Table of Contents

- Executive Summary

- Why Revenue Architecture Has Become the Growth Constraint

- Four Forces Driving the Revenue Architecture Imperative

- How Revenue Architecture Gaps Create Compounding Risk

- Proof Point: How Dell EMC Transformed Partner Commerce

- How the Market Is Evaluating Commercial Platforms

- The Emerging Revenue Architecture Pattern

- Revenue Architecture Lessons From Experience

- Revenue Architecture Questions for CEOs and Boards

- Revenue Architecture: The Next Decade of Advantage

- Frequently Asked Questions

- References

Executive Summary

In the last eighteen months, I’ve had the same conversation with dozens of CEOs.

The symptoms vary — margin erosion, stalled integrations, misaligned incentives — but the diagnosis is always the same: their commercial architecture can’t keep pace with their strategy.

The commercial systems that powered the last decade of growth are now constraining the next decade of value creation. Across private equity portfolios, global enterprises, and acquisitive organizations, a structural tension has emerged: strategy moves faster than systems. Pricing changes take months to propagate. Acquisitions close but revenue logic remains fragmented. AI pilots launch but governance frameworks lag. Sales demands velocity while finance demands predictability.

This paper introduces the concept of Revenue Latency — the measurable delay between commercial intent and commercial execution — and argues that reducing it has become a board-level imperative.

Key findings from leading research firms underscore the urgency:

Below are key findings from leading research firms that underscore the urgency:

- Pricing confidence premium: Companies confident in their pricing capabilities achieve 5–11 percentage point profit margin premiums over peers (Bain & Company, 2025)

- Price realization leverage: A 1% improvement in price realization translates to approximately 11% operating profit uplift (McKinsey)

- Alignment gap: 92% of executives cite internal misalignment as a barrier to growth, yet only 21% take corrective action (Harvard Business Review Analytic Services & Varicent, 2024)

- M&A acceleration: Global M&A reached $4.7 trillion in 2025 (+43% YoY), with AI-enabled integration reducing costs by 20% and timelines by 30–50% (McKinsey)

- AI governance gap: 74% of organizations expect AI to drive revenue growth, but only 20% are achieving it (Deloitte, 2026)

- RevOps advantage: Mature revenue operations organizations achieve 36% more revenue and 28% greater profitability (Forrester)

- Sales cycle impact: Companies with optimized commercial systems experience 28% shorter sales cycles and 105% larger average deal sizes (Aberdeen Group)

Notably, the global CPQ market — a proxy for revenue architecture investment — is projected to reach $5.8 billion in 2026, growing at 16% annually, according to MGI Research. Undoubtedly, this growth reflects a fundamental shift: enterprises are treating revenue architecture as a strategic asset rather than an operational afterthought.

As a result, this paper outlines the four structural forces driving this imperative, the architectural patterns emerging among market leaders, and the questions every CEO and board should be asking about their revenue architecture.

The average complex enterprise leaks 3–7% of addressable margin through revenue architecture gaps. Most boards don’t realize it’s happening until a PE firm points it out during diligence — or until a competitor with better commercial infrastructure wins a deal that should have been theirs.

In reality, enterprise leaders rarely lose sleep over quoting tools. Instead, they lose sleep over margin volatility, stalled integrations, unpredictable renewals, and misalignment between sales ambition and financial control.

And increasingly, those issues trace back to something less visible but more consequential: revenue architecture.

Specifically, across private equity portfolios, global managed service providers, enterprise software companies, and complex services organizations, a structural pattern is emerging:

Strategy is moving faster than systems.

- Pricing strategy evolves — but implementation takes months

- Meanwhile, acquisitions close — but revenue logic remains fragmented

- Similarly, AI pilots launch — but governance frameworks lag

- And sales is pushed for velocity — while finance demands predictability

Clearly, this gap is not operational friction. Rather, it is structural. Moreover, in today’s market, revenue architecture misalignment compounds into measurable enterprise value erosion.

For example, consider the math: Salesforce research shows the average sales representative spends only 28% of their week actually selling. Unfortunately, the rest disappears into administrative tasks, manual data entry, quote revisions, and approval chasing. For organizations with complex product configurations and hybrid pricing models, that number is often worse. Ultimately, every hour spent wrestling with spreadsheets is an hour not spent with customers.

Why Revenue Architecture Has Become the Growth Constraint

Historically, for much of the last decade, growth constraints were external: market demand, competitive positioning, capital availability.

Today, however, for complex enterprises, growth is increasingly constrained internally — by the speed, coherence, and governance of commercial execution. In other words, the bottleneck has moved from market opportunity to revenue architecture capability.

The Margin Premium of Pricing Confidence

Bain & Company’s 2025 Commercial Excellence research shows that companies confident in their pricing capabilities achieve profit margin premiums of 5 to 11 percentage points over peers. That’s not a rounding error — for a $500 million enterprise, that’s $25–55 million in annual margin at stake.

Similarly, McKinsey’s pricing analysis consistently demonstrates that a 1% improvement in price realization can translate into roughly 11% uplift in operating profit — more leverage than equivalent improvements in volume or cost.

Clearly, those numbers are not marginal improvements. Rather, they are valuation multipliers.

Yet many enterprises still rely on fragmented pricing logic embedded separately inside multiple CRM, CPQ, ERP, and billing systems — creating latency between commercial intent and execution. Fundamentally, this is a revenue architecture failure.

What is Revenue Latency?

Revenue Latency is the measurable delay between commercial strategy and system-level execution. It is the silent killer of enterprise value. At scale, Revenue Latency compounds silently: margin leakage through inconsistent discounting, missed cross-sell and upsell opportunities, billing errors during mid-term contract changes, integration delays during M&A, and AI deployments stalled by governance risk.

The Competitive Impact of System Alignment

Aberdeen Group research quantifies the impact: companies using optimized commercial systems experience a 28% shorter sales cycle and 105% larger average deal sizes compared to those relying on manual processes. Essentially, that’s the difference between winning and losing in competitive markets.

Furthermore, KPMG and CMO Council research indicates that over 70% of marketers say fragmented technology across marketing, sales, and service restrains better sales-marketing alignment — a structural barrier that directly impacts revenue capture.

Additionally, Harvard Business Review research reports that 92% of executives cite internal misalignment as a barrier to growth — yet only 21% take meaningful corrective action.

Unfortunately, the gap between awareness and revenue architecture response is widening. The question is no longer whether revenue architecture matters — rather, it’s whether your organization will address it before your competitors do.

Four Forces Driving the Revenue Architecture Imperative

Importantly, this moment is distinct because four forces are converging simultaneously. Understanding each is essential for any executive navigating revenue architecture transformation.

1. Margin Discipline Has Replaced Growth-at-Any-Cost

First, the capital environment has shifted dramatically. Inflation-based pricing justification is fading. Moreover, interest rates and valuation scrutiny are higher than they’ve been in over a decade.

As a consequence, boards are asking sharper questions: How disciplined is pricing governance? Are discount thresholds enforced systemically? Is cost-to-serve embedded in quoting workflows?

Bain confirms that pricing leaders outperform reactive competitors not only in margin, but also in revenue growth rates. Therefore, pricing precision is now a strategic lever — not a tactical adjustment.

In short, the organizations that treat pricing as a core competency — with real-time governance, systematic enforcement, and continuous optimization — are pulling ahead. Conversely, those that treat it as a spreadsheet exercise are falling behind.

2. M&A Integration Timelines Have Compressed

Second, global M&A activity reached $4.7 trillion in 2025, according to McKinsey — up 43% year-over-year and significantly above the 10-year average.

However, integration timelines have shortened dramatically. Boards increasingly expect synergy realization within 90–120 days — not 18 months.

Nevertheless, CRM consolidation often becomes the bottleneck. Traditional “standardize everything” approaches require forced migration, freeze sales productivity, and delay revenue synergies. As a result, the promise of M&A value gets trapped in integration complexity.

McKinsey reports that organizations applying AI and structured integration frameworks can reduce M&A costs by approximately 20% and accelerate timelines by 30–50%. But those gains depend on unified commercial logic across systems — something most enterprises lack.

Thus, the strategic question is no longer: “How do we migrate systems?” Instead, it is: “How do we orchestrate revenue architecture across what already exists?”

Ultimately, that is an architectural decision. And it’s one that separates successful acquirers from those who destroy value through integration paralysis.

3. The Multi-CRM Reality Is Structural

Third, the “single source of truth” mandate was logical in theory. However, in federated enterprises and acquisitive organizations, it has proven unrealistic — and often destructive.

In practice, Salesforce, Dynamics, HubSpot — and multiple regional instances — now coexist across business units. In fact, forcing consolidation often costs millions and disrupts sales productivity for quarters. In contrast, the cure becomes worse than the disease.

Let me be direct: forced CRM consolidation is one of the most expensive mistakes in enterprise software. It promises simplicity and delivers paralysis. The enterprises winning today aren’t consolidating — they’re federating.

Therefore, revenue architecture must assume CRM plurality as a design constraint, not a problem to be eliminated. The emerging architectural response is federation — centralized commercial logic with distributed execution.

4. AI Without Governance Introduces Risk

Fourth, AI is entering pricing workflows, bundle recommendations, renewal forecasting, and contract configuration. The opportunity is real — but so is the risk.

Deloitte’s 2026 State of AI in the Enterprise report shows that while 74% of organizations expect AI to drive revenue growth, only 20% are achieving measurable revenue impact. Notably, the gap is not technological capability. Rather, it is governance maturity.

Furthermore, Gartner predicts that 40% of enterprise applications will incorporate task-specific AI agents by 2026, up from less than 5% in 2025. Evidently, the velocity of AI adoption is accelerating, but governance infrastructure is not keeping pace.

Without question, modern revenue architecture requires that commercial AI operate within margin floors, regulatory caps, approval hierarchies, and cost-to-serve constraints.

AI must be probabilistic in insight — but deterministic in enforcement. Otherwise, intelligence amplifies volatility rather than value.

How Revenue Architecture Gaps Create Compounding Risk

Typically, Revenue Latency does not present as a single failure. Instead, it manifests incrementally, often invisibly — until the damage is done:

Pricing changes delayed across systems — competitors respond faster

Meanwhile, contract amendments are manually reconciled — errors compound

Additionally, cross-sell logic remains inconsistent across CRMs — opportunities missed

At the same time, billing adjustments create margin discrepancies — finance and sales diverge

Ultimately, integration synergies get postponed — M&A value erodes

Consequently, over time, the gap between strategy and execution widens. And the cost is not neutral.

The Cost of Inaction:

Organizations that delay addressing revenue architecture gaps typically experience 2–4% annual margin erosion that compounds silently — visible only in hindsight during valuation events, refinancing, or sale processes. For a $500 million enterprise, that’s $10–20 million in enterprise value erosion per year. Over a typical PE hold period, that’s $50–100 million in unrealized value.

Forrester research indicates that mature revenue operations organizations achieve 36% more revenue and up to 28% greater profitability than less aligned peers. Importantly, the difference is not tool adoption. Rather, it is revenue architecture alignment.

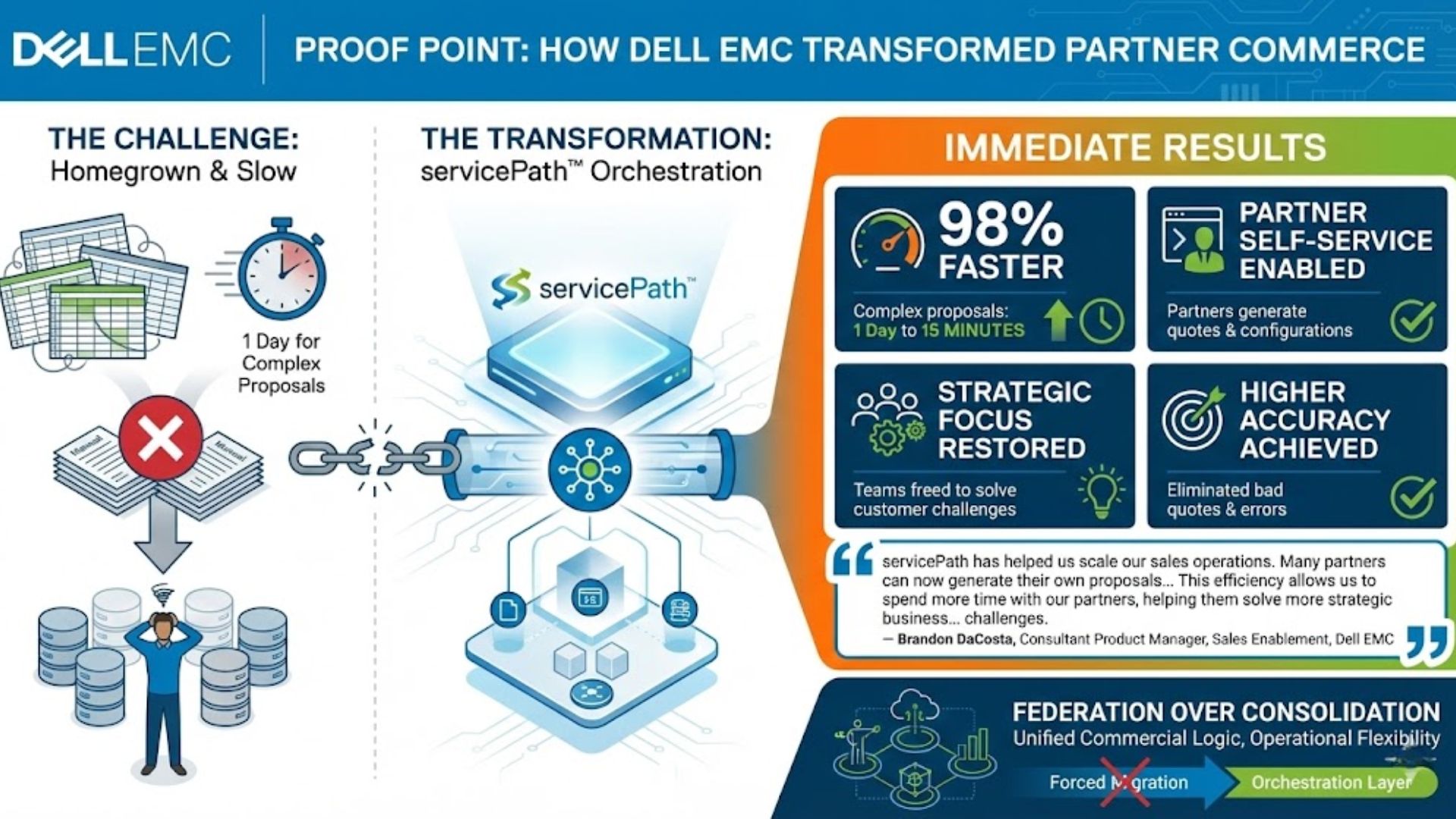

Proof Point: How Dell EMC Transformed Partner Commerce

Admittedly, theory is useful. However, results are better. To illustrate, consider the experience of Dell EMC — one of the world’s largest technology companies, serving 98% of the Fortune 500 across 180 countries.

Initially, Dell EMC’s Sales Engineering team faced a familiar challenge: their homegrown spreadsheet configurators couldn’t keep pace with their partners’ complex needs. As their offerings increased in size and scope, configuring and quoting solutions for their Managed Service Provider (MSP) partners became increasingly unwieldy. Consequently, the team realized they needed something more robust, more reliable, and more partner-centric.

Subsequently, after an extensive evaluation, Dell EMC selected servicePath™. The results were immediate and measurable:

Dell EMC Results with servicePath™:

98% faster: Complex proposals dropped from 1 day to just 15 minutes

Additionally, partner self-service enabled — partners now generate own quotes and configurations

Furthermore, strategic focus restored — teams freed from spreadsheets to solve customer challenges

Most importantly, higher accuracy achieved — eliminated bad quotes and pricing errors

“servicePath has helped us scale our sales operations. Many partners can now generate their own proposals and configurations using the platform. This efficiency allows us to spend more time with our partners, helping them solve more strategic business and technology challenges.”— Brandon DaCosta, Consultant Product Manager, Sales Enablement, Dell EMC

Overall, the Dell EMC implementation illustrates a broader pattern: revenue architecture transformation delivers fastest time-to-value when it embraces federation rather than forced consolidation. Specifically, Dell EMC didn’t rip out their existing systems. Instead, they added an orchestration layer that unified commercial logic while preserving operational flexibility.

How the Market Is Evaluating Commercial Platforms

Admittedly, in a crowded CPQ and revenue operations landscape, feature claims are abundant. However, objective evaluation remains scarce.

One reason the Gartner Magic Quadrant remains influential for executive buyers is methodological rigor. Unlike popularity-based rankings, Gartner requires vendors to demonstrate real capabilities under structured, comparable evaluation scenarios — assessing configuration depth, pricing logic, governance enforcement, lifecycle handling, and AI explainability.

Simply put, revenue architecture cannot be evaluated through slideware. It must be demonstrated.

In the January 2026 Gartner Magic Quadrant for CPQ Applications, 16 vendors were evaluated under such structured criteria.

That recognition reflects something larger than product capability. It signals that the market is beginning to reward revenue architecture thinking over feature accumulation.

Therefore, executives evaluating commercial platforms should apply similar rigor: Was governance demonstrated, not assumed? Was multi-system orchestration proven? Were AI recommendations auditable? Was contract lifecycle complexity tested under real conditions?

Essentially, those questions differentiate revenue architecture decisions from tactical upgrades.

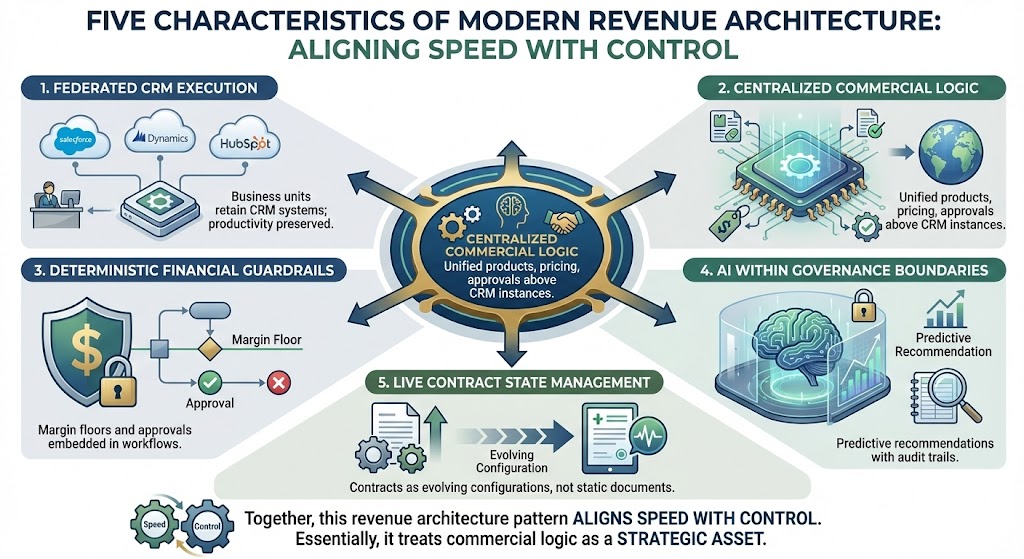

The Emerging Revenue Architecture Pattern

Consistently, across enterprises successfully reducing Revenue Latency, a consistent revenue architecture model is emerging. It includes five characteristics:

Five Characteristics of Modern Revenue Architecture:

Consistently, across enterprises successfully reducing Revenue Latency, a consistent revenue architecture model is emerging. Specifically, it includes five characteristics:

First, Federated CRM Execution — Business units retain CRM systems; productivity preserved

Second, Centralized Commercial Logic — Unified products, pricing, approvals above CRM instances

Third, Deterministic Financial Guardrails — Margin floors and approvals embedded in workflows

Fourth, AI Within Governance Boundaries — Predictive recommendations with audit trails

Finally, Live Contract State Management — Contracts as evolving configurations, not static documents

Together, this revenue architecture pattern aligns speed with control. Essentially, it treats commercial logic as a strategic asset.

This is not theory. Rather, it is operational reality for enterprises including Dell Technologies, Telefónica, TierPoint, Park Place Technologies, and telent — organizations that have made revenue architecture a strategic priority.

Revenue Architecture Lessons From Experience

Throughout years of working with complex enterprises navigating M&A integration, hybrid pricing, and managed service contracts, one lesson repeats:

Revenue architecture transformation fails when it’s treated as an implementation detail. Conversely, it succeeds when governance, flexibility, and velocity are designed together.

Understandably, the temptation in commercial transformation is to focus on interface improvements and incremental workflow automation. However, the harder — but more consequential — work is rethinking where commercial logic lives and how it is governed.

Gartner’s CIO Agenda research identifies application modernization as a top priority for 71% of CIOs. But modernization divorced from revenue impact misses the point.

Make no mistake: revenue architecture is not an IT initiative. It is a margin initiative. It is an integration initiative. It is a board-level decision.

Revenue Architecture Questions for CEOs and Boards

Accordingly, if you are leading a complex enterprise, consider these diagnostic questions:

Start with pricing governance:

How long does it take to implement a pricing change across all revenue systems?

Do finance and sales operate on a shared definition of margin?

Then examine integration capability:

Can we integrate an acquisition without forcing CRM migration?

Is our commercial logic centralized — or fragmented across platforms?

Finally, assess operational efficiency:

Are AI-driven pricing recommendations explainable under audit?

Are contract amendments executed cleanly — or manually reconciled?

What percentage of our sales reps’ time is spent actually selling versus administering quotes?

Importantly, if multiple questions generate discomfort, the issue is structural. Revenue architecture gaps rarely resolve themselves — instead, they compound.

Revenue Architecture: The Next Decade of Advantage

Without doubt, the competitive landscape is shifting. Revenue growth alone is insufficient.

Specifically, the winners of the next decade will combine velocity with governance — agility with discipline. They will treat revenue architecture as a strategic asset. Moreover, they will design systems that reflect how modern enterprises actually operate: federated, acquisitive, AI-enabled, and margin-conscious.

Deliberately, they will reduce Revenue Latency.

And thereby, in doing so, they will align strategy and execution in a way that compounds over time — creating sustainable competitive advantage that competitors cannot easily replicate.

Admittedly, revenue architecture may not be visible to customers. But its impact is visible in margin, integration speed, renewal strength, and enterprise value.

That makes it a CEO conversation.

Frequently Asked Questions ( FAQs)

What is Revenue Latency, and why does it matter for revenue architecture?

Revenue Latency is the measurable delay between commercial intent and commercial execution — the time it takes for a pricing strategy change, product configuration update, or governance rule to propagate across all revenue systems.

Essentially, it matters because latency creates margin leakage, missed opportunities, and competitive disadvantage. In fact, research shows that 50% of buyers choose the vendor that responds first. Therefore, when your competitor can implement a pricing change in hours while you require weeks, they win deals you should have won. Modern revenue architecture eliminates this latency.

How long does it typically take to see ROI from revenue architecture transformation?

Typically, most implementations demonstrate measurable impact within the first 90 days, with full platform payback occurring within 6–9 months.

Specifically, the primary value drivers include: reduced quote cycle time (organizations commonly see 90%+ reduction in quote generation time), improved pricing accuracy and margin protection, accelerated M&A integration (unified commercial logic within 60 days of close), and increased sales productivity through automation of administrative tasks.

For example, Dell EMC reduced complex proposal changes from a full day to 15 minutes — a 98% improvement that translated directly into faster deal velocity and partner satisfaction.

Does revenue architecture transformation require CRM consolidation?

No — and this is a critical distinction. Unfortunately, traditional approaches require forced CRM migration, which is expensive, disruptive, and often destroys more value than it creates.

Instead, modern revenue architecture assumes CRM plurality as a design constraint. The architectural pattern that’s emerging among market leaders involves federating CRM execution while centralizing commercial logic — products, pricing rules, approval workflows, and cost-to-serve models are governed in a unified layer above CRM instances.

Consequently, this allows business units to retain operational systems that work for them while ensuring consistent pricing, governance, and reporting across the enterprise. servicePath™ was designed specifically for this multi-CRM reality.

How does AI fit into revenue architecture, and how do we manage the risk?

AI is increasingly embedded in pricing recommendations, bundle optimization, renewal forecasting, and contract configuration. Gartner predicts 40% of enterprise applications will incorporate AI agents by 2026.

Nevertheless, the risk is equally real: AI without governance introduces compliance, audit, and margin exposure. Therefore, the key principle is that AI must be probabilistic in insight but deterministic in enforcement.

In practice, this means AI can recommend optimal pricing or configuration, but those recommendations must operate within explicit guardrails: margin floors, regulatory caps, approval thresholds, and audit requirements. Importantly, every AI-influenced decision should be explainable and auditable. servicePath™’s revenue architecture embeds this principle: AI augments decision-making while governance ensures compliance and control.

Continue the Conversation

If this paper surfaced questions about your own commercial infrastructure, I want to hear them.

Executive Briefing

I offer 30-minute executive briefings for seniorleadership. In that time, I’ll help you assess whether Revenue Latency is eroding your enterprise value — and whether servicePath™ is the right solution to address it. If it’s not, I’ll tell you that too.

To schedule: Email daniel.kube@servicepath.co with “Executive Briefing” in the subject line.

Talk to a CPQ Specialist

See servicePath™ in action. Our product specialists will walk you through a live demonstration tailored to your industry, showing how enterprises like Dell Technologies, Telefónica, and TierPoint have reduced Revenue Latency and transformed their commercial operations.

Subscribe to Executive Conversations

Join CEOs, CFOs, and CROs who receive my insights on commercial architecture, revenue operations, and the strategic decisions shaping enterprise value creation.

No spam. No fluff. Just the strategic perspectives that matter to executive leadership.

Listen to Our Podcasts

Hear directly from industry leaders, PE operating partners, and enterprise executives on the challenges and opportunities in commercial transformation.

Explore Our Whitepapers & Reports

Dive deeper into the topics covered in this paper. Our resource library includes:

CPQ Vendor Comparison Matrix — Compare top CPQ vendors side-by-side with ratings, features, and industry focus

A Day in the Life of a Sales Manager — See how CPQ transforms quote processes and accelerates sales cycles

Executive Sales Quoting Process Questionnaire — Identify hidden inefficiencies and assess CPQ readiness

The CPQ Solution Study — In-depth analysis of the CPQ landscape, trends, and vendor insights

Mastering Complexity in Technology Sales — How modern CPQ systems turn complexity into competitive advantage

Explore Whitepapers & Reports →

Learn About Our Gartner Recognition

servicePath™ has been named the sole Visionary in the 2026 Gartner Magic Quadrant for CPQ Applications — for the fourth consecutive year. Learn what this recognition means and why Gartner positioned servicePath™ apart from 15 other vendors.

Visit Our Glossary

New to CPQ, revenue architecture, or commercial transformation terminology? Our comprehensive glossary defines key terms used by revenue operations professionals.

About the Author

Daniel Kube is the Chief Executive Officer of servicePath™, a Configure, Price, Quote platform for mid to large tech-enabled enterprises with complex revenue models.

Over the past decade, Daniel has worked with PE-backed portfolio companies, global managed service providers, enterprise technology organizations, and complex services businesses navigating the intersection of commercial strategy and revenue operations. His work focuses on helping organizations reduce Revenue Latency — aligning pricing strategy, M&A integration, contract lifecycle management, and AI governance into coherent commercial architecture.

servicePath™ has been positioned in the Visionary quadrant of the Gartner Magic Quadrant for CPQ Applications for four consecutive years — and stands alone in that quadrant for the third consecutive year. The platform is trusted by Dell Technologies, Telefónica, TierPoint, Park Place Technologies, telent, and leading PE-backed portfolio companies across North America, Europe, and Asia-Pacific.

Connect with Daniel on LinkedIn | daniel.kube@servicepath.co

References

McKinsey & Company, The Power of Pricing

KPMG & CMO Council, Drive Revenue by Rethinking Marketing/Sales Collaboration

McKinsey & Company, 2026 M&A Trends: Navigating a Rapidly Rebounding Market

Deloitte, State of AI in the Enterprise 2026

Gartner, AI Agent Adoption Forecast, August 2025

Forrester, Revenue Operations Research

Gartner, 2026 CIO and Technology Executive Agenda

Gartner, Magic Quadrant for Configure, Price and Quote Applications, January 2026

Aberdeen Group via Experlogix, CPQ and CRM Integration Research

MGI Research, CPQ Market Summary 2026

Dell EMC servicePath™ Case Study, 2024

Quick Links

| Action | Link |

|---|---|

| Book a Demo | servicepath.co/contact |

| Subscribe to Newsletter | LinkedIn Newsletter |

| Explore Podcasts | servicepath.co/podcasts |

| Whitepapers & Reports | servicepath.co/whitepapers-guides |

| Gartner Recognition | servicepath.co/gartner-landing-page-2026 |

| Visit Glossary | servicepath.co/glossary-archive |

| Contact Daniel Kube | daniel.kube@servicepath.co |

Gartner Disclaimer

GARTNER and MAGIC QUADRANT are registered trademarks and service marks of Gartner, Inc. and/or its affiliates in the U.S. and internationally and are used herein with permission. All rights reserved.

Gartner does not endorse any vendor, product or service depicted in its research publications and does not advise technology users to select only those vendors with the highest ratings or other designation. Gartner research publications consist of the opinions of Gartner’s research organization and should not be construed as statements of fact. Gartner disclaims all warranties, expressed or implied, with respect to this research, including any warranties of merchantability or fitness for a particular purpose.

© 2026 servicePath™. All rights reserved.