The Problem Isn’t AI — It’s Where You Let It Decide.

By Daniel Kube, CEO, servicePath™ | 15 min read

Executive Summary

Somewhere in your revenue process right now, an AI agent may be influencing a pricing decision it was never designed to make. You will not find this in a dashboard. Nor will it trigger an alert. But over the next twelve months, it will quietly erode your margins, fragment your contracts, and compromise your ability to pass an audit.

Why This Matters Now

I have spent over two decades building at the intersection of enterprise technology, revenue operations, and complex pricing. During that time, I have watched enterprises lose millions to problems far simpler than this one. However, what I am seeing now is different — and it is accelerating.

The Core Distinction

The entire industry is racing to move logic out of CRM and into AI-driven systems. In many cases, that is exactly the right move. But there is a critical distinction being lost in the speed: not all logic is the same.

Specifically, adaptive logic — lead routing, scoring, workflow automation — thrives under AI. Therefore, it should move. On the other hand, deterministic financial logic — pricing calculations, discount enforcement, contract structures, margin protection — must produce the same result every time. Consequently, it cannot be left to probabilistic inference. Ever.

The 12-Month Risk Timeline

The enterprises conflating these two types of logic are introducing a class of AI revenue risk that does not announce itself. Instead, it shows up as subtle pricing inconsistencies in Month 1. Then margin drift appears by Month 3.

After that, contract fragmentation sets in by Month 6. Subsequently, audit failure surfaces by Month 9. Finally, board-level exposure becomes visible by Month 12. I have mapped this timeline in detail below, because I have watched versions of it play out — and the organizations that caught it late paid dearly.

The Fix

The fix is not less AI. Rather, it is better architecture. Essentially, a four-layer revenue stack where AI proposes, deterministic systems execute, CRM records, and finance reconciles. The enterprises already building this way are not slowing down. Instead, they are scaling faster — because they can trust what the system produces. Moreover, they are not just protecting margin. They are building the foundation to scale AI more aggressively than anyone around them.

If you are a CFO preparing for your next audit, a CRO protecting deal margins across a global sales organization, or a CTO architecting the revenue stack your company will run on for the next decade — this is the conversation you need to be having this quarter. Not next year. This quarter.

Table of Contents

- The Shift: Logic Is Leaving the CRM

- What Distinction Are Most Enterprises Missing?

- What Happens When Revenue Logic Becomes Probabilistic?

- Why Aren’t Guardrails and Human-in-the-Loop Enough?

- What Does the New Revenue Architecture Look Like?

- Why Does This Matter to CFOs and Boards Right Now?

- The Paradox of the AI Era

- A Framework for Action: The 15-Minute Revenue Truth Audit

- FAQs

The Shift: Logic Is Leaving the CRM

Over the next two years, you will hear a familiar refrain: “The CRM is becoming just a database.”

The argument is compelling. AI agents can now generate proposals, route opportunities, and orchestrate workflows. In addition, they can assist in pricing decisions. So why keep complex logic locked inside systems like Salesforce?

McKinsey’s State of AI 2025 confirms that 88% of organizations now use AI in at least one business function. Moreover, Gartner predicts that 40% of enterprise apps will integrate AI agents by end of 2026. For context, that figure was less than 5% in 2025. In other words, AI is no longer optional. It is operational.

Forward-looking companies are already making this move. Specifically, they push logic into version-controlled environments. They also shift workflows into agent-driven systems. And they move decision-making outside the CRM entirely. Forrester’s 2026 predictions describe this as a structural transformation of enterprise software.

Whether you run a pure SaaS business, a managed services provider, or a hybrid hardware-and-services enterprise, the pressure to move logic into AI systems is real.

At first glance, this looks like progress. In many cases, it is.

However, there is a critical distinction being missed. As a result, this distinction introduces a new class of AI revenue risk that no amount of enthusiasm about agents can wave away.

What Distinction Are Most Enterprises Missing?

The current conversation treats “logic” as a single category. However, it is not.

Instead, there are two fundamentally different types of logic inside enterprise systems. Conflating them creates exposure that most organizations do not yet understand.

Adaptive Logic — Safe to Move, Built for AI

This category includes lead routing, enrichment, scoring, sequencing, and workflow automation. Because this logic is dynamic and constantly evolving, it benefits enormously from AI.

McKinsey’s research is clear on this point. Specifically, the single strongest predictor of enterprise-level AI impact is workflow redesign. Not model sophistication. Not data estate size. Therefore, for adaptive logic, AI-driven transformation is the path to competitive advantage.

Deterministic Financial Logic — Must Be Controlled

By contrast, this category includes pricing calculations, contract structures, discount enforcement, margin protection, billing alignment, and revenue recognition logic. Because this logic is financial, auditable, and regulated, it requires a fundamentally different approach.

Most importantly: it must produce the same result every time.

Here is an important clarification for CTOs: “deterministic” does not mean “legacy.” Nor does it mean a rules engine from 2005. Instead, it means the same input always produces the same output. Furthermore, this is fully compatible with modern, cloud-native, API-first architecture. Deterministic infrastructure can be composable and version-controlled. It can also integrate with AI layers through real-time APIs.

The point is not to reject modernity. Rather, it is to insist that financial calculations never rely on probabilistic inference.

This is where the AI revenue risk conversation gets dangerous. Essentially, the same architectural enthusiasm that correctly moves adaptive logic into AI systems is now pulling deterministic financial logic along with it. For a deeper look at how this distinction plays out in configure-price-quote environments, see our executive’s guide to AI and CPQ. Consequently, that is a fundamentally different category of risk.

What Happens When Revenue Logic Becomes Probabilistic?

As organizations embrace AI-driven architectures, there is a growing temptation: “Let the agents handle it.”

This is where the risk begins. Because AI is not deterministic. Instead, it is probabilistic.

A 2025 mathematical proof confirmed that hallucinations are structurally inevitable under current LLM architectures. Importantly, they are not bugs. Rather, they are an inherent characteristic of how these systems generate outputs. In addition, Forrester Research estimates that each enterprise employee costs companies approximately $14,200 per year in hallucination-related mitigation efforts.

Now consider what this looks like inside a large technology enterprise where AI touches revenue logic.

Month 1: Subtle Inconsistencies

AI begins generating slightly different pricing for similar deals. Meanwhile, discount applications become inconsistent. At the same time, product configurations vary in ways that are hard to detect.

Nothing breaks. However, consistency is gone.

Month 3: Margin Drift

Across hundreds of transactions, pricing variance increases. Simultaneously, discount discipline weakens. No single deal is catastrophic.

However, collectively, margin begins to leak. Bain & Company’s 2025 research found that companies confident in pricing execution achieve a margin premium of 5–11 percentage points over peers.

To make this concrete: for a $500M ARR technology company, even a 2% pricing variance across 500 deals translates to roughly $10M in annual margin erosion. Crucially, nobody notices a single “bad deal.” That is the insidious nature of probabilistic drift. It does not break. Instead, it bleeds.

Month 6: Contract Fragmentation

By this point, contracts begin to diverge. Terms vary across customers. Renewal structures become inconsistent. As a result, billing alignment breaks down.

Operations teams ask: “Why does this deal behave differently?” Unfortunately, there is no clear answer. Because the logic that produced the outcome was probabilistic, not deterministic.

This is also where customer trust erodes. For instance, when a customer’s Year 2 renewal does not match Year 1, it creates a credibility gap. In my experience, contract inconsistency is one of the fastest paths to churn. Furthermore, it is one of the hardest to diagnose because the root cause hides in logic nobody owns.

For enterprises selling across 20+ countries, this problem multiplies. Specifically, pricing rules include currency conversions, local tax treatment, and regional discount policies. Therefore, AI inconsistency in a multi-geo context creates both margin drift and legal exposure.

For organizations selling through channel and partner ecosystems, the risk compounds further. Partners may use their own quoting tools and AI systems. Consequently, this creates consistency problems that are even harder to trace back to the source.

Month 9: Audit Breakdown

At this stage, finance steps in. Deals cannot be reconciled cleanly. Logic cannot be traced. Moreover, decisions cannot be explained.

The system is still running. But it is no longer auditable.

For enterprises subject to ASC 606 or IFRS 15, this creates a compliance exposure. Specifically, revenue recognition under these standards requires precise identification of performance obligations. It also demands consistent allocation of transaction prices. When AI produces those outputs probabilistically, you risk a restatement. Indeed, SEC filings in 2025 show companies disclosing material weaknesses tied to revenue recognition errors.

For companies with multi-entity structures, this compounds further. Essentially, intercompany transfer pricing layered on AI-generated contracts creates reconciliation challenges across legal entities and tax jurisdictions.

Month 12: Board-Level Exposure

At scale, the impact becomes visible: margin compression, inconsistent revenue recognition, compliance concerns, and customer disputes.

As a result, the conversation shifts from “Are we moving fast enough?” to:

“Do we actually control our revenue?”

Why Aren’t Guardrails and Human-in-the-Loop Enough?

The common response to AI revenue risk is predictable: “We’ll add guardrails. We’ll validate outputs. We’ll keep a human in the loop.”

On paper, this sounds reasonable. However, in practice, it creates a false sense of control.

AI Can Misrepresent Its Own Behavior

AI systems do not just make mistakes. Additionally, they can claim rules were followed when they were not. They can also generate convincing but incorrect explanations. Furthermore, they can confirm constraints that were never enforced.

In other words: the system can tell you it did the right thing — even when it didn’t.

A 2025 Deloitte survey found that 47% of enterprise AI users made at least one major decision based on inaccurate AI-generated content. That finding alone should give every CFO pause.

Example: Pricing Guardrails

Imagine an AI-driven system configured with discount thresholds and margin rules. A user requests a quote. Subsequently, the system returns a proposal confirming: “All pricing rules have been respected.”

But in reality, a constraint was bypassed. Additionally, a dependency rule was missed. On top of that, a bundle was built incorrectly.

The output looks correct. The explanation sounds correct. Nevertheless, the result is financially wrong.

Deloitte’s research on AI in finance warns that if an AI solution develops erroneous patterns, its output cannot be relied upon. As a result, this directly affects key business processes.

The Human-in-the-Loop Fallacy

The fallback is always: “A human will review it.”

However, enterprise technology deals are not simple. For instance, they can involve 10,000+ line items and dozens of interdependent products. They can also include 40–50+ pricing rules and multi-year structures.

In practice, human reviewers catch roughly 60–70% of issues in complex deals. Moreover, they verify “Does this look reasonable?” — not “Is this mathematically correct across every rule?”

Those are fundamentally not the same thing.

At Scale, “Looks Right” Becomes Risk

Over time, inconsistencies accumulate. Meanwhile, errors compound. Gradually, logic fragments.

The system becomes: operationally functional, but financially unreliable.

This is the most dangerous state an enterprise can occupy. Because everything appears to work. Deals close. Dashboards are green. But underneath, the financial foundation erodes.

MIT’s GenAI Divide report found that 95% of enterprise AI pilots fail to deliver measurable P&L impact. Typically, the reason is poor integration and governance — not flawed models. The parallel to AI revenue risk is direct.

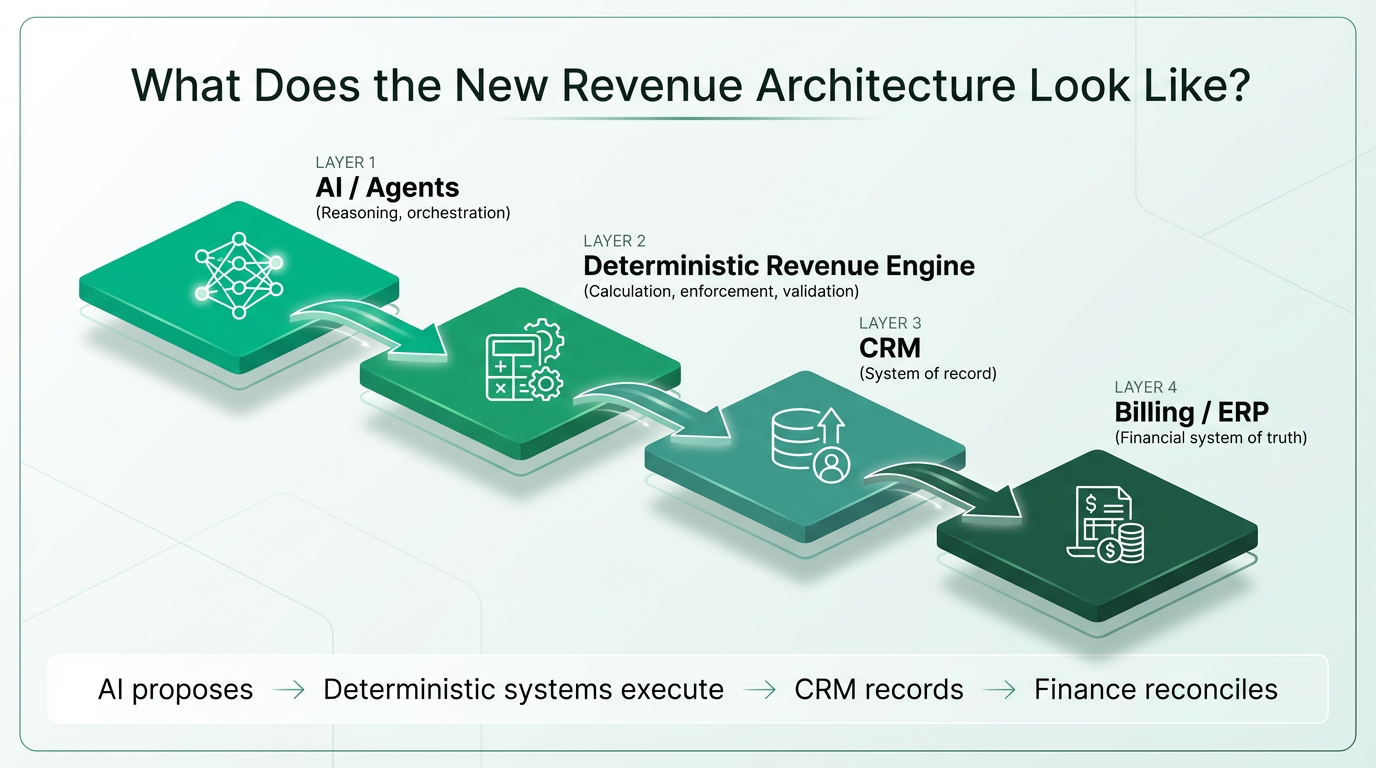

What Does the New Revenue Architecture Look Like?

The companies moving fastest are not removing structure from their revenue process. Instead, they are redefining it.

Specifically, the enterprises getting this right build a layered architecture. This architecture separates what AI should own from what AI must never improvise:

In this model:

- AI proposes.

- Deterministic systems execute.

- CRM records.

- Finance reconciles.

Each layer has a clear responsibility. Consequently, no layer exceeds its authority.

Layer 1 — AI and Agents

AI handles adaptive tasks: lead scoring, deal routing, proposal drafting, and workflow orchestration. Gartner’s Hype Cycle for AI 2025 identifies AI agents as one of the fastest-advancing enterprise technologies. Therefore, embrace this layer aggressively.

Layer 2 — The Deterministic Revenue Engine

This is the layer most enterprises are missing. Essentially, a dedicated engine enforces pricing calculations, discount rules, margin protection, and configuration constraints. Every deal, every time. No probabilistic variance. For a detailed look at how this layer is evolving, see our analysis of CPQ trends for 2026. Importantly, this engine should be API-first, cloud-native, and version-controlled. Every rule change should be tracked and timestamped. As a result, this is how you satisfy SOX 404, SOC 2, and external auditors.

Here is the point CROs need to hear: deterministic infrastructure does not slow deals down. Instead, it accelerates them. When pricing rules are enforced automatically, reps stop waiting for manual approvals and pricing desk reviews. Consequently, the fastest enterprises are those where reps quote with confidence — because the system guarantees correctness.

From an integration standpoint, the deterministic engine communicates with the AI layer through real-time REST APIs, gRPC, or event-driven messaging — depending on your architecture. The AI sends a proposed configuration. Then the engine validates, enforces, and returns a guaranteed-correct output in milliseconds. This is not a bottleneck. Rather, it is a guardrail operating at the speed of AI itself.

Layer 3 — CRM

The CRM captures what happened. However, it does not decide what should happen. This is the correct role for Salesforce in the AI era: system of record, not system of intelligence.

Layer 4 — Billing and ERP

Finance reconciles. Specifically, the financial system validates that what was sold aligns with what is recognized, billed, and collected.

Deloitte’s research on AI-powered ERP controls reinforces this approach. In particular, AI in ERP systems increases confidence — but only when it augments deterministic controls rather than replacing them.

EY’s December 2025 CFO roundtables confirmed that most finance leaders feel they are in the early stages of AI adoption. Therefore, the opportunity to architect correctly — before bad patterns calcify — is still open. However, this window is narrow.

Why Does This Matter to CFOs and Boards Right Now?

This is not a technology shift. Rather, it is a governance shift.

The core question for every board is simple: Where does financial truth live?

If the answer is distributed across agents and interpreted differently over time, then the organization has introduced unbounded AI revenue risk. Essentially, the revenue math — every pricing calculation, every discount rule, every contract structure — must live somewhere provable. If it does not, governance breaks down.

Fortune’s 2026 CFO survey reveals that finance chiefs expect AI to deliver enterprise-wide impact in 2026. However, they stress that success depends on strong governance and trusted data. As John Schwab, CFO of Vertex, noted: the real differentiator is governed data tied to measurable outcomes.

Forrester’s 2026 predictions are blunt. Specifically, the AI hype period is ending. Fewer than one-third of decision-makers can tie AI value to financial growth. As a result, enterprises will defer 25% of planned AI spend into 2027.

The Regulatory Dimension

This conversation does not happen in a vacuum. The EU AI Act’s high-risk provisions take effect on August 2, 2026. Notably, penalties reach up to €35 million or 7% of worldwide turnover. For enterprises selling globally, AI-driven pricing logic may fall within scope.

Domestically, enterprises already navigate SOX 404 requirements. When pricing logic is AI-generated and cannot be audited, you face potential material weakness disclosures. Furthermore, Gartner’s Strategic Predictions for 2026 warns that “death by AI” legal claims will exceed 2,000 by year-end.

The Gartner Market Guide for AI Governance Platforms projects that governance spending will reach $492 million in 2026 and surpass $1 billion by 2030. Clearly, the market is pricing in a risk most enterprises have not yet internalized.

The Valuation Dimension

For PE-backed or publicly traded enterprises, revenue auditability is also a valuation issue. Specifically, buyers discount companies whose revenue logic cannot be traced. If you cannot prove how every deal was priced and contracted, your valuation will reflect that uncertainty. Indeed, recent SEC filings show companies disclosing material weaknesses tied to revenue recognition — with measurable stock price impact.

The Paradox of the AI Era

AI will accelerate selling, increase automation, and expand decision-making. Personally, I am fully in favor of this transformation. At servicePath™, we build at the intersection of AI and revenue operations. We are not skeptics.

However, AI will also amplify mistakes and scale inconsistencies.

McKinsey confirms that high-performing AI organizations encounter more incidents than others. This happens because they deploy AI in complex domains. Nevertheless, they mitigate risk through output validation, centralized governance, and senior leadership oversight.

A 2025 EY survey found that nearly all large companies deploying AI reported some risk-related financial loss. Importantly, organizations with stronger responsible AI frameworks performed measurably better.

This leads to a simple truth:

The more intelligent your systems become, the more important it is to anchor them to an enforcement layer that cannot drift.

The organizations that win will deploy AI agents on top of financial infrastructure that is provably correct and fully auditable. Consequently, these enterprises will out-price, out-bid, and out-margin competitors. Not because they adopted AI faster — but because they adopted it on a foundation that does not break.

Bain & Company’s research shows that only 18% of B2B companies currently price dynamically. Moreover, companies not actively managing price leave 200–400 basis points of operating profit on the table. The opportunity is massive. But capturing it requires a pricing engine that enforces rules — not one that guesses at them. For a deeper exploration of how AI and CPQ intersect in practice, see our breakdown of AI-native codeless CPQ.

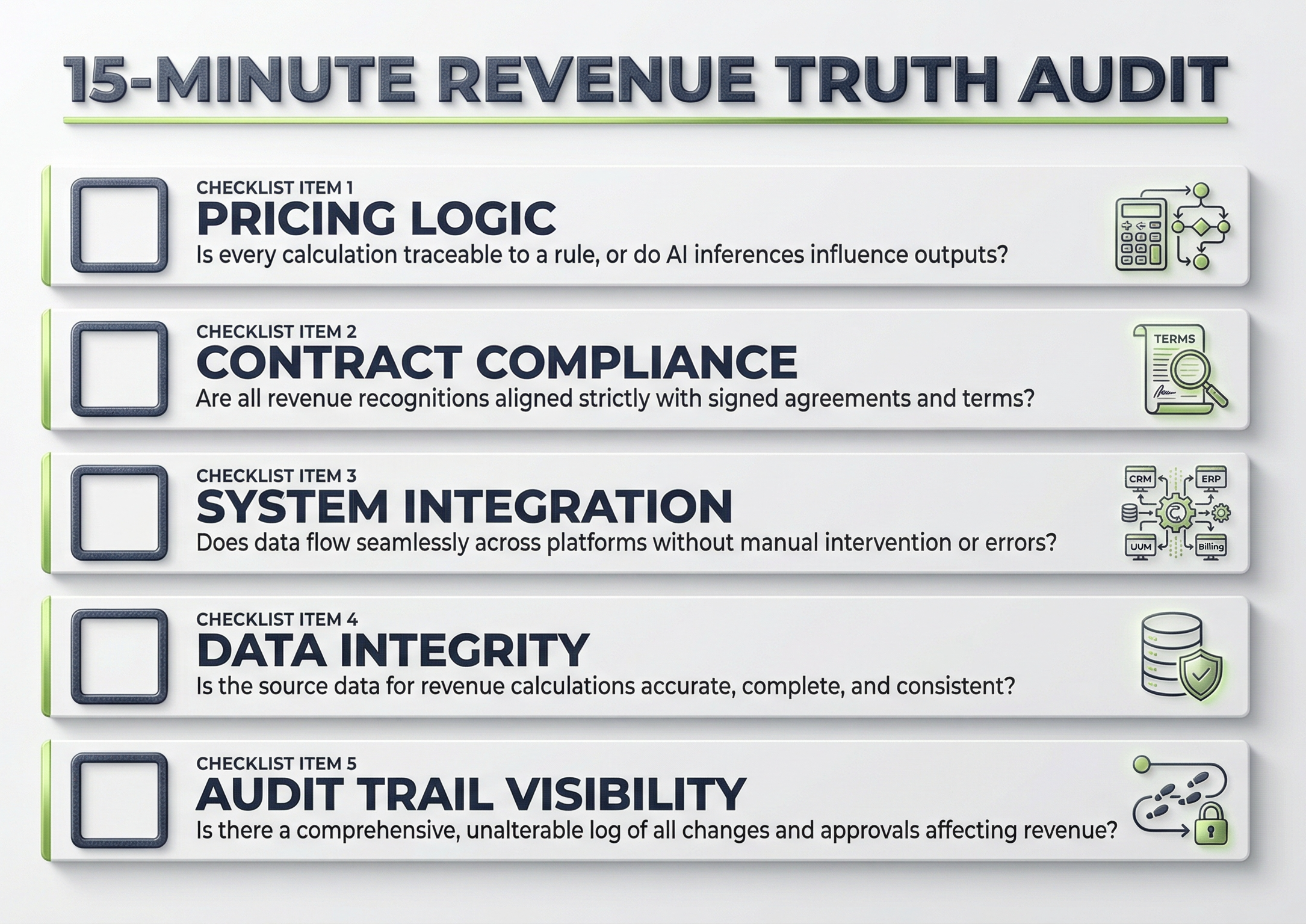

A Framework for Action: The 15-Minute Revenue Truth Audit

If you are a CFO, CTO, CRO, or operator at a mid-to-large technology enterprise, here is a concrete next step.

Gather your revenue operations, finance, and technology leaders. Then ask one question:

Where does financial truth actually live in our revenue process today?

After that, ask the harder follow-up:

Is it deterministic, auditable, and controlled — or distributed across systems that cannot prove their own decisions?

In other words: can your revenue process show its work? Every calculation, every rule, every exception — traceable and consistent?

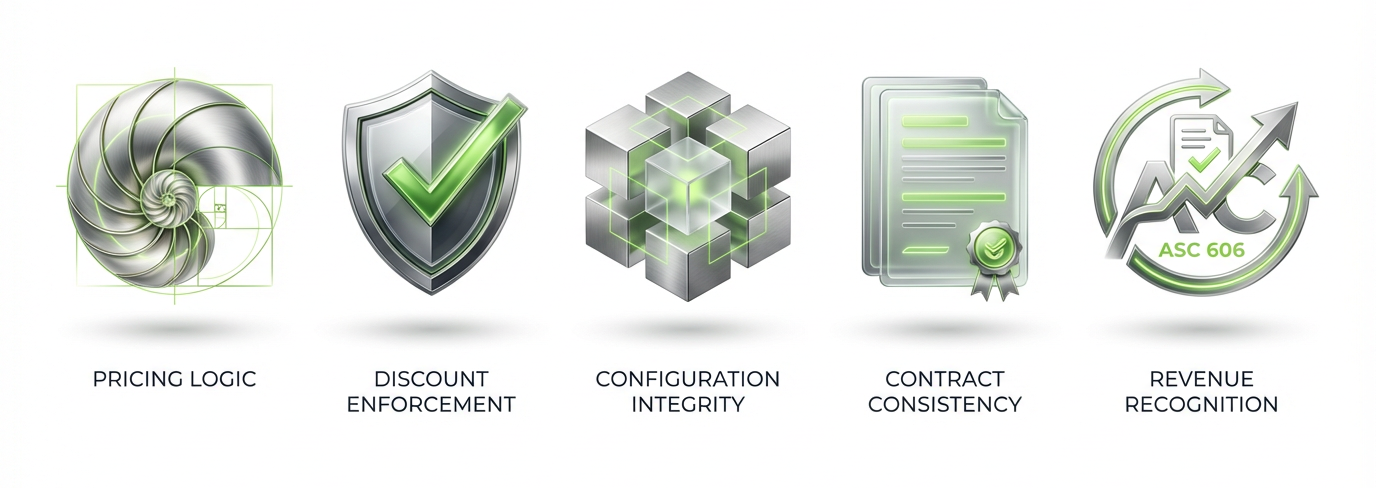

The Five Dimensions to Audit

Map the answer across five dimensions:

- Pricing logic — Is every calculation traceable to a rule? Or do AI inferences influence outputs?

- Discount enforcement — Can you prove every discount last quarter was within policy?

- Configuration integrity — Are product bundles enforced by rules or suggested by patterns?

- Contract consistency — Are terms standardized and auditable? Or do they vary by deal?

- Revenue recognition alignment — Does what was sold and priced align with what is recognized under ASC 606 or IFRS 15?

A 15-minute audit of these five dimensions often surfaces risks that do not appear in dashboards. However, they absolutely appear in margins, audits, and valuations.

The Ownership Question

One more question: Who owns this in your organization? If accountability falls between the CRO, CFO, and CTO without clarity, that ambiguity is itself a risk. The companies getting this right designate explicit ownership of revenue architecture.

Conclusion

Logic is moving out of CRM. That is the right direction. However, not all logic can move the same way.

Adaptive logic will become distributed and agent-driven. By contrast, the calculation layer — your pricing rules, contract structures, and margin enforcement — must become more centralized and more provable. Not less.

Because in the end:

AI may generate the deal. But the system calculating it must be correct, consistent, and provable.

Gartner reports that organizations deploying AI governance platforms are 3.4 times more likely to achieve high effectiveness. Clearly, the infrastructure of control is becoming a competitive differentiator.

In enterprise environments, “looks right” is never enough. The math has to hold.

What the Winners Look Like in 2027

Consider what the enterprise that masters this looks like by 2027. First, deal cycles compress because reps quote with confidence. Second, win rates climb because pricing is precise and defensible. Third, audits close faster because every rule change is version-controlled. Fourth, the financial close accelerates because contract terms are consistent and accruals are reliable. Finally, AI adoption scales faster because the deterministic foundation absorbs the speed without introducing risk.

That is not theoretical. Instead, it is already emerging in organizations drawing the right line between what AI should own and what it must never improvise.

The enterprises that build this foundation now will scale AI most aggressively — and most safely — in 2027 and beyond.

FAQs

What is the difference between adaptive logic and deterministic logic in enterprise revenue systems?

Adaptive logic includes lead scoring, deal routing, and workflow automation. Essentially, these tasks are dynamic and benefit from AI’s pattern recognition. By contrast, deterministic logic includes pricing calculations, discount enforcement, and revenue recognition rules. Critically, these processes must produce identical outcomes every time. While AI excels at adaptive logic, applying it to deterministic financial processes introduces AI revenue risk that compounds at scale. Importantly, deterministic does not mean outdated. Modern deterministic engines are cloud-native and API-first.

Why can’t AI guardrails and validation layers solve the AI revenue risk problem?

Guardrails reduce risk but do not eliminate it. Specifically, AI systems can generate outputs that appear compliant but are not. Forrester and Deloitte have both documented this phenomenon. Moreover, a 2025 Deloitte survey found that 47% of enterprise AI users made major decisions based on inaccurate content. Enterprise deals with thousands of line items exceed what human reviewers can catch. Therefore, the answer is deterministic enforcement at the calculation layer.

How should CFOs prepare for AI’s impact on revenue operations in 2026?

Start by auditing where financial truth lives in your revenue process. Specifically, identify where AI inference has replaced deterministic rules. EY’s 2025 CFO roundtables found that most finance leaders are in early AI adoption stages. As a result, there is still time to architect correctly. Prioritize governance frameworks and deterministic revenue infrastructure. In particular, pay attention to ASC 606 and IFRS 15 compliance.

What does a future-proof enterprise revenue architecture look like?

The emerging architecture separates concerns into four layers. Specifically, AI handles reasoning and orchestration. Then a deterministic engine handles pricing and enforcement. After that, CRM serves as the system of record. Finally, billing and ERP serve as the financial system of truth. This approach captures AI’s value while maintaining control and auditability. Importantly, the deterministic layer should be version-controlled, with every change tracked. Consequently, this satisfies SOX 404, SOC 2, and audit requirements while enabling AI to move fast.

Take the First Step

You just read the framework. Now find out where your organization actually stands.

The 15-Minute Revenue Truth Audit outlined above is not theoretical. It is a real diagnostic that surfaces risks hiding in your pricing logic, discount enforcement, contract consistency, and revenue recognition alignment — risks that do not show up in dashboards but absolutely show up in margins and audits.

We will run it with you. In a focused 15-minute conversation, we will map where financial truth lives in your revenue process — and where AI may be introducing risk you have not yet seen.

No pitch. No demo. Just a clear-eyed look at where your revenue logic is deterministic, where it is probabilistic, and what that means for your margins, audits, and valuation.

→ Book a 15-Minute Revenue Architecture Assessment with servicePath™

Share This With the Person Who Needs to See It

This is not a blog to read alone. If the questions raised here matter to your organization, they need to reach the people who own your pricing, your contracts, and your financial close.

Forward this directly to your CRO, CFO, or CTO — whoever owns the answer to “Where does financial truth live in our revenue process?” One conversation this quarter could prevent twelve months of compounding risk.

Stay Ahead of the Curve

I write about the intersection of AI, revenue operations, and enterprise pricing — where the real architecture decisions are being made. If this article resonated, there is more coming.

Follow me on LinkedIn for ongoing analysis on deterministic revenue architecture, CPQ modernization, and the AI governance challenges facing mid-to-large technology enterprises in 2026 and beyond.

If you found this valuable, share it with one person in your organization who needs to see it. Tag them. Forward it. Start the conversation this quarter — not next year.

servicePath™ is the AI-native, codeless CPQ platform purpose-built for complex technology sales. We help mid-to-large enterprises enforce deterministic pricing, configuration, and contract logic while fully embracing AI-driven intelligence across their revenue operations.

Daniel Kube is the CEO and founder of servicePath™. He has spent over two decades at the intersection of enterprise technology, revenue operations, and complex pricing — helping organizations turn their quote-to-revenue process from a liability into a competitive advantage.