Executive summary

Enterprise deals rarely fail in the negotiation. Instead, they are mis-shaped months earlier, in the unstructured phase where complex solutions are designed. The damage hides in the Missing Mile, the ungoverned gap between what sales quoted and what finance can explain. As a result, by the time a deal reaches paper, the margin, the delivery risk, and the renewal are already largely decided.

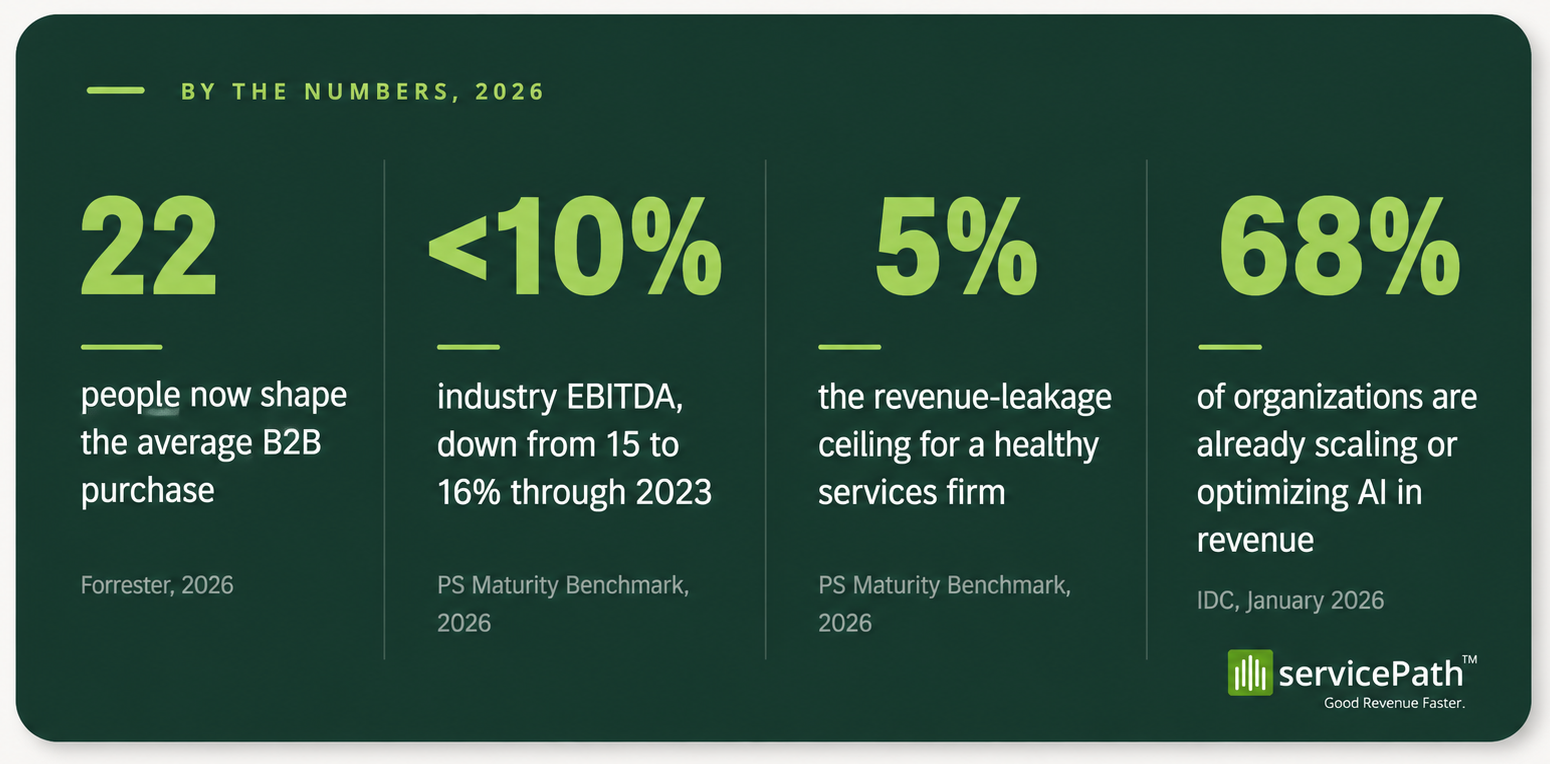

- The average B2B purchase is now shaped by roughly 22 people, and buying groups grow further when AI enters the picture, according to Forrester’s State of Business Buying 2026.

- The damage concentrates in the Missing Mile. The 2026 Professional Services Maturity Benchmark names real-time visibility across delivery and finance as the single capability separating high performers from the rest.

- Meanwhile, the economic buyer is moving from the CRO to the CFO. Finance now treats deal construction as a margin-governance problem, not a sales problem.

- The fix is not a faster quote. Instead, it is Revenue Lifecycle Management: designing the right deal with guided selling, scoring it before signature, and keeping the contract live across delivery, renewal, and expansion.

In short, the problem is no longer selling. It is constructing revenue correctly in the first place.

The room you are not watching

There is an assumption buried inside almost every enterprise sales review, and nobody challenges it. Specifically, we believe deals are won or lost in the room everyone watches: the negotiation, the final pricing call, the board-level sign off.

But it is the wrong room.

By the time a complex deal reaches that table, the outcome is already largely decided. The margin is set. The delivery risk is baked in. Meanwhile, the renewal is quietly alive or already dead. In other words, the room everyone watches is mostly theater. The real decisions happened months earlier, in a far messier place no dashboard reports on.

Picture a deal everyone celebrated on a Friday, with the margin already gone by the first delivery review. No competitor took it. Nobody fumbled the negotiation. Yet it was simply built wrong, long before anyone signed.

So let me state it plainly. Most enterprise deals are not lost. They are mis-shaped. The shape is set early, and a crowd sets it. For example, Forrester’s State of Business Buying 2026 reports a striking number.

On average, 13 internal stakeholders and nine external participants now influence a single B2B purchase.

Moreover, the buying group roughly doubles when the purchase includes generative AI features. Procurement no longer waits at the end to squeeze price. Instead, it is in the room from the start. It is named a decision-maker by 53 percent of respondents, and the C-suite by 68 percent.

By the time a request for proposal appears, then, the requirements are locked and the deal already has a shape. Even the largest vendors concede this is the hard part.

For instance, Oracle’s senior vice president of applications development, Kartik Raghavan, has said growing complexity makes moving from opportunity to fulfillment without added risk increasingly difficult.

Designing a commercial system.

A modern enterprise deal is not a product transaction. Rather, it is a multi-layered commercial system that routinely bundles:

- Products and services

- Subscriptions and usage-based components

- Managed services and service level agreements

- Implementation and lifecycle support

- Multi-year commercial structures with escalators, renewals, and expansion paths

Each layer carries its own cost to serve, delivery risk, and revenue recognition profile. So when you stack them, you are no longer quoting a price. Instead, you are designing a system that must hold its shape for years. It also has to survive every handoff between sales, delivery, finance, and the customer.

Most organizations still try to manage this with linear configure, price, quote logic built for product-only selling. Of course, that logic can produce an accurate number.

However, it cannot tell you whether the system is sound. For example, it cannot see cost to serve or weigh delivery feasibility against commercial structure. Worse, it cannot warn you that the deal carries a margin profile that collapses in month three.

As TSIA Executive Director Thomas Lah argues, in a services-led economy pricing is a company’s most powerful transformation lever.

In other words, value lives in how the deal is structured, not in how fast it is quoted.

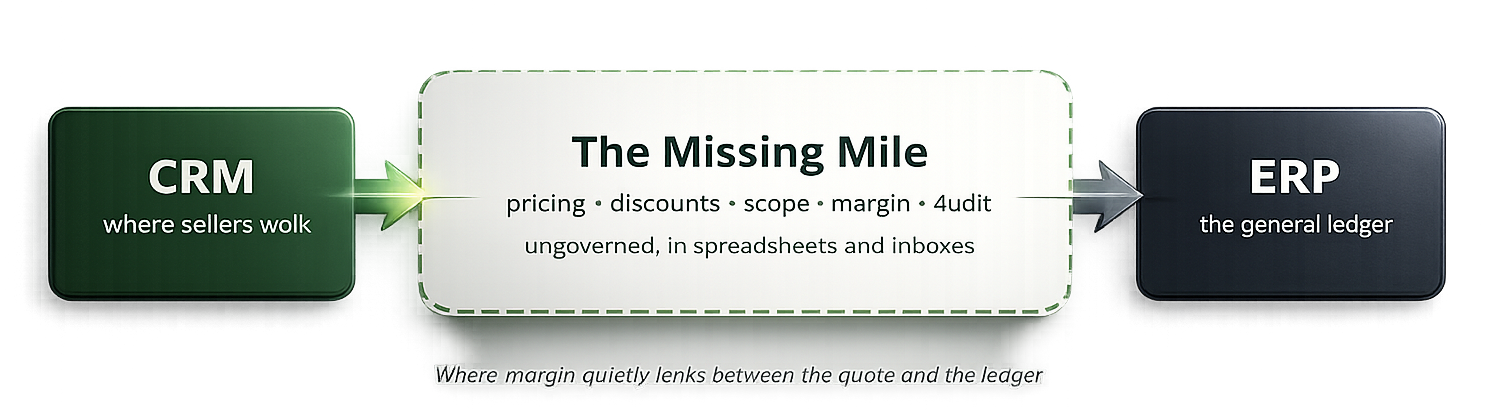

The Missing Mile

I call the place where this goes wrong the Missing Mile. Simply put, it is the gap between what sales quoted and what finance can actually explain.

In most service-led businesses, that gap has never been governed or traced. In fact, it barely exists as structured data.

Pricing decisions, discount approvals, scope assumptions, and contract amendments live in spreadsheets, in inboxes, and in the heads of a few experienced people.

Meanwhile, the front of the business runs on a CRM and the back runs on an ERP. Between them, where a deal is priced, validated, and made audit-ready, there is too often nothing but a spreadsheet.

So that is the Missing Mile, and it is where margin leaks, quietly, between the quote and the general ledger. Because no system owns it, the leakage is misdiagnosed. When numbers come in soft, leadership calls it an execution problem and tells the team to sell harder and discount less. But it was never an execution problem. It is a construction problem, and the cost is now measurable.

For instance, the 2026 Professional Services Maturity Benchmark draws on more than 160 KPIs across 509 organizations managing 63 billion dollars in services revenue. It found that the single capability separating high-performance firms from the rest is integrated real-time visibility across delivery, resources, and financials.

Moreover, EBITDA across the industry fell from 15 to 16 percent through 2023 to under 10 percent by 2025. Revenue leakage is healthy only below 5 percent. Ultimately, the firms that win are the ones that can see across the Missing Mile in real time.

Three places enterprise deals get mis-shaped

When I trace mis-shaped deals to their origin, they almost always break in one of three places.

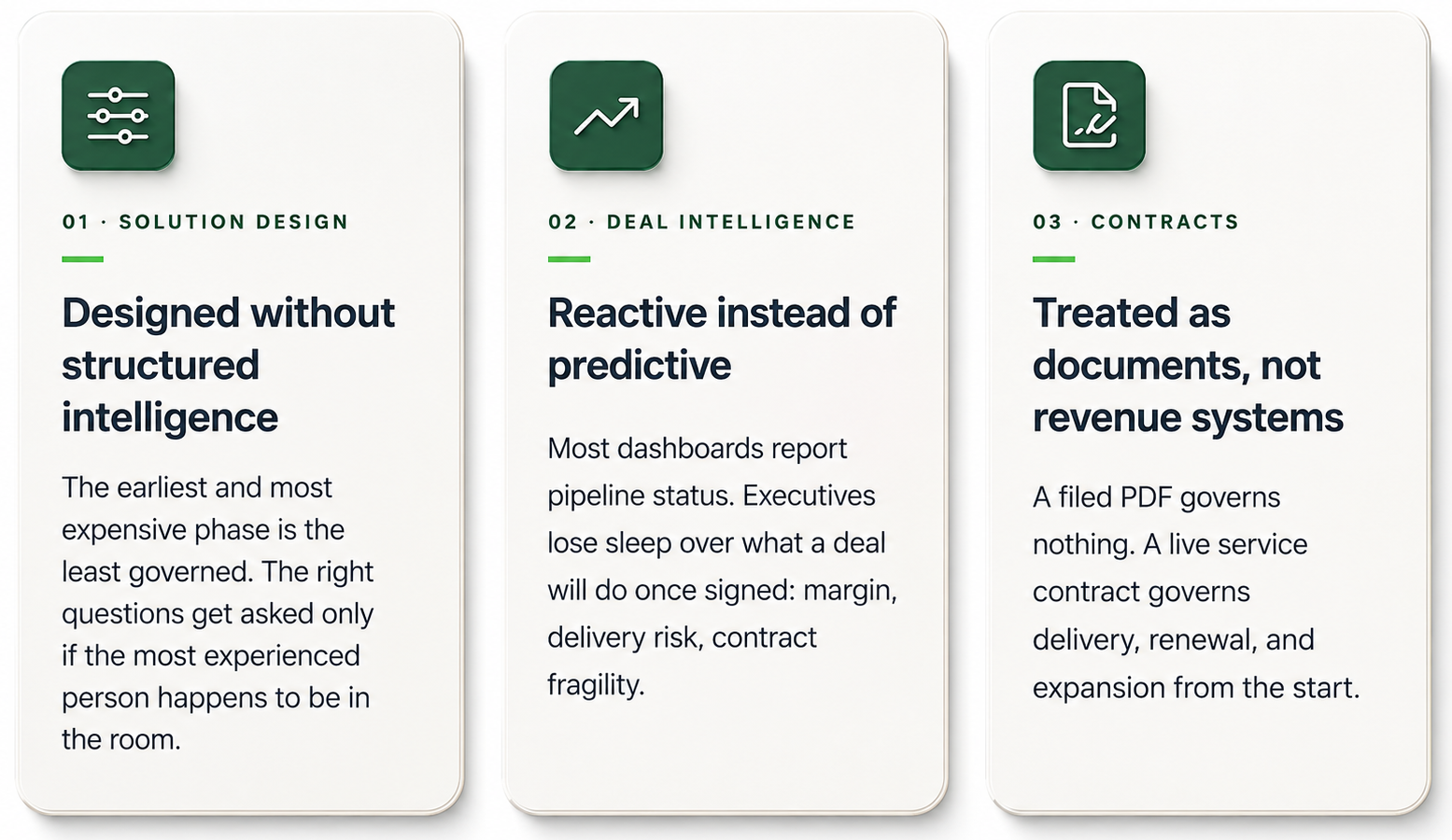

1. Solution design happens without structured intelligence

The earliest and most expensive phase of a deal is also the least governed. Solutions get shaped through fragmented discovery and informal alignment. As a result, the right questions get asked only if the most experienced person happens to be in the room.

What is missing is structured guidance during construction. In short, this is the difference between using AI to qualify a lead and using AI-assisted guided selling to design a solution. Done well, it surfaces better discovery questions, brings service and delivery requirements forward before they become surprises, and aligns technical feasibility with commercial structure while there is still time to change either.

2. Deal intelligence is reactive instead of predictive

Most dashboards report pipeline status. Stage, value, close date, probability. However, that is rear-view reporting dressed up as insight. Executives do not lose sleep over pipeline status.

Instead, they lose sleep over what a deal will do once signed: margin erosion hidden in the structure, delivery risk embedded in assumptions, contract fragility, and lifecycle value leakage. So this is the gap the servicePath™ Deal Dashboard and Deal Intelligence layer are built to close. They evaluate what a deal will do to margin, risk, delivery, and long-term revenue health before it is signed.

Furthermore, the person who cares about that question has changed. The economic buyer for quoting technology is shifting from the Chief Revenue Officer to the Chief Financial Officer, because margin governance, audit readiness, and revenue recognition now sit at the center of the deal.

For example, Deloitte’s CFO Signals found 86 percent of CFOs expect pricing to become more important over the coming year.

Similarly, Gartner Finance VP analyst Dennis Gannon describes the explicit tension finance leaders now face between cost and growth goals.

In addition, Bain finds that commercial excellence built on pricing architecture and discount governance can deliver two to three times the revenue growth of peers.

The finance climate this deal lands in

None of this happens in a vacuum. The finance leaders who now sit at the center of the deal are entering 2026 under real pressure. Indeed, their own words explain why deal construction has become a finance problem.

For example, Amy Dickerson, EVP, CFO and CHRO at Regenesis, calls 2026 a hold steady kind of year, with more planning on deck.

Similarly, Armanino partner Dean Quiambao notes that even growth-oriented businesses are being forced to justify expansion with unit economics.

So when growth must be justified deal by deal on unit economics, a quote nobody margin-tested before signature is no longer a sales inconvenience. It is a finance liability.

At the same time, the CFO’s mandate is widening. For instance, CFO.com describes the rise of platform CFOs, finance leaders acting as orchestrators of cross-functional growth rather than stewards of reporting. That is exactly why finance now wants visibility into the deal while it is being built.

Likewise, BCG’s transformation research captures the same instinct. Tom Casey, former CFO at Lending Club, calls the modern finance chief the chief storyteller for transformation.

Meanwhile, Jeff Elliott, former CFO at Exact Sciences, frames the two questions any change must answer: the first is why, the second is what’s in it for me.

Finally, EY’s Myles Corson pushes leaders to challenge how robust their scenario planning really is against shocks that arrive at speed. In short, a deal whose margin and delivery risk stay invisible until after signature fails every one of those tests at once.

3. Contracts are treated as documents instead of revenue systems

This is the most expensive misconception in enterprise revenue. Typically, we treat the signed contract as a legal artifact, file it, and move on. But in a service-led business, a contract is a living commercial system.

The strongest organizations turn it into a service contract that actively governs the relationship: ongoing revenue realization, delivery execution, renewal and expansion pathways, and lifecycle revenue continuity. When that system is left ungoverned, the cost compounds quietly.

In fact, that is exactly the leakage the 2026 benchmark puts at up to 5 percent of services revenue even in a good year. Similarly, TSIA describes the shift from selling units of transactions to value realization across renewal and expansion.

Revenue is not a funnel. It is a continuous system.

Each failure point is really a break in one chain. Modern enterprise revenue is no longer a funnel that ends at signature. Instead, it is a continuous system: Opportunity, to Solution Design, to Guided Configuration, to Quote, to Contract, to service contract, to Delivery, to Renewal, to Expansion.

Every break in that chain is where margin, time, and customer value are lost. For example, manage each stage in a different tool, owned by a different team, and the breaks are guaranteed. Therefore, Revenue Lifecycle Management makes the chain one governed system instead of nine disconnected ones.

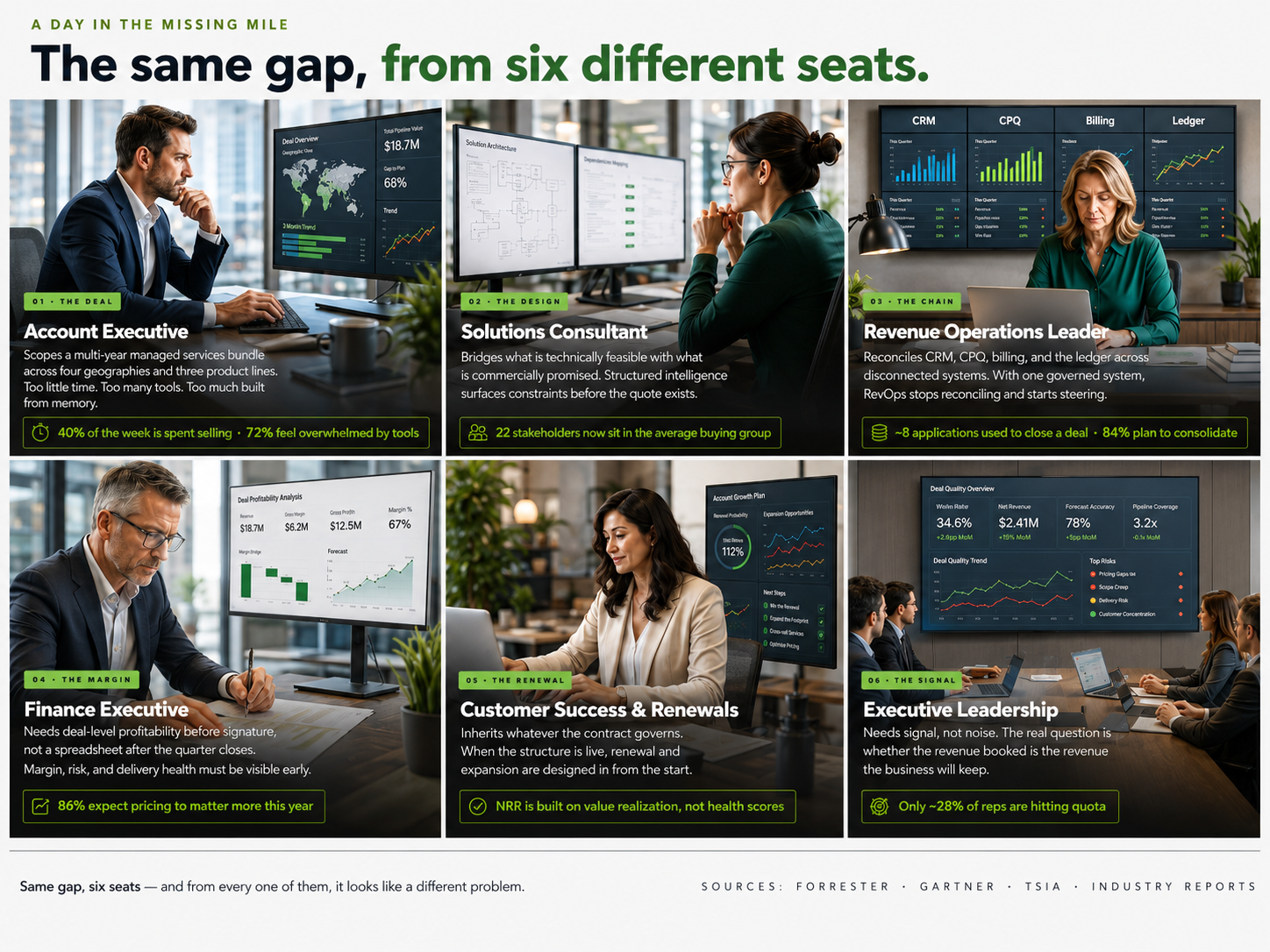

The same gap, six seats

The Missing Mile is abstract until you watch it show up in someone’s workday. Because the same gap looks different from every seat, it stays invisible. So let us walk it around the table.

The account executive

Picture an AE scoping a multi-year managed services bundle across four geographies, three product lines, and a delivery team they have never met.

They are not short on effort. Rather, they are short on time and structure. For example, sellers now spend only about 40 percent of their week actually selling, according to Salesforce’s 2026 State of Sales report.

The same report found that 72 percent of sellers feel overwhelmed by their tools, and that overwhelmed sellers are 45 percent less likely to hit quota.

So the AE does what the calendar forces. They assemble the deal from memory, price it on instinct, and ship it. As a result, the unpriced delivery dependency does not show up until the first delivery review. However, with AI-assisted guided selling, that risk surfaces while the deal can still be reshaped.

As Salesforce’s EVP of Sales Adam Alfano put it, the aim is to kill the busywork so our teams can focus on what actually moves deals forward. In short, servicePath™ puts that intelligence at the point of design, not the post mortem.

The solutions consultant

The SC is the line between a solution that holds and one that looks elegant in the proposal but falls apart in delivery. Their daily tension is that technical feasibility and commercial structure are decided in different rooms, sometimes weeks apart.

Moreover, with buying groups now averaging 22 stakeholders (Forrester, 2026), requirements arrive fragmented and contradictory. Therefore, structured intelligence during design closes that gap. It surfaces service and delivery requirements and feasibility constraints before the quote exists.

The revenue operations leader

RevOps owns the whole chain, yet is handed none of the tools to govern it as one. For example, the average rep now uses roughly eight applications to close a deal.

In addition, Salesforce’s 2026 research found that 84 percent of teams without a unified platform plan to consolidate, because the disconnection has become the bottleneck.

So RevOps is the role most likely to see the Missing Mile, and the most frustrated by it. Day to day, they reconcile CRM against CPQ against billing against the ledger by hand. Meanwhile, the 2026 benchmark names integrated real-time visibility as the high-performer differentiator.

Give RevOps one governed system, then, and they stop reconciling and start steering.

The finance executive

The CFO has moved from the end of the process to the center of it, accountable for the margin a deal will actually produce. However, the tooling hands them a spreadsheet forecast assembled after the quarter closes, when nothing can be changed.

As noted, Gartner Finance analyst Dennis Gannon describes the explicit tension finance leaders now carry between cost discipline and growth.

Likewise, Deloitte reports that 86 percent of CFOs expect pricing to matter more this year.

So this CFO wants deal-level profitability before signature, not a reconciliation after it. Ultimately, Deal Intelligence that scores margin, risk, and delivery health at the moment of construction separates a finance leader who governs the deal from one who explains the miss.

The customer success and renewals leader

This team inherits whatever the contract governs, and usually it governs nothing. For instance, TSIA’s research is clear that net revenue retention in 2026 is built on value realization, not health scores.

Furthermore, the shift from selling units of transactions to selling value realization runs straight through renewal and expansion. So when the signed structure is a filed PDF, every renewal is a renegotiation from zero.

By contrast, when it is a live service contract, renewal and expansion are designed in from the start. As a result, customer success manages a revenue system rather than chasing a document.

Executive leadership

Leaders need none of the detail and all of the signal. For example, with only around 28 percent of reps hitting quota and EBITDA compressed across the services industry (2026 benchmark), the question that matters is forecast confidence. In other words, is the revenue we booked the revenue we will keep.

A pipeline-status dashboard answers the wrong question. Instead, a Deal Dashboard lets leadership read margin quality, risk exposure, and contract integrity directly. So the conversation becomes about the shape of the revenue, not the status of the pipeline.

Why the gap stays invisible

Six seats. One gap. And here is why it stays invisible: the Missing Mile is nobody’s job, because it is everybody’s edge. Each role sees only the slice that lands on their desk.

The AE sees the scramble, finance sees the miss, and customer success sees the hard renewal. Yet no one sees the whole break, so no one owns it. In short, a gap that belongs to everyone is governed by no one. Therefore, a platform that closes it has to serve all six as a single governed system.

A note on AI, because the timing decides who wins

Every services business is now racing to put AI into its commercial process. For example, a January 2026 IDC study found that 68 percent of organizations are already scaling or optimizing AI across revenue functions.

As IDC’s Michelle Morgan puts it, agentic AI represents a structural change in how revenue teams operate.

Furthermore, Gartner expects 40 percent of enterprise applications to embed task-specific AI agents by the end of 2026, up from less than 5 percent a year earlier.

I am all for it. However, the uncomfortable truth connects straight to the Missing Mile, and it should stop every revenue leader cold.

For thirty years, the Missing Mile has been expensive but slow, because a human still had to make each ungoverned pricing call by hand. That capped the damage. But AI removes the cap. So when you point a model at an ungoverned Missing Mile, you do not get better decisions.

Instead, you get your worst decisions, the same mis-shaped deals you have always made, now produced at machine speed and machine scale, with machine confidence, and signed before anyone can object.

In short, AI does not fix the Missing Mile. It industrializes it.

As CFO Dive has observed, AI performs best against structured, reliable data, and cannot fix an operating model that is manual and disconnected. Therefore, governance is not the thing you bolt on after the AI project. Rather, it is the precondition for the project being worth doing at all. First, build the governed revenue architecture. Then let agents operate inside guardrails your CFO and your auditor can inspect.

Why this matters now

The shift from quoting tool to revenue lifecycle system is no longer a prediction. In fact, it is documented in the category’s definitive reference.

In its Magic Quadrant for Configure, Price and Quote Applications, published 22 January 2026 by analysts Luke Tipping and Mark Lewis, Gartner describes a market evolving toward solutions that support selling all types of goods and services, not just producing a faster quote.

Moreover, the vendors are reorganizing around it in public.

For instance, Conga’s acquisition of PROS B2B was explicitly about connecting pricing, quoting, and contracting so teams can make smarter decisions from price to signature, in CEO Dave Osborne’s words.

So when the largest players are all racing to connect the same chain, the question is no longer whether enterprise revenue is becoming a governed lifecycle. Instead, it is which platforms were built for it, and which are retrofitting a connected story onto tools that began as product-only quoting engines.

Why servicePath™ is built for this

servicePath™ is not another configure, price, quote tool. Instead, it is a Revenue Lifecycle Management platform for complex, service-led revenue.

A CPQ tool helps you produce a correct quote. By contrast, servicePath™ helps you shape a sound deal with AI-assisted guided selling, score its margin and delivery health before signature through Deal Intelligence and the Deal Dashboard, and keep the signed structure live as a service contract.

In effect, it sits in the Missing Mile, between CRM and ERP, governing the deal logic that has lived in spreadsheets for too long.

That is why Gartner has recognized servicePath™ as a Visionary in its Magic Quadrant for Configure, Price and Quote Applications. In addition, independent buyers ranked it a SoftwareReviews CPQ Triple Crown winner.

Enterprises such as Dell, telent, Telefónica, ATOS, TierPoint, and Park Place Technologies also trust it to cut proposal cycles by as much as 90 percent. Ultimately, the recognition matters less for the badge than for what it reflects: a platform built, from the start, to govern the whole revenue lifecycle rather than to speed up one step of it.

Take Dell EMC. After an extensive evaluation, its sales engineering team chose servicePath™. As a result, complex proposal changes that once took a full day now take about 15 minutes.

That is a 98 percent reduction. At the same time, partners gained the ability to generate their own configurations and quotes. The full account is in the Dell EMC case study.

Frequently asked questions

What is the Missing Mile in enterprise revenue?

The Missing Mile is the ungoverned gap between what sales quoted and what finance can actually explain. In practice, it is the space between CRM and ERP where pricing, discounts, scope, and contract terms are decided, usually in spreadsheets. Because no system governs it, margin quietly leaks.

Why do most complex enterprise deals fail?

They are not lost to competitors or to price. Instead, they are mis-shaped during solution design, long before the proposal. For example, with an average of 22 stakeholders shaping a purchase, the deal takes its shape early. As a result, a structurally flawed deal cannot be recovered in the negotiation.

What is Revenue Lifecycle Management, and how is it different from CPQ?

CPQ produces an accurate quote. By contrast, Revenue Lifecycle Management governs the entire chain from opportunity through solution design, quote, contract, delivery, renewal, and expansion as one connected system. Notably, Gartner’s 2026 CPQ Magic Quadrant documents the market evolving in exactly this direction.

What is servicePath™?

servicePath™ is a Revenue Lifecycle Management platform for complex, service-led revenue. Moreover, it is recognized as a Visionary in Gartner’s Magic Quadrant for CPQ Applications and trusted by enterprises including Dell, Telefonica, Telent, TierPoint and Park Place Technologies.

Related reading from servicePath™

- Revenue Architecture 2.0: human-led CPQ for 2026 explains why the CPQ layer, not the CRM, should act as the control plane for enterprise revenue.

- The revenue gap between CRM and ERP goes deeper on the Missing Mile, the spreadsheet layer where margin quietly leaks.

- AI-native, codeless CPQ and the 2026 CIO agenda covers how to operationalize AI across the revenue lifecycle without custom code.

- Salesforce CPQ end-of-sale: what it means for revenue operations lays out the decision window that legacy CPQ users now face.

- servicePath™ wins the 2025 CPQ Triple Crown details the independent Software Reviews recognition behind the platform.

Key terms

For definitions of the concepts in this article, see the servicePath™ glossary: Configure, Price, Quote (CPQ), Quote-to-Cash, Lead-to-Cash, Service Contracts, Composable Revenue Architecture, and Revenue Engine.

The real takeaway

If the pattern here is right, and both the analyst evidence and the market’s behavior suggest it is, then most enterprise deals are being lost long before they are visible. Not in pricing. Not in negotiation. Instead, in how they are constructed, and in whether anyone governs the Missing Mile between the quote and the ledger.

So before your team’s next significant deal reaches paper, ask three questions:

- Is this solution being designed with structured guidance, or assembled from memory?

- Do we know its margin, risk, and delivery health before we sign, or only after?

- Will the signed structure govern delivery and renewal, or just sit in a folder?

If your team cannot answer all three with confidence, then the deal is already at risk of being mis-shaped. Fortunately, you still have time to do something about it. After all, that window, before paper, is the most valuable and least governed real estate in your revenue process.

So stop watching the room where deals are won and lost. Instead, start governing the Missing Mile where they are shaped. Ultimately, that is where the revenue actually lives.

Find your Missing Mile before your next deal does

See how servicePath™ scores margin, risk, and delivery health before signature, and keeps the contract live across the whole lifecycle.

1. Keep reading

Go deeper on the revenue architecture.

The Missing Mile is one piece. See how the CPQ layer, not the CRM, becomes the control plane for enterprise revenue.

Read Revenue Architecture 2.0

2. Salesforce CPQ alternative

On legacy Salesforce CPQ? The clock is running.

Salesforce CPQ is end-of-sale. See what a Revenue Lifecycle Management platform does that a retrofitted quoting tool cannot.

See the Salesforce CPQ alternative

3. Explore the glossary

New to the language of revenue lifecycle? Start with the terms.

Every concept in this article, defined in the servicePath™ glossary.

Explore the glossary

4. The CRM-to-ERP gap

See exactly where margin leaks between your systems. A deeper look at the Missing Mile, the ungoverned layer between CRM and ERP.

See the CRM to ERP gap