–7% ARR leakage. 5–15% quote-to-invoice mismatch. 30–40% of sales ops capacity consumed by manual reconciliation.

Run those numbers on your revenue base. Now add the DSO impact from configuration-induced delays.

ROI framework: Reducing pricing errors from 5% to 2% on $10 million in annual sales recovers $300,000—typically within the first year. AI-native implementations show 2.8× ROI versus non-AI tools, with meaningfully shorter time-to-value.

This isn’t infrastructure spend. This is margin recovery disguised as a software project.

For the CTO/CIO: Integration Debt Is Killing Your AI Strategy

94% of CIOs expect major changes within 24 months. AI integration tops every priority list.

But here’s the constraint: Legacy CPQ governance limitations risk locking you out of the modern composable stack. Each manual integration adds 18–24 month timelines to what should be API-driven orchestration.

Meanwhile, 82% of enterprises have adopted API-first approaches. Real-time data feeds. Multi-system orchestration. The things AI agents actually need to function.

The gap between “our AI strategy” and “our revenue infrastructure” is where AI pilots go to die.

For the CEO: Revenue Infrastructure Is Your AI Control Plane

By 2028, AI agents will outnumber human sellers by 10:1.

The strategic question isn’t whether you’ll adopt AI. It’s whether your revenue architecture can scale it when your competitors are already deploying it.

Single-CRM-lock at acquisition time? Strategic liability in an M&A-driven growth environment.

Batch processing instead of real-time pricing feeds? Velocity tax that won’t show up on a dashboard until you’ve lost three quarters of momentum.

Research shows CEOs consistently underestimate digitalization complexity. Revenue infrastructure isn’t just ops. It’s the control plane for your AI strategy—and the difference between leading your market and explaining to the board why integration timelines keep slipping.

The Decision Framework: Five Questions That Actually Matter

Forget the vendor pitch decks. Here are the five questions that separate strategic clarity from expensive mistakes:

1. How many CRMs will you run in three years?

If the honest answer is “one, and it’s Salesforce,” Revenue Cloud makes sense.

If the answer is “multiple” or “I don’t know”—because M&A, because regional autonomy, because you acquired companies that won’t consolidate—composable architecture is the only path that doesn’t force a choice between growth strategy and systems strategy.

2. What’s your product complexity trajectory?

Simple catalogs (<500 SKUs, limited dependencies) can survive on AI wrappers for 12–18 months.

Complex catalogs (1,000+ SKUs, heavy product dependencies, rule-based pricing) need real migration—either to Revenue Cloud or composable CPQ. Half-measures just accumulate technical debt.

3. What’s your AI maturity—honestly?

Committee exploration and proof-of-concept pilots? Revenue Cloud with future AI add-ons is the safe bet.

Agentic workflows already in production, with AI agents making autonomous pricing decisions? You need composable, real-time pricing feeds. Legacy batch processing won’t scale.

4. What’s your M&A outlook over the next 36 months?

Organic growth with no acquisitions? Revenue Cloud’s integration complexity is manageable.

Active acquirer with 2+ deals per year? Composable architecture enables Day 1 cross-selling and 70% faster synergy capture. Every avoided 18-month integration saves $250K–$500K+ in direct costs—and preserves momentum that can’t be measured in dollars.

5. What’s your organizational risk tolerance?

Lower risk appetite? Pilot-first approach with structured success criteria. Choose one region or product line, define 3–5 measurable outcomes, and build conviction before scaling.

Higher risk tolerance? Full Revenue Cloud migration with upfront data-model redesign—but only if you’re confident Salesforce remains your system of record through 2030.

Why servicePath™ (And Why It Matters for This Decision)

Full disclosure: servicePath™ is the sole Visionary in Gartner’s 2026 Magic Quadrant for CPQ Applications—the fourth consecutive year.

But here’s why that positioning matters for the Salesforce CPQ End-of-Sale 2026 decision:

1. AI-Native from the Ground Up

servicePath™ is architected with AI as foundational, not retrofitted. Codeless configuration. Real-time AI-driven pricing optimization. Native integration with enterprise AI agents.

This isn’t vaporware. It’s in production at Dell EMC, Telent, and dozens of enterprises that couldn’t afford to wait for legacy platforms to catch up.

2. The RIAC Framework (Revenue-IT Architecture Convergence)

servicePath™ pioneered RIAC—the ability to orchestrate pricing across multiple CRMs without forcing consolidation.

Launch hybrid pricing Day 1 in M&A. No data migration. No 18-month integration timelines. 70% faster synergy capture because you’re orchestrating, not consolidating.

3. Proven Implementation Velocity

Telent: 8 weeks to go-live, ~60% quote-cycle reduction.

Dell EMC: partner ecosystem scaled without CRM consolidation.

Financial services company: 90% reduction in time-to-quote post-migration.

These aren’t product marketing claims. They’re documented case studies from enterprises that bet their revenue operations on composable architecture—and won.

4. Multi-CRM as Default State

Unlike platforms designed for single-CRM environments, servicePath™ treats multi-CRM as the baseline assumption—because that’s the reality of modern M&A.

No vendor lock-in at acquisition time. $250K–$500K+ in avoided migration costs per M&A transaction. Cross-selling enabled without forced system consolidation.

This is the composable bet—and it aligns with where enterprise architecture is demonstrably headed.

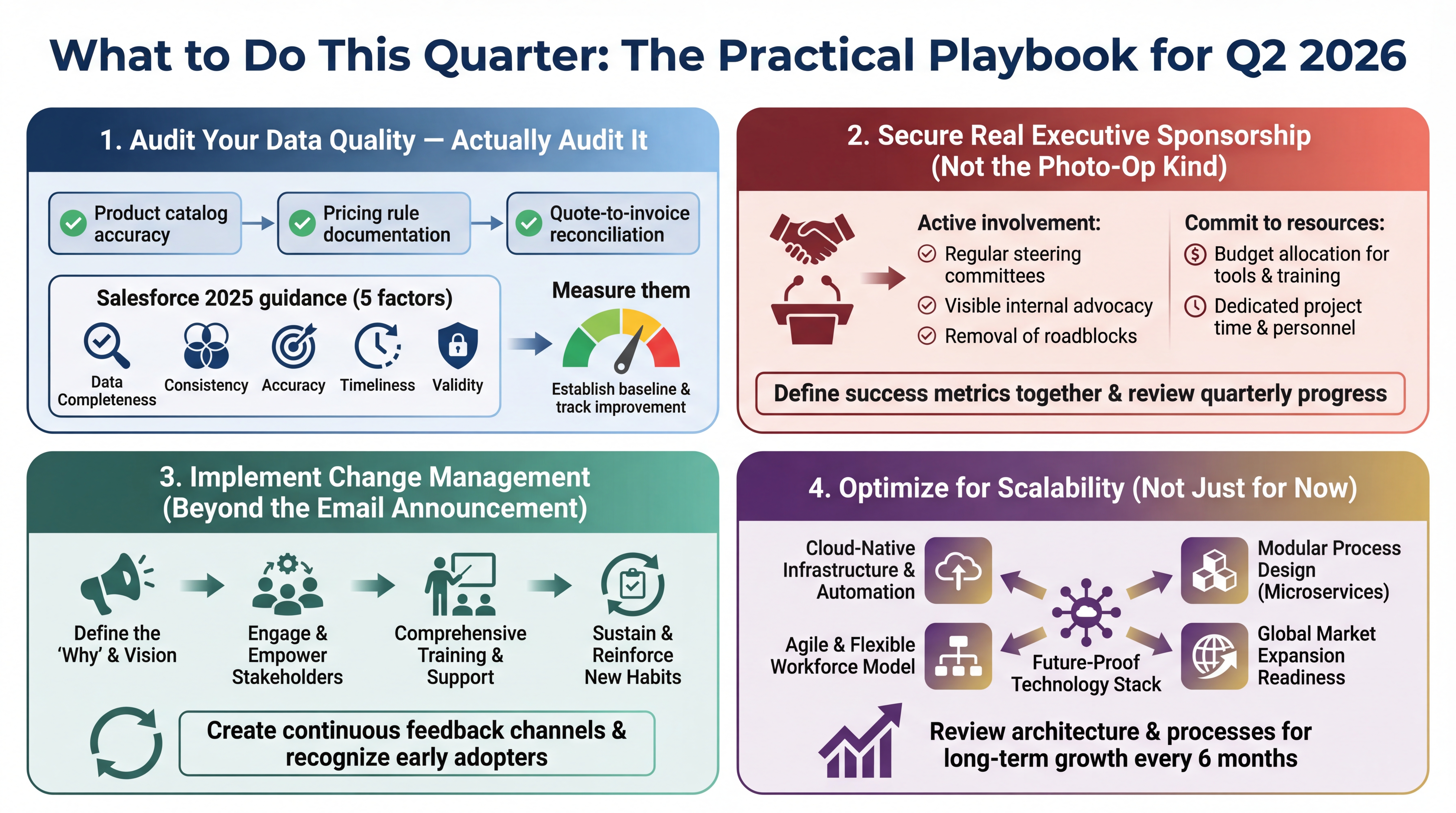

What to Do This Quarter: The Practical Playbook

If you’re serious about getting Salesforce CPQ End of Sale 2026 right, here’s what matters in Q2 2026:

1. Audit Your Data Quality—Actually Audit It

Not your data strategy. Not your roadmap. Your actual data.

Product catalog accuracy. Pricing rule documentation. Quote-to-invoice reconciliation rates. Salesforce’s 2025 data-readiness guidance lays out five critical factors. Measure them.

2. Secure Real Executive Sponsorship (Not the Photo-Op Kind)

Not the kind where someone attends kickoff and delegates.

The kind where they’re in the 30/60/90-day governance reviews, making trade-offs when reality diverges from the plan, and taking ownership when adoption stalls.

3. Run a Structured Pilot—Not a Proof of Concept

Choose your most complex product line—not your easiest. If it works there, it scales.

Define 3–5 measurable outcomes: cycle time, quote accuracy, seller adoption rate.

Structured pilots achieve 40–60% conversion rates versus <10% for free trials. The difference is commitment and clear success criteria.

4. Be Honest About Your M&A Timeline

If you’re acquiring companies in the next 24 months, multi-CRM orchestration isn’t optional. Plan for it now—or pay the integration tax repeatedly, deal after deal, while competitors move faster.

Salesforce CPQ End of Sale 2026: The Bottom Line

Salesforce CPQ End of Sale 2026 isn’t about replacing software. It’s about whether you’re building revenue architecture that scales your business strategy, or optimizing for the company you used to be.

The executives who get this decision right will enter 2027 with AI-enabled revenue operations, the ability to move at market speed, and revenue infrastructure that doesn’t constrain growth.

The ones who don’t will spend 2027 explaining to their board why integration timelines keep slipping, why revenue leakage is a “known issue,” and why competitors are moving faster despite similar market conditions.

The choice isn’t complicated. The execution is.

Act in Q2 2026. Lead in 2027.

Ready to Ensure Your CPQ Doesn’t Become Your Growth Ceiling?

The 2026 Revenue Architecture Imperative

Salesforce CPQ End of Sale 2026 is not a sunset notice. It is a strategic inflection point.

The real deadline is not 2029 or 2030. It is the moment your revenue infrastructure can no longer support AI-native selling, multi-CRM reality, and acquisition-driven growth.

The critical reality:

AI does not fail because of algorithms. It fails because legacy architecture cannot feed it clean, real-time, orchestrated pricing data.

The path forward:

Revenue architecture is no longer an IT decision. It is a board-level growth decision.

The question is not whether you will modernize.

The question is whether you will do it before velocity becomes someone else’s advantage.

Take Action: Your Next Steps

Step 1: Evaluate Your Revenue Architecture Readiness

Pressure-test your current environment against the five decision questions:

- How many CRMs will you operate in three years?

- How complex will your product catalog become?

- Is your AI strategy production-grade or experimental?

- What is your M&A trajectory over the next 36 months?

- What is your real risk tolerance?

If those answers create tension, your infrastructure is already signaling constraint.

Step 2: Speak with a Revenue Architecture Expert

Engage a servicePath™ CPQ architect to:

- Assess legacy technical debt exposure

- Quantify revenue leakage and integration latency

- Model ROI across Revenue Cloud vs. composable pathways

- Evaluate Day 1 M&A cross-sell readiness

Book Architecture Consultation →

Step 3: See Composable CPQ in Action

Explore how AI-native, API-first revenue orchestration enables:

- Real-time pricing intelligence

- Multi-CRM execution without consolidation

- Faster synergy capture in M&A scenarios

- Scalable AI agent integration

Step 4: Review Enterprise Case Studies

See how leading enterprises achieved:

- ~60% reduction in quote cycle time

- 90% reduction in time-to-quote

- 70% faster synergy capture

- Avoided $250K–$500K+ per acquisition in integration costs

Step 5: Deepen Your Strategic Context

Access resources on:

- Composable revenue architecture

- AI-native CPQ design principles

- Multi-CRM orchestration strategies

- Revenue infrastructure modernization frameworks

Resources:

About servicePath™

servicePath™ is the sole Visionary in Gartner’s 2026 Magic Quadrant for CPQ Applications, recognized for AI-native composable revenue architecture. With proven implementations at Telent, Dell EMC, and enterprise leaders worldwide; servicePath™ is the AI-native enterprise CPQ and revenue lifecycle platform built specifically for mid-to-large technology service providers, including MSPs, SaaS, Field Services, Financial Services, and XaaS organizations.

Unlike traditional product-centric CPQ tools, servicePath™ is designed for complexity. We help enterprises manage multi-region catalogs, hybrid pricing models, dynamic service bundles, and margin-sensitive deals—all in one codeless, AI-ready architecture.

Learn more: servicepath.co

Frequently Asked Questions: Salesforce CPQ End of Sale 2026

1) What does Salesforce CPQ End of Sale 2026 mean for existing customers?

Salesforce CPQ End of Sale 2026 means the product is no longer being sold to new customers, but existing users can continue operating under current agreements. However, End of Sale is often the start of strategic risk, not the end of operational viability.

2) Is Salesforce CPQ End of Sale the same as End of Life?

No. End of Sale does not mean immediate End of Life. Support may continue for several years. The real risk is not the vendor timeline, but whether your CPQ architecture can support AI-native, multi-CRM, and M&A-driven growth through 2027 and beyond.

3) What are the main alternatives after Salesforce CPQ End of Sale?

Enterprises typically evaluate three paths:

-

Migrating to Salesforce Revenue Cloud

-

Adopting a composable, API-first CPQ platform

-

Using a short-term bridge strategy while planning full modernization

The right choice depends on CRM strategy, product complexity, AI maturity, and acquisition plans.

4) How do we decide between Revenue Cloud and composable CPQ?

If your organization will operate a single CRM long-term and has limited M&A complexity, Revenue Cloud may align.

If you expect multiple CRMs, frequent acquisitions, or need real-time AI-driven pricing across systems, composable CPQ architecture is often more scalable.

5) Why shouldn’t we wait until Salesforce CPQ End of Life?

Waiting can increase revenue leakage, integration debt, and technical constraints. Modern revenue operations require real-time data orchestration and AI readiness. The longer modernization is delayed, the harder it becomes to move at market speed.

6) What is the biggest strategic risk of staying on legacy CPQ?

The biggest risk is not support expiration. It is architectural limitation. Legacy CPQ can restrict AI integration, slow product launches, and complicate post-acquisition cross-selling, ultimately turning revenue infrastructure into a growth ceiling.