Table of Contents

- Executive Summary

- Revenue Architecture 2.0: The Thesis

- The Stakes: Why 2026 Is a Defining Year

- Why Legacy CPQ Is Now a Strategic Liability

- The Solution: Human-Led, AI-Augmented Infrastructure

- servicePath™: Built for This Moment

- What Winning Looks Like: Stakeholder by Stakeholder

- Three Shifts That Make This Mandatory

- The Financial Impact Model

- Ready to Architect Your Revenue for 2026?

- About servicePath™

- FAQ

Executive Summary

The enterprise revenue stack is broken — and most leaders know it.

Legacy CPQ tools that once felt revolutionary are now ceilings, not accelerators. They buckle under complex pricing, multi-CRM sprawl, and the governance demands that AI introduces. Meanwhile, Salesforce has officially stopped selling its CPQ managed package. As a result, thousands of organizations are staring at a frozen product with no roadmap.

However, the solution is not handing the keys to autonomous AI agents. Instead, it is building Revenue Architecture 2.0 — a human-led, AI-augmented control plane that ensures precision, protects margins, and empowers teams without replacing them.

Boards are scrutinizing AI risks. RevOps teams are fighting latency. CFOs want governance they can audit. In short, the winners will be those who architect revenue as infrastructure: deterministic at its core, informed by AI, and always under human authority.

Revenue Architecture 2.0: The Thesis

Modern enterprises do not fail on features — they fail on architecture.

Revenue Architecture 2.0 positions CPQ not as a point tool, but as the authoritative control plane for the entire revenue lifecycle. Specifically, it is engineered for AI governance, complex quoting in tech sales, MSPs, and telecom, and seamless interoperability across CRM, ERP, and PLM stacks. Most importantly, it is human-led: AI augments judgment, but humans own decisions, with hard-coded logic enforcing compliance and accuracy.

This addresses the core tension: enterprises crave AI’s speed but fear its risks. Revenue is too relational, too political, and too accountable to delegate to probabilistic systems. Therefore, we need infrastructure that strengthens human teams — boosting confidence, reducing errors, and unlocking new monetization models without workforce disruption.

The Stakes: Why 2026 Is a Defining Year

The M&A wave and CRM fragmentation

The data tells a stark story. Global M&A reached $4.9 trillion in 2025, a 40% surge and the second-highest deal value on record, according to Bain & Company’s 2026 M&A Report. In addition, eighty percent of the 300 M&A executives Bain surveyed expect to sustain or increase deal activity this year. On top of that, private equity is sitting on $3.8 trillion in unrealized value, and firms are under intense pressure to demonstrate value creation — not just financial engineering.

The cloud CPQ market is projected to reach nearly $5.8 billion in 2026, growing at a 16% CAGR according to MGI Research. Furthermore, the 2026 Gartner Magic Quadrant for CPQ Applications evaluated 16 vendors, reflecting a market expanding and fragmenting at the same time. Clearly, this is revenue infrastructure now.

The Salesforce CPQ wake-up call

Add AI to the equation and the risks compound. For example, hallucinated discounts, non-compliant bundles, and unauditable decisions are not theoretical scenarios. They are boardroom nightmares waiting to happen. Meanwhile, Salesforce confirmed End-of-Sale for its CPQ managed package in March 2025. No new customers. No meaningful feature investment in over four years. As a result, the fragility of legacy approaches — siloed, rigid, unprepared for AI-driven workflows — is now fully exposed.

Four converging dynamics

In 2026, four revenue dynamics are converging:

Monetization complexity. MSPs and tech providers juggle recurring models, bundles, and usage-based pricing across hybrid stacks. In other words, the quoting engine that handled simple per-seat licensing five years ago cannot handle outcome-based monetization today.

AI backlash. Buyers and sellers alike resist AI systems that “replace” human judgment. The fear is real — accountability gaps, internal politics, and the erosion of relational selling. For instance, McKinsey’s State of AI in 2025 found that 88% of organizations now use AI in at least one function, yet only 6% qualify as “high performers” capturing meaningful EBIT impact. The gap is not technology access — it is organizational discipline and workflow redesign.

Stack obsolescence. Multi-cloud environments demand interoperability, not more middleware. Consequently, every acquisition adds another CRM instance, another pricing spreadsheet, another set of diverging commercial logic.

Governance imperative. Boards demand audit trails, margin guardrails, and human oversight. Notably, Gartner predicts that over 40% of agentic AI projects will be canceled by the end of 2027 due to escalating costs, unclear business value, or inadequate risk controls. In short, governance is not optional — it is existential.

Without a unified architecture, organizations face what I call “revenue latency”: slow cycles, shadow spreadsheets, and untapped potential. However, the opportunity is clear. Architect revenue as infrastructure — hidden plumbing that powers deals, with a human-friendly interface on top.

Why Legacy CPQ Is Now a Strategic Liability

Let me be direct about what is happening.

Legacy CPQ — whether Salesforce, Expertlogix, or homegrown — treats revenue as a silo. As a result, rigid rules engines cannot handle AI insights without custom hacks, leading to errors in complex scenarios like MSP bundling or telecom provisioning. Worse still, in the AI era, they invite ungoverned risks: autonomous agents negotiating prices without guardrails? That is a boardroom nightmare.

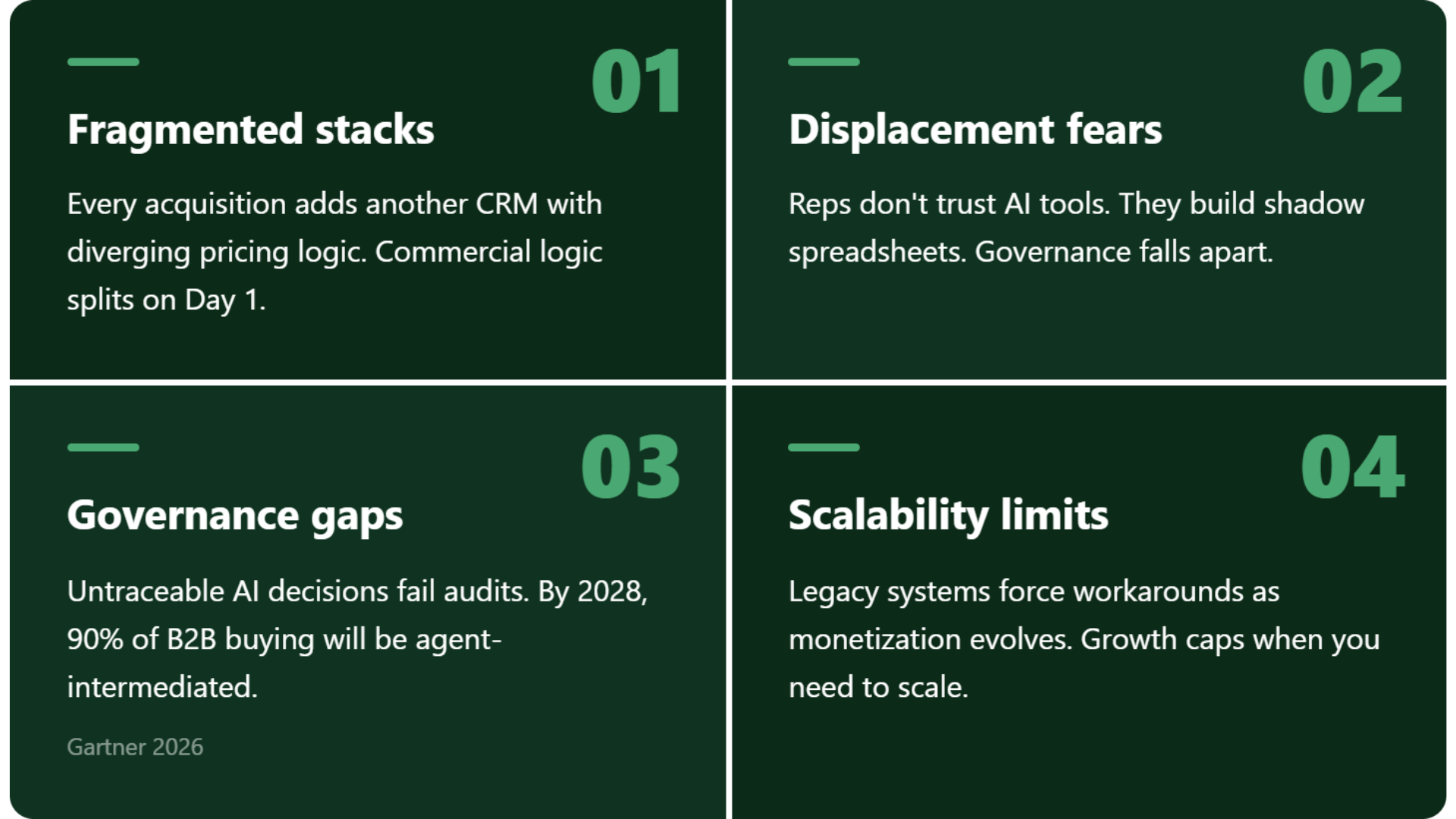

Four traps of the status quo

The status quo traps enterprises in four ways:

Fragmented stacks. Manual syncs between Salesforce, NetSuite, and Dynamics waste time and leak revenue. Moreover, every M&A deal makes this worse. Every acquisition introduces another CRM instance with its own pricing logic, product catalog, and approval workflows. The commercial logic diverges on Day 1, and it keeps diverging.

Human displacement fears. Overhyped “AI-first” tools promise autonomy but erode seller confidence and threaten seat-based models. As a result, when reps do not trust the tool, they build shadow spreadsheets — and your governance falls apart.

Governance gaps. Without deterministic floors, AI creates exposure — untraceable decisions that fail audits. For context, Gartner’s Strategic Predictions for 2026 warn that by 2028, 90% of B2B buying will be AI-agent intermediated, pushing over $15 trillion in spend through AI agent exchanges. If your systems cannot produce an audit trail for every pricing decision, you are exposed.

Scalability limits. As monetization evolves — outcome-based models, usage tiers, hybrid bundles — legacy systems force workarounds. Consequently, they cap growth precisely when you need to scale.

Ignore this, and revenue becomes a liability: slower closes, eroded margins, and competitive disadvantage in a market where AI-savvy rivals move faster.

The Solution: Human-Led, AI-Augmented Infrastructure

Revenue Architecture 2.0 flips the script. It is a composable control plane that orchestrates revenue across systems — deterministic logic ensures accuracy, AI provides guidance, and humans retain authority. Importantly, there is no rip-and-replace: it layers on existing stacks, reducing migration latency by 50% while preserving your investments.

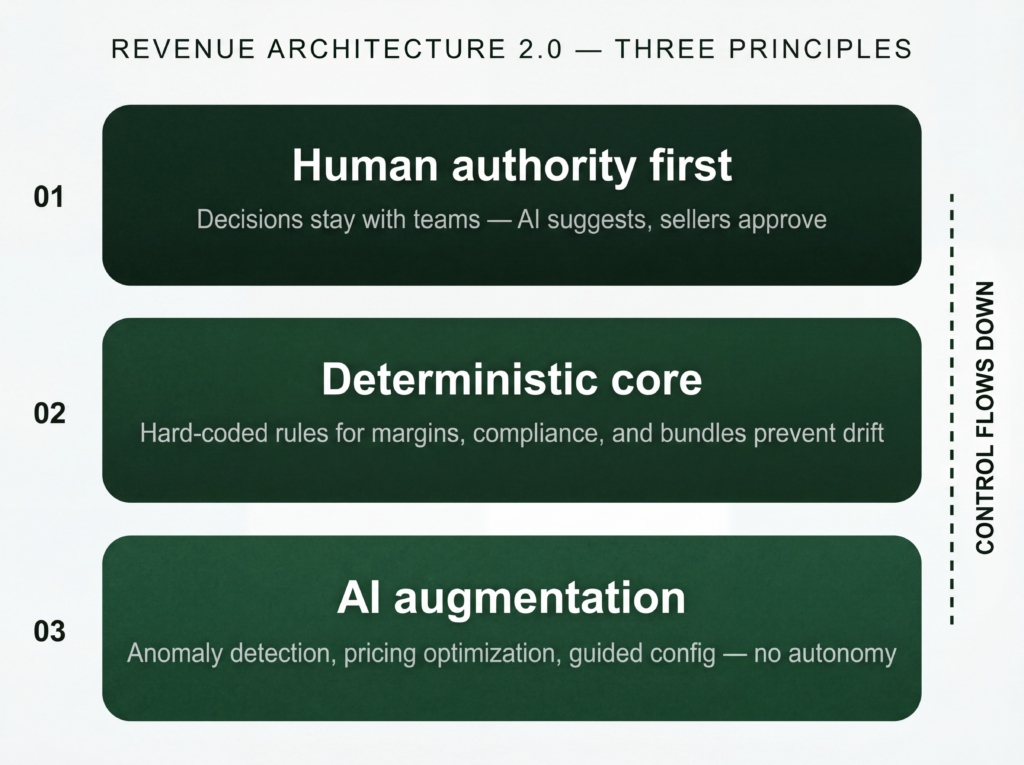

Three core principles

1. Human authority first. Decisions stay with teams. AI suggests; sellers approve. Revenue is too relational and too accountable to hand over to probabilistic systems. Therefore, the winners are the organizations that use AI to make their people faster and more confident — not the ones that try to remove people from the loop.

2. Deterministic core. Hard-coded rules for margins, compliance, and bundle logic prevent drift. AI can recommend a pricing adjustment, but the guardrails ensure it never crosses a legal or business boundary — regardless of what it “learns.” This is the difference between enterprise-safe AI and the kind that generates Gartner’s predicted wave of project cancellations.

3. AI augmentation. Intelligent insights for anomaly detection, pricing optimization, and guided configuration — without autonomy. In other words, this is not “AI-native” in the hype sense. It is enterprise-safe: guardrails for AI in revenue, aligned with board priorities.

Why McKinsey’s research validates this approach

McKinsey’s 2025 State of AI research found that among 25 attributes tested, the redesign of workflows had the single biggest effect on an organization’s ability to see EBIT impact from AI. The companies capturing real value are not bolting AI onto existing processes — instead, they are rebuilding how work gets done. Revenue Architecture 2.0 is that rebuild for the commercial engine.

Specifically, the high performers — the 6% generating more than 5% of EBIT from AI — share a common trait: they redesign workflows, structures, and governance around AI rather than layering it onto legacy processes. That is precisely what a CPQ control plane enables.

servicePath™: Built for This Moment

At servicePath™, we have architected our CPQ as this control plane — recognized as the sole Visionary in Gartner’s Magic Quadrant for CPQ Applications for three consecutive years (2024–2026), and an IDC Major Player. Our platform handles complex tech sales for MSPs and telecom providers, integrating seamlessly with Salesforce, NetSuite, Dynamics, and more via our Revenue Interoperability Hub.

Real results from our deployments

50% Faster Quoting. AI-guided workflows cut cycle times without replacing reps. As a result, sellers close with precision, not guesswork.

Zero-Tolerance Governance. Audit-ready trails and margin protection — trusted by enterprises that cannot afford AI pitfalls. Specifically, every pricing decision is traceable, and every discount is governed.

Seat-Strengthening Economics. We boost team productivity, not eliminate roles — thereby preserving your revenue model. This matters deeply in an environment where Forrester predicts that 20% of B2B sellers will be forced to engage in agent-led quote negotiations in 2026. Your sellers need better tools, not replacement.

In a world of AI chaos, servicePath™ delivers calm, responsible revenue infrastructure.

What Winning Looks Like: Stakeholder by Stakeholder

Revenue Architecture 2.0 is not abstract. Here is what it delivers for each stakeholder at the table — contrasted against the status quo pains of legacy systems, with real-world examples from our MSP and telecom deployments.

For the CFO: Margin protection and audit-ready governance

Status quo: Constant revenue leakage from pricing errors and unauditable AI experiments, leading to 5-10% margin erosion and audit headaches.

Value with servicePath™: Unbreakable auditability and margin guardrails deliver 2-5% margin uplift within the first two quarters through deterministic controls, plus full traceability for compliance.

Example: A mid-market telecom provider (~$150M revenue) reduced quarterly audit prep from weeks to days. As a result, they recaptured $500K in leaked discounts by enforcing AI-informed but human-approved pricing rules — turning revenue risks into predictable profits.

For RevOps: Killing revenue latency

Status quo: Siloed stacks and manual workflows cause “revenue latency,” with teams spending 30-40% of time on data syncs and error fixes, stalling operational efficiency.

Value with servicePath™: End-to-end orchestration slashes this overhead by 50%, freeing capacity for strategic analysis while eliminating shadow systems.

Example: For instance, an MSP consolidated quoting across Salesforce and NetSuite, cutting bundle configuration time from hours to minutes — boosting operational throughput by 35% and enabling real-time anomaly detection to flag 20% more upsell opportunities.

For the CRO: Seller confidence and faster closes

Status quo: Slow cycles and inconsistent quoting undermine seller confidence, resulting in 15-25% longer deal times and missed win rates due to rigid tools that cannot adapt to complex monetization.

Value with servicePath™: AI-guided workflows accelerate closes by 40-50%, empowering sellers with precise recommendations while preserving relational control.

Example: A tech services firm saw win rates climb 18% after implementation, as reps used AI insights to optimize bundles on the fly — closing a $2M recurring deal in half the usual time without discounting margins. To illustrate what that looks like in practice: a rep in Dynamics quotes a managed network service. The AI co-pilot then recognizes that the customer’s infrastructure profile matches a security monitoring package that came into the catalog through a recent acquisition. It surfaces the cross-sell prompt with margin guidance. The rep adds it in two clicks. As a result, the deal expands 20%+ and both products are governed under a single contract with unified discount controls.

For the CIO/CTO: Composable architecture and multi-CRM reality

Status quo: Integration middleware bloat and legacy rigidity force costly custom development (often $100K+ per year), with no path to AI readiness or multi-cloud flexibility.

Value with servicePath™: Composable architecture cuts integration costs by 60-70%, providing future-proof hubs that scale without vendor lock-in.

Example: A hybrid MSP migrated from Salesforce CPQ in under 90 days, saving $150K in middleware while gaining seamless PLM and ERP connectivity — enabling AI-augmented forecasting that improved resource allocation accuracy by 25%. In addition, our Revenue Interoperability Hub provides API-first connectors for Salesforce, Dynamics, HubSpot, NetSuite, and ServiceNow with pre-built data mappings, so your integration team is not building from scratch.

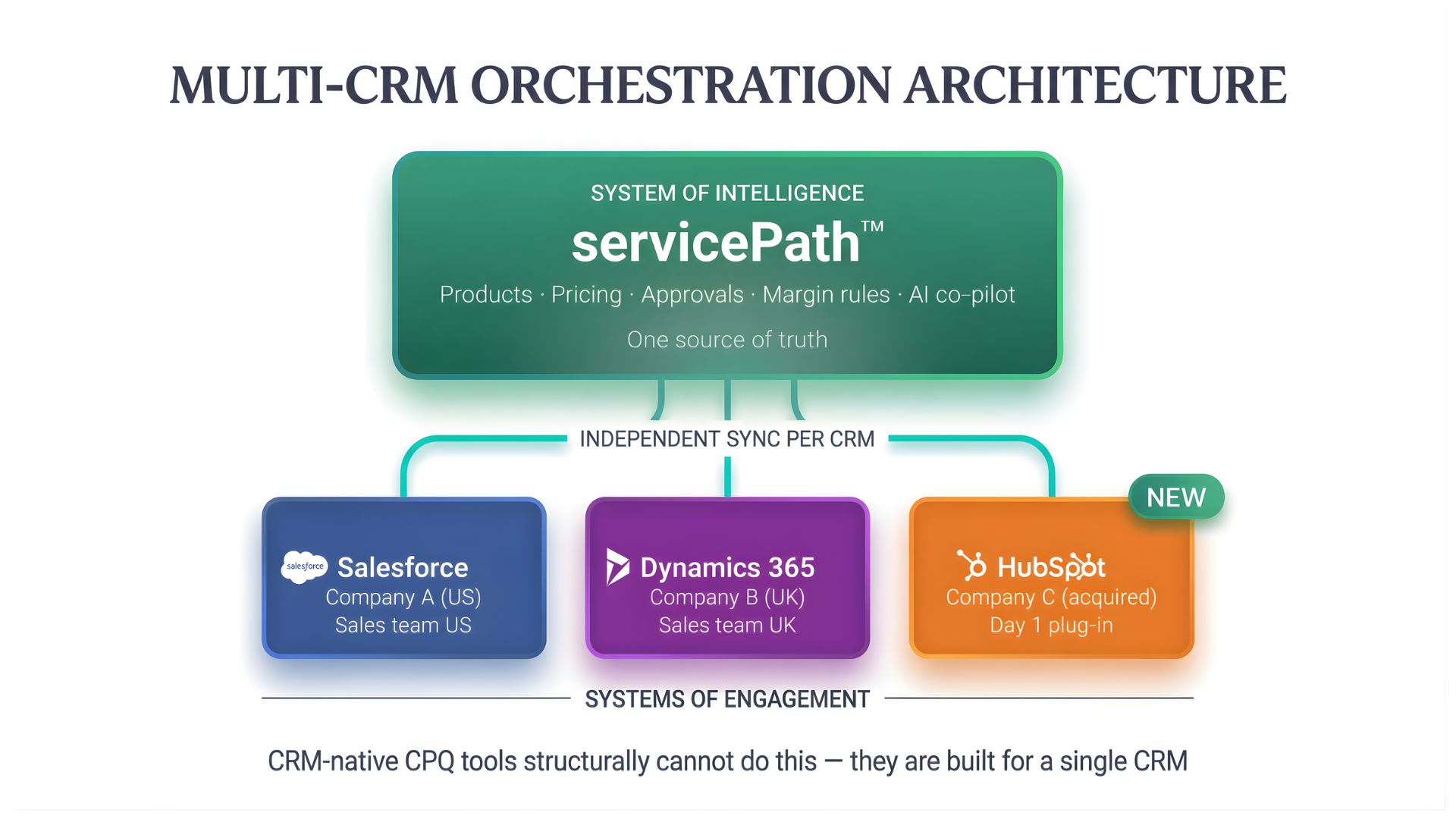

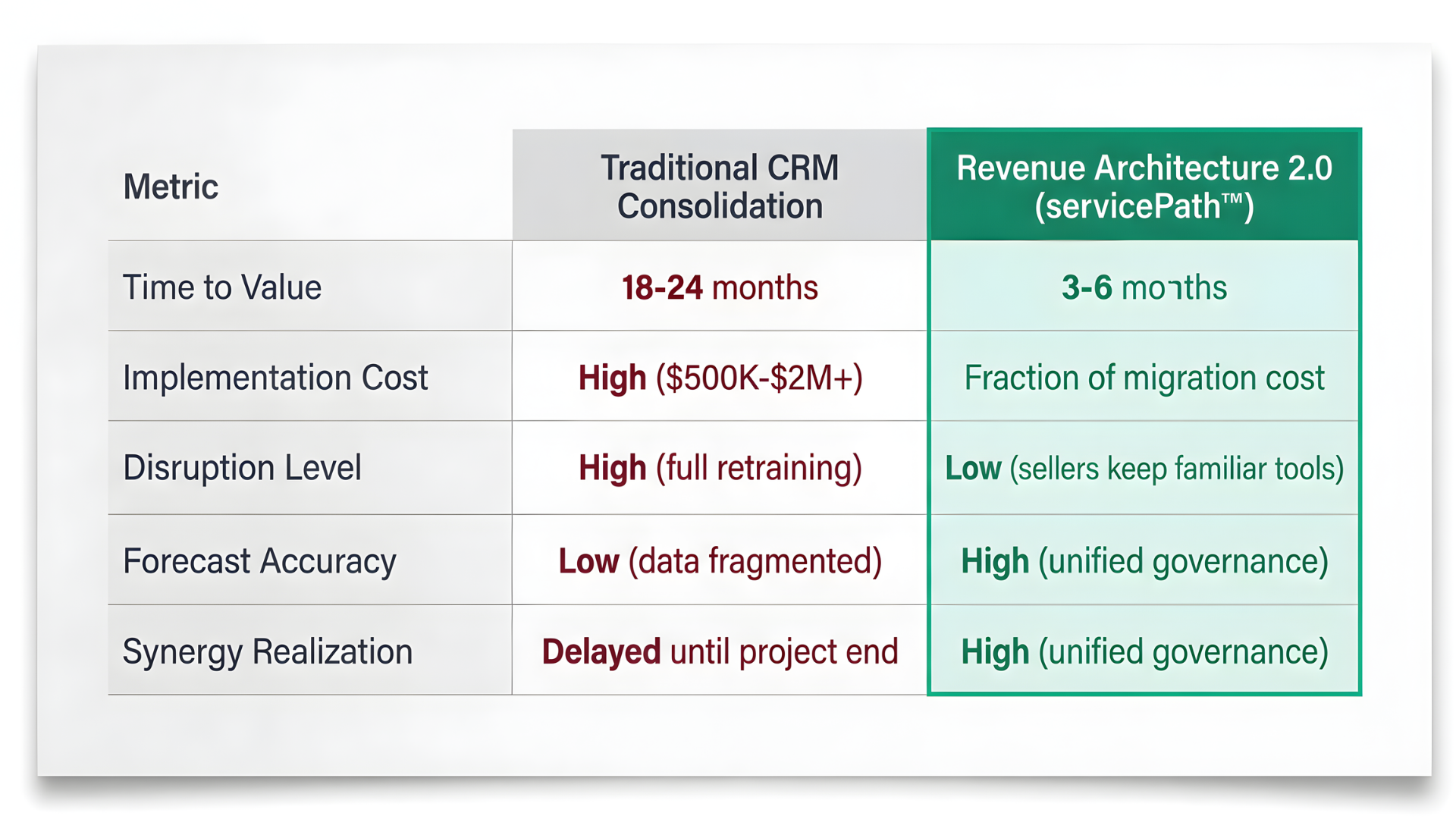

For the CTO specifically, this is also where our Multi-CRM Adapter and Service Contracts capability come in. Most enterprises run multiple CRM instances post-acquisition — Salesforce, Dynamics, HubSpot — each carrying its own pricing logic. The traditional playbook says consolidate first. However, that is a value trap: CRM migrations cost millions, take 18+ months, and stall the revenue synergies that M&A was supposed to deliver.

Our Multi-CRM Adapter lets each CRM sync independently to the servicePath™ brain. As a result, sellers stay in their familiar system. The CPQ enforces unified pricing, margin rules, and cross-sell prompts across every instance.

In other words, one source of truth, multiple points of engagement. New acquisitions plug in on Day 1 rather than waiting years for a consolidation that may never happen. This is a capability that CRM-native CPQ tools and point solutions structurally cannot deliver — they are architected for a single CRM instance, not for orchestrating commercial logic across a heterogeneous stack.

Meanwhile, servicePath™ Service Contracts solves the contract lifecycle problem that plagues every MSP and telecom provider: siloed contract data across CRM, CMDB, and billing systems leading to missed renewals, incorrect invoicing, and revenue leakage.

Specifically, it is a centralized, cloud-based platform for tracking, modifying, and renewing service agreements — with mid-term revisions, co-termination, auto-renewals with end-of-life controls, dynamic financial dashboards, multi-currency support, and seamless integration with Salesforce, Dynamics, HubSpot, ServiceNow, and DocuSign.

For the CTO, this means contract data feeds directly into the CPQ brain, enabling accurate quoting, better forecasting, and governance that auditors actually trust.

For partners: Consistent, governed channel quoting

Status quo: Fragmented enablement tools lead to inconsistent partner quoting, causing channel conflicts and 10-20% lost ecosystem revenue from poor onboarding and customization barriers.

Value with servicePath™: Low-code governance tools streamline partner access, increasing channel productivity by 30-40% through shared, compliant workflows.

Example: A telecom aggregator empowered 50+ partners with branded quoting portals, growing joint revenue 22% by simplifying bundle configurations and ensuring margin alignment — turning partners into seamless extensions of the sales engine. As Michael Cantor, CIO of Park Place Technologies, put it when describing why they chose servicePath™ to support their global growth strategy: the platform has enterprise features and scalability built in, which is critical when the only constant is change.

The 2026 Strategic Landscape: Three Shifts That Make This Mandatory

Shift 1: Agentic AI demands unified logic

Gartner predicts that 40% of enterprise applications will include task-specific AI agents by the end of 2026, up from less than 5% in 2025. In addition, at least 15% of day-to-day work decisions will be made autonomously by agentic AI by 2028. However, AI agents cannot function in chaos. If your pricing logic is scattered across five spreadsheets and three CRM instances, your AI strategy is dead on arrival. Therefore, by centralizing commercial logic in a governed CPQ brain, you create the structured data layer that agentic AI needs. In essence, you are building the highway for your future AI workforce.

Shift 2: The rise of agent-to-agent commerce

This is not theoretical. Forrester predicts that 20% of B2B sellers will be forced to engage in agent-led quote negotiations in 2026, as buyer organizations deploy AI engines to support purchasing. Meanwhile, Gartner’s 2026 Strategic Predictions indicate that by 2028, 90% of B2B buying will be AI-agent intermediated, pushing over $15 trillion of spend through AI agent exchanges.

What does this mean in practice? Your customers will soon have AI negotiating on their behalf — pinging your systems for pricing, specs, and discounts instantly. If your quoting engine is slow or manual, you lose the deal before a human even sees it. Consequently, a unified CPQ brain exposes API endpoints to buyer agents, enabling automated, profitable negotiation at machine speed.

Shift 3: Full potential due diligence is the new standard

Bain’s 2026 Global PE Report reinforces the architecture argument from the investment side. Specifically, the firms generating strong returns are those executing full potential due diligence that scrutinizes revenue levers, operational levers, and technology levers. As a result, technology architecture is now a value-creation variable, not a back-office concern. For PE sponsors, a centralized CPQ brain that new acquisitions plug into on Day 1 — enabling cross-sell in months rather than years — is not a nice-to-have. It is a portfolio-level lever that strengthens the exit narrative.

Looking ahead: What 2028 demands

If these shifts accelerate on their current trajectory, by 2028 the enterprises that thrive will be the ones whose revenue infrastructure can negotiate autonomously with buyer agents, adapt pricing models in real time, and maintain full governance across every transaction — all without a human touching the keyboard for routine deals. In other words, the CPQ brain you build today is not just solving a 2026 problem. It is the foundation for a commercial operating system that compounds in value with every acquisition, every new product line, and every AI capability you layer on top.

The Financial Impact Model

The Cost of Inaction: For a $100M revenue company, a 1% margin leak due to siloed pricing logic equals $1M in pure EBITDA lost annually. At a 15x valuation multiple, that is $15M in enterprise value destroyed by poor data governance. Multiply that across a PE portfolio and the numbers become staggering.

The Future Is Not CRM-First. It Is Revenue-First. And It Is Human-Led.

Most enterprises will remain multi-CRM for the foreseeable future. Therefore, the decision for leaders and sponsors is clear: you can let CRM migration roadmaps dictate your revenue strategy, or you can adopt an architecture where CRMs are allowed to differ, but your commercial engine operates as one.

Revenue Architecture 2.0 turns technological fragmentation from a liability into a managed, strategic advantage. Ultimately, it is the architecture for leaders who need to show revenue impact now — not after a multi-year IT program.

These are the conversations I am having with CTOs, CROs, and PE sponsors every week. If any of this resonates, here is how to take the next step.

Ready to Architect Your Revenue for 2026?

If any of this resonated, I would welcome the conversation. Here are three ways to continue it.

Talk to me directly If you are a CEO, CTO, or PE sponsor wrestling with CRM fragmentation or CPQ strategy, reach out. I will make time for a candid conversation about your architecture — no pitch deck required. → Email me directly

See servicePath™ in action In 15 minutes, our team will show you how servicePath™ CPQ+ sits above Salesforce, Dynamics, and HubSpot to standardize what matters most — without ripping out what already works. → Request a demo

Read how others have done it Explore how enterprise teams — including Dell, Park Place Technologies, and Telent — modernized quoting and contract management without ripping out CRM. → View case studies

About servicePath™

servicePath™ is the sole Visionary in Gartner’s 2026 Magic Quadrant for Configure, Price and Quote Applications — the fourth consecutive year in the Visionary quadrant and the third year standing alone among 16 evaluated vendors. In addition, we are recognized as an IDC Major Player.

Our platform handles complex technology sales for MSPs, telecom providers, and enterprise technology companies, integrating seamlessly with Salesforce, Microsoft Dynamics, HubSpot, ServiceNow, and NetSuite. We serve customers including Dell, Telefónica, TierPoint, Park Place Technologies, and Telent.

servicePath™ is headquartered in Burlington, Ontario, Canada, with offices in London, UK and Dubai, UAE.

Learn more at servicepath.co

FAQ

What is Revenue Architecture 2.0? A design philosophy that positions CPQ as the authoritative control plane for the entire revenue lifecycle — separating where sellers work (their CRM) from how the enterprise sells (unified commercial logic), with a deterministic core, AI augmentation, and human authority over all decisions.

What happened to Salesforce CPQ? Salesforce confirmed End-of-Sale in March 2025. Existing customers retain support, but no new features are planned, the partner ecosystem is shrinking, and strategic investment has shifted to Revenue Cloud Advanced — which requires a full rebuild, not a migration.

How does Multi-CRM orchestration work? Each CRM syncs independently to the servicePath™ CPQ brain. As a result, sellers stay in their familiar system. The CPQ enforces unified pricing and cross-sell prompts across every instance. New acquisitions plug in on Day 1.

What is the best Salesforce CPQ alternative in 2026? With Salesforce CPQ now End-of-Sale and Revenue Cloud Advanced still maturing, organizations need a CPQ that works across CRMs — not just within Salesforce. servicePath™ is a vendor-agnostic, AI-augmented control plane that integrates with Salesforce, Dynamics, HubSpot, and NetSuite. In addition, it is recognized as the sole Visionary in Gartner’s 2026 Magic Quadrant for CPQ Applications.

Ready to discuss? Reach out at daniel@servicepath.co or connect on X @danielkube