The Compliance Trap: When Faster Order-to-Cash Becomes a SOX & ASC 606 Liability (and What Governance‑First AI Actually Means)

Executive Summary: The Defining Tension of Finance in 2026

Finance leaders are currently trapped.

The board and CEO have issued a clear mandate. You must close books faster. You must automate more transactions. Simultaneously, you must tighten controls. Regulatory scrutiny is increasing. Yet, resources remain flat or shrink.

The pressure is acute.

Deloitte’s Finance Trends 2026 research reports a stark gap. “More than 70%” of finance leaders need significantly more resources. They need them just to capture current opportunities. They must build the future of finance. Yet, current demands stretch their capacity thin. Source

CFOs are betting heavily on Artificial Intelligence to bridge this gap. They hope AI will provide the needed productivity boost.

Deloitte’s CFO Signals report confirms this. 87% of CFOs expect AI to be extremely important in 2026. Furthermore, 54% say integrating AI agents is a top priority. The industry has pushed its chips all-in on AI. Source

The Trap vs. The Velocity Promise

Here is the catch few vendors admit. Speeding up order‑to‑cash through automation without tightening governance fails. It does not modernize finance. It scales exceptions.

Suppose you deploy autonomous agents into a fragmented data environment. Quotes might not match contracts. Contracts might not match invoices. In that scenario, you are not automating revenue. Instead, you are automating audit discrepancies. You create them at a speed human teams cannot manage.

Crucially, consider SOX 404. An autonomous agent might make a material financial decision. That decision might not be auditable. This is not just a tech failure. It is a potential material weakness in internal controls. You, as a finance leader, must personally certify it.

The Governance-First Imperative

The win condition for the modern CFO isn’t “AI everywhere.” It is Governance-First Automation.

This isn’t about putting brakes on the business. Governance-First is a paved highway. It allows you to drive fast without crashing.

Therefore, we must design systems where machine‑readable evidence is default. Continuous traceability from quote to revenue must be standard. The World Economic Forum (WEF) and Capgemini call for this framing. They argue we must govern agents through scalable practices.

Without this foundation, speed is just risk acceleration. Source

Part 1: The Anatomy of the Compliance Trap

The “Compliance Trap” is not merely a failure of internal strategy. It is a structural failure of the software market. This market allowed an “Ecosystem Accountability Gap” to widen.

Enterprises have operated with major CRMs on one side. These are optimized for sales velocity. On the other side are major ERPs optimized for financial control. Neither ecosystem governs the transition between those two states.

The “General Contractor” Problem

Think of your CRM as a fantastic General Contractor. They are brilliant at framing the house quickly. They keep the project moving. But you would not ask your General Contractor to perform heart surgery.

Yet, that is exactly what happens. You leave SOX compliance and ASC 606 logic in CRM hands. CRMs are great for sales. However, most are functionally “revenue-illiterate.” Consequently, they do not understand accounting consequences.

When you inject AI agents into that gap, they don’t bridge it. They exploit it. They accelerate the creation of unverifiable data. Finance must then manually clean this up.

Organizations often approach order-to-cash as disconnected silos. You modernize CPQ for Sales. You implement a new billing engine for Finance. You deploy AI-chaser bots for Collections. Each team optimizes locally.

As a result, order-to-cash accelerates on paper. The “Time to Quote” drops significantly.

Yet, finance discovers the truth at quarter-end. The system of record is now a system of exception.

The data passed between silos lost its context. It lost its meaning. Therefore, the finance team must manually reconstruct complex deals for auditors.

The Collision: Continuous Finance vs. Static Controls

“Continuous” finance is colliding with rigid traditional controls. Business decision-making has outpaced financial control:

“In the past, we may have run scenario’s monthly; now we’ve been running models and doing analysis almost daily.”

— David Chojnowski, Corporate Controller & Chief Accounting Officer, Walmart Source

Analysis and decision-making happen daily. But controls are applied quarterly. This creates a “Governance Gap.”

In that gap, humans and AI agents make thousands of micro-decisions. For example, they bundle products or offer non-standard discounts. These decisions remain invisible until the audit team reconciles them.

The Deep Constraint: ASC 606 as Process Discipline

ASC 606 (Revenue from Contracts with Customers) is unforgiving. It is not just an accounting memo for the end of the quarter. It is process discipline.

ASC 606 requires a linear logic flow. This flow must be evidence-backed. It must mirror commercial reality. The FASB’s Topic 606 summary lays out a five-step model. Each step is a failure point for ungoverned processes:

- Identify the contract: Does the system recognize an email agreement is a contract modification?

- Identify performance obligations: Can automation distinguish a “distinct” license from a professional service?

- Determine transaction price: Can it handle variable consideration or rebates?

- Allocate transaction price: Does it know the Standalone Selling Price (SSP) for allocation?

- Recognize revenue: Does it know the difference between “point-in-time” vs. “over-time” recognition? Source

Your data must consistently answer critical questions. “What was promised? What changed? What was delivered? WHY was it treated this way?” If it cannot, you do not have automation.

You have the acceleration of audit friction.

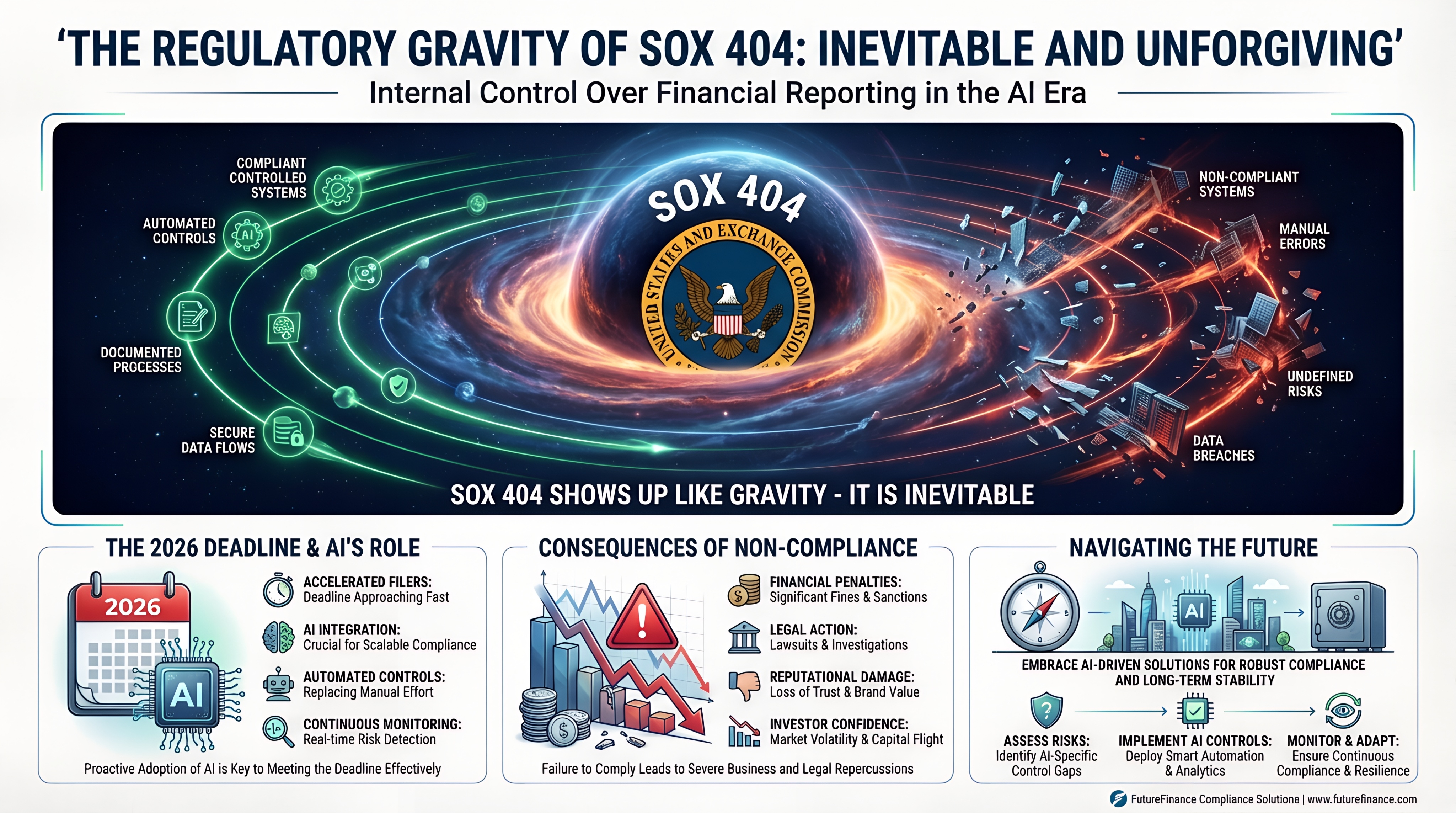

The Regulatory Gravity of SOX 404

Then SOX 404 shows up like gravity. It is inevitable. The SEC’s materials explain SOX 404 strictly regarding internal control over financial reporting (ICFR). Source

Here is the critical realization for 2026. If an AI agent touches data that feeds the General Ledger, it is part of the control environment.

Suppose an AI agent re-allocates revenue based on an algorithm. It must produce a log explaining the why. If it cannot, you do not just have a “black box.” Instead, you have a potential material weakness in internal controls. You cannot prove financial statements are accurate if the mechanisms are opaque.

The Verdict: Fast order-to-cash without robust evidence architecture is just faster failure.

Part 2: Phoenix — Operationalizing the “Shift Left” Model

If the Compliance Trap is the problem, Phoenix is the answer.

Phoenix is a rebuild philosophy. It is not a “rip and replace” of core ERP systems. Instead, it is a fundamental shift in mindset: “Stop pretending the close is where you fix revenue.”

Forward-thinking finance leaders are shifting controls left. They are moving controls closer to where commercial decisions are made.

This is not just about safety; it is about velocity.

You must move governance to the front of the sales cycle. Move it into a robust Configure, Price, Quote (CPQ) engine. This ensures only clean, compliant deals enter the pipe.

CPQ becomes your governance gateway. It is where you enforce business rules and pricing guardrails before commitment. Clean deals do not get stuck in “approval purgatory.” They sail through to revenue recognition.

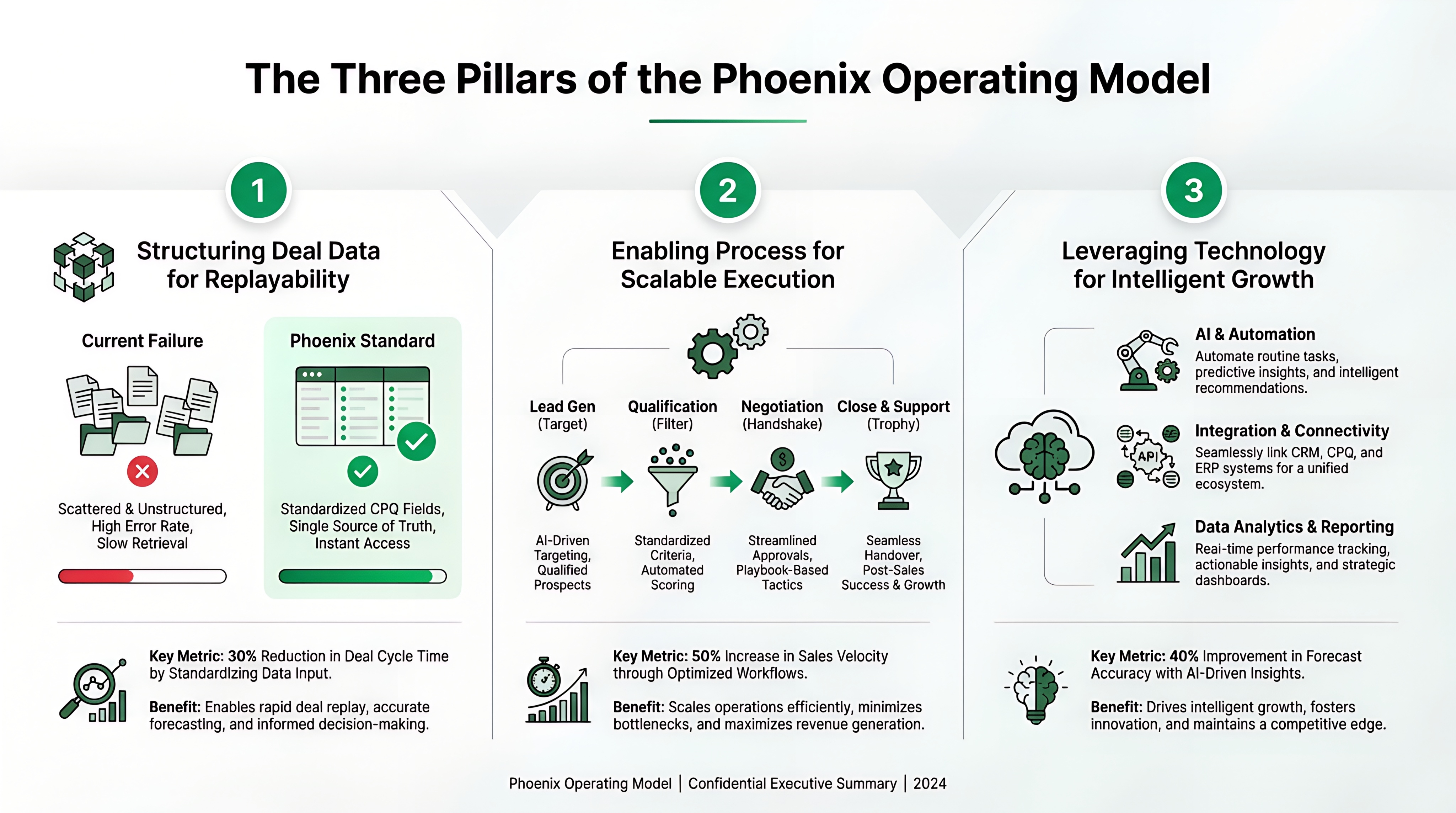

The Three Pillars of the Phoenix Operating Model:

1. Structuring Deal Data for Replayability (via CPQ)

- Revenue logic must be replayable. You should take raw data from the Quote and Contract years later and get the exact same revenue result.

-

-

The Current Failure Mode: Sales Reps enter critical terms into free-text descriptions. This data is invisible to automated revenue engines.

-

The Phoenix Standard: CPQ enforces structured fields for relevant terms. If a term affects revenue, it must be a structured data field. It is never a comment.

-

- Capturing Evidence at the Point of ActionMost audits are painful archaeological digs. Finance teams dig through emails to find old approvals.Phoenix demands capturing evidence at the point of action. For instance, when a discount is approved, the system captures who, why (a code), and when. Crucially, this metadata travels with the transaction forever.

- Enforcing Traceability (Lineage)Every dollar recognized in the General Ledger must trace back to a specific contract obligation.

-

The Challenge: Integration breaks. The ERP sees a generic “Service Revenue” bucket. The CRM sees specific project names. Thus, the connection is lost.

-

The Fix: A unified data key or “Golden Thread” that persists from Lead to Cash to Renewal.

-

Strategic Validation from Leadership

Deloitte’s Finance Trends 2026 findings call this out. Finance leaders are building agile governance models for faster decision-making. They recognize that speed requires better brakes and steering, not just a bigger engine. Source

AI fundamentally changes the decision surface:

“We’re able to use AI to understand market trends and correlate those trends and other competitors’ decisions with ours in a way that we haven’t been able to in the past.”

— David Chojnowski, Corporate Controller & Chief Accounting Officer, Walmart Source

This capability is only possible if your internal deal data is clean, structured, and governable.

The “Quiet Part” Out Loud

This is the Phoenix model framed as a competitive advantage:

“We have a chance to be a real strategic partner to the business, with capabilities like advances in AI and agentic AI enabling much more real-time and effective decision making,”

— Marie Myers, EVP & CFO, Hewlett Packard Enterprise Source

Phoenix Summary: Speed is fine—but only if the foundation is real.

Part 3: From Copper to 6G — The Integration Gap

We use the metaphor “Copper to 6G.” It describes the difference between merely connected systems and connected truth.

Copper: Your stack passes data. The API works. Field A in Salesforce maps to Field B in NetSuite. The pipe exists.

6G: Your stack passes meaning. The system understands that “Service Start Date” drives “Revenue Recognition Start Date.” Furthermore, it proves why based on contract terms.

The AI Acceleration Factor

AI makes this gap painfully obvious. Put a Ferrari engine (a high-speed AI Agent) into a Model T chassis (fragile “Copper” wiring). The car shakes itself apart.

Gartner predicts 40% of enterprise applications will include task-specific AI agents by 2026. The proliferation of these agents is imminent. Source

The “Spreadsheet Glue” Problem

Is your current order-to-cash environment defined by “spreadsheet glue”? Does critical revenue logic live in Excel files on desktops? If so, adding agents does not create autonomy. Instead, it creates autonomous inconsistency.

The Concrete AI Threat: A Financial Hallucination Scenario

Consider an AI Sales Agent. It is tasked with “Optimizing Renewals for Retention.” It analyzes customer sentiment and determines a key account is at risk. To save the deal, the AI autonomously offers a 30% discount. It also waives the standard annual inflation adjustment clause.

The agent succeeds in its local task. The customer renews instantly.

However, the AI lacked the “6G” context. It didn’t know the company’s long-term profitability depends on those inflation adjustments compounding.

The agent just wiped out millions dollars in future contract value (TCV) to secure a short-term win. It happened outside structured guardrails. Finance only discovers the massive liability during an audit months later.

The WEF/Capgemini paper is explicit. Agents introduce new governance challenges. Traditional software governance models are insufficient for autonomy. Therefore, you cannot “patch” this complexity. You must design for it structurally. Source

Part 4: Governance-First AI — The New Standard

Governance-First AI is not a compliance tax that slows innovation. It is the only way agentic automation survives contact with audit and regulators.

The World Economic Forum frames agent adoption as a governance progression. You must classify agents, evaluate risks, and scale governance proportionate to autonomy. Source

The Core Principles of Governance-First AI in Finance:

Least Privilege is Foundational

The WEF calls least privilege “essential.” In finance, this is critical. An AI agent should not have “God Mode” access to the ERP.

-

Practical Application: An agent drafting invoice responses needs read-only access to Invoices. It needs write access to Email Drafts. It should not have write access to the General Ledger.

Audit Logs are Not Optional—They Are Central

Audit logs are central to agent oversight. This goes beyond standard system logs.

-

The Requirement: Every significant agent action must generate a structured log. It must answer: Who (Agent ID), What (Action Taken), Why (Policy referenced), and When (Timestamp).

-

The Use Case: An auditor asks, “Why was this customer categorized as High Risk?” You must point to the specific log entry referencing internal policy. If the “Why” is missing, the control has failed.

The “Plain Language” Executive Test

Look to Embraer’s approach for a plain language governance point:

“We want to motivate and encourage our departments to build their own solutions without creating a second or third IT structure.”

— Antonio Carlos Garcia, Executive Vice President & CFO, Embraer Source

You need a unified governance layer. This allows Democratized AI without creating a massive “Shadow IT” risk.

[Visual Anchor #3 Placeholder: Insert “WEF/Capgemini Governance Model” image here]

The Governance-First Standard:

If the agent cannot explain what it did, why it did it, and what evidence it used, it does not belong in order-to-cash. Source

Part 5: Deep Dive into the Three Main Risks

We identified three primary failure modes where speed overwhelms governance in order-to-cash.

Risk #1: The Bundling Trap (Revenue Recognition Whiplash)

The Scenario: A Sales AI agent wants to maximize Total Contract Value (TCV). It bundles a 3-year subscription, professional services, and support into a single, discounted line item. The customer signs immediately.

The Accounting Reality: Bundling isn’t an accounting afterthought. It is a control decision that must happen in the CPQ.

Topic 606 explains that performance obligations must be identified individually. A good is “distinct” only if specified criteria are met. Source

Humans default to shortcuts: “We’ll fix it in rev rec,” or “Close first, reconcile later.”

The AI Failure Mode:

The agent bundled items without identifying them as “distinct” obligations. Consequently, the Revenue Team receives a contract they cannot process automatically.

They must manually review the contract to determine Standalone Selling Price (SSP) and perform allocation. Ultimately, the AI’s “efficiency” created a massive manual debt for Finance.

Your Agent (and CPQ) Must Show:

- Which distinct performance obligations it identified.

- How it allocated price (referencing SSP data).

- What contract evidence it relied on.

Table: Bundling vs. Unbundling (The Audit View)

(Topic 606 core model + allocation logic reference) Source

Risk #2: “MACD Amnesia” (The Lifecycle Traceability Gap)

The Concept: MACD stands for Modify / Add / Cancel / Disconnect. These events happen after the initial signature. This is where revenue integrity dies in subscription businesses.

The Fix: It is boring and powerful. You must enforce a continuous chain of custody:

Quote → Order → Contract → Fulfillment → Invoice → Cash → Revenue.

(Topic 606 requires revenue depiction based on transfer of promised goods. This depends entirely on traceable contract terms and changes.) Source

The Agent Risk:

Gartner’s forecast about agents proliferating is a scale warning. As agents spread, the cost of inconsistency explodes. Source

Consider an AI agent handling a “Disconnect” request. Initially, it successfully processes the cancellation in the CRM. It stops future billing.

However, it might fail to update the Revenue Recognition Schedule in the ERP. The company might continue recognizing revenue for a churned customer. That is a phantom revenue scenario and a significant restatement risk.

The Governance Requirement:

Governance-first AI demands lifecycle replayability. WEF emphasizes audit logs as structured records of activity across the lifecycle. Source

Risk #3: Audit Governance as a Scavenger Hunt

The Pain Point: Most audit pain isn’t defined by a lack of controls. It’s defined by the lack of retrievable evidence. You have the approval. You just can’t find it because it’s buried in Slack.

The WEF Standard:

WEF states that monitoring and logging are core governance practices. Source

The SOX Connection:

SOX 404 turns that principle into operational reality. If the evidence isn’t readily available, the control is deemed ineffective. Source

The goal is machine-readable evidence by default. Decisions are recorded with identity and timestamp. Audit trails must be queryable without heroics.

Part 6: Bain 2026 Takeaway — Foundations First

We must address market reality versus hype. You will hear claims of “1.5x faster order-to-cash growth” via AI. We are careful with such unverifiable metrics.

Bain says it publicly based on research. Finance teams often chase shiny new tools while basics remain underused. Furthermore, integration and data governance are the real bottlenecks to performance. Source

The Case of Danone:

Bain cites Danone applying machine learning in deduction management. This was not a generalist agent. It was a targeted application to a specific, high-volume pain point. Source

The Executive Takeaway for 2026:

If you want order-to-cash transformation to survive audit, don’t start with autonomous agents. Start with the foundation:

- Adoption of mature workflow tools (e.g., killing email approvals with a robust CPQ).

- Data governance that makes automation reliable (fixing “Copper” problems).

- Integration that prevents exception factories (creating the “6G” lineage).

Therefore, then—and only then—scale autonomy with auditability designed in from day one.

Part 7: Frequently Asked Questions (FAQ)

Q1: Does SOX 404 actually apply to automation and AI agents?

A: Yes. SOX 404 is about internal control over financial reporting (ICFR). If automation changes how transactions are initiated, approved, or recorded, it is part of the control environment. An agent acting on financial data without governable logs is a potential material weakness. Source

Q2: Why is bundling such a specific governance problem for AI?

A: Because Topic 606 requires identifying performance obligations based on contracts. Without clear traceability of “distinct” goods, you cannot defend your revenue treatment. If an agent bundles items without logging the rationale, you cannot prove compliance. Source

Q3: What’s the single biggest agent risk in finance?

A: Not that the agent is “wrong”—but that its actions are un-auditable. WEF explicitly places audit logs at the center of governance for agents. If you cannot trace the decision path to evidence, you cannot govern the risk. Source

Q4: Are AI agents actually coming to enterprise finance, or is this hype?

A: They are here. Gartner predicts 40% of enterprise apps will feature task-specific AI agents by the end of 2026. The question for CFOs is not adoption; it is governance of that adoption. Source

Q5: What are CFOs prioritizing in 2026 regarding this?

A: Deloitte’s CFO Signals reports 87% AI importance to finance ops in 2026. 54% prioritizing integrating AI agents. The mandate is clear: modernize or fall behind, but the execution risk is massive. Source

Part 8: The 2026 Operational Readiness Protocol: A 30‑Day Governance Audit

Do not begin with the question, “Which AI agent should I buy?”

Begin with the question, “Which evidence is missing from my current order-to-cash process?”

The WEF frames audit logs and governance as central for oversight as you scale agent autonomy. Source

[Visual Anchor #4 Placeholder: Insert “30-Day Governance Checklist” infographic here]

The 30-Day Governance-First Checklist (High Impact, Low Drama):

Days 1-7: Map the Lineage & Reality

-

[ ] Trace the “Golden Thread”: Map the exact Quote → Cash → Revenue data path for one material product line.

-

[ ] Identify “Air Gaps”: Mark every point where data is manually re-keyed (e.g., PDF to Excel, Email to CRM). These are your highest risk points for AI hallucination.

Days 8-14: Stop Reconstruction & Standardize

-

[ ] Audit the “Distinct” Tag: Verify if your current CPQ explicitly tags performance obligations as “Distinct” (per ASC 606).

-

[ ] Enforce Structured Changes: Add structured “Change Reasons” drop-downs for any contract/booking modifications in your CRM. No more free-text “Notes.”

Days 15-21: Lock Down Access & Evidence

-

[ ] Enforce Least Privilege: Review automated user permissions. Does the bot have admin access it doesn’t need?

-

[ ] Implement Immutable Logging: Ensure deal decisions are logged in a way that cannot be edited later (“write once, read many”).

Days 22-30: The Replay Test

-

[ ] Test Replay: Can you reproduce revenue outcomes solely from contract + event history without asking a human for context? (Topic 606 compliance relies on depicting transfers based on traceable terms; replayability is the operational proof.) Source

Governance isn’t paperwork. It’s what prevents your automation from becoming a compliance incident.

A Final Thought from Daniel Kube

We didn’t build servicePath™ just to make quoting faster. We built it because we spent years watching brilliant finance and sales leaders get ground down by the friction of disconnected systems and ungovernable data.

The technology now exists to solve the tension between speed and compliance. The constraints of 2020 do not apply in 2026. The only remaining variable is leadership will.

It is time to stop coping with the chaos and start governing it.

Further Intelligence & Tools for the Governance-First Leader

Navigating the intersection of AI speed and regulatory compliance requires continuous intelligence. Equip your team with our latest research, proven frameworks, and practical tools.

Gartner Magic Quadrant Report

See why Gartner has named servicePath™ a Visionary in CPQ Application Suites for four consecutive years.

Access the Gartner Report

Proven Enterprise Case Studies

Move from theory to evidence—see how global enterprises design quote-to-revenue for resilience and auditability.

Download Case Studies

Whitepapers & Strategic Guides

Deep-dive frameworks for finance transformation, process discipline, and operational governance.

Explore Resources

The servicePath™ Insight Hub

Stay ahead with practical insights on O2C governance, AI risk, and revenue intelligence.

Read the Blogs

Executive Conversation Podcasts

Listen to candid conversations on the future of finance, risk, RevOps, and revenue operations at scale.

Listen to Podcasts

The Definitive Quote-to-Cash Guide

Understand the full Quote-to-Cash lifecycle—and how to optimize for both speed and control.

Master the Process

Revenue Terms Glossary

Clarity is a control feature—standardize definitions across Sales, Finance, and RevOps teams.

View the Glossary

Sources & References

-

Deloitte — Finance Trends 2026 leadership report hub: Link

-

Deloitte — CFO Signals Q4 2025 (PR Newswire write-up with stats): Link

-

Walmart / Embraer quotes (Deloitte/WSJ CFO): Link

-

HPE CFO Marie Myers quotes (Deloitte/WSJ Risk & Compliance): Link

-

ABB CFO Timo Ihamuotila quote (Deloitte/WSJ CFO): Link

-

Gartner AI agents forecast + Verma quote: Link

-

FASB Topic 606 (ASU 2014-09, Section A): Link

-

SEC SOX 404 study landing page: Link

-

WEF/Capgemini AI Agents governance paper (PDF): Link

-

Bain finance digital tools (Heric): Link

-

IDC FutureScape hub: Link