Executive Summary

This article explains how to audit AI pricing decisions. It covers why boards will demand this capability by 2026, what auditable governance means, and how to build it into your revenue architecture.

Bottom line: Companies that can prove how AI made pricing decisions will capture disproportionate value. In contrast, those that can’t face margin erosion, valuation challenges, and regulatory scrutiny.

By 2026, boards will demand proof that AI pricing decisions are auditable.

However, while 88% of firms have deployed AI in at least one business function (McKinsey State of AI, 2025), most cannot reconstruct a single pricing decision with complete audit trails.

For example, Goldman Sachs forecasts AI agents will capture more than 60% of the software profit pool by 2030 (Goldman Sachs Research, 2025).

Furthermore, the combined market for customer-service SaaS and AI agents could expand by 20–45% versus a no-AI scenario. As a result, the overall application-software market could reach $780 billion by 2030 at a 13% CAGR.

Here’s where it gets expensive.

Bain & Company warns that firms pursuing “business as usual” strategies—without embedding AI governance—could see margin declines of more than 200 basis points and revenue erosion of 30% or more over five years (Bain & Company, 2025).

Companies that build auditable AI governance now will capture disproportionate value; those that retrofit later face significantly higher costs and longer timelines.

5-Minute Governance Health Check

Score Your AI Pricing Governance (Answer YES or NO)

Can you reconstruct any pricing decision from the past 12 months—data sources, policy applied, approvals, alternatives considered?

Your Score:

- 6–8 YES: You’re ahead of most of the market. Keep investing.

- 3–5 YES: Moderate risk. Start planning governance upgrades.

- 0–2 YES: High risk. Immediate action required.

Why Boards Are Asking: “Can We Audit AI Pricing Decisions?”

The question isn’t hypothetical. In fact, it’s already happening in board meetings, PE diligence calls, and SOX audits.

Here’s a real scenario playing out right now:

Picture this: Your CRO proudly reports that AI-driven Configure-Price-Quote (CPQ) has accelerated deal velocity by 40%.

The board applauds.

Then, the chair leans forward:

“If our AI mispriced that $10 million deal tomorrow, can you show me exactly how it made the decision?”

Silence.

First, the CRO points to workflow approvals. Next, the CFO mentions “controls.”

However, no one can reconstruct the data inputs, policy logic, alternatives evaluated, or confidence thresholds that led to the final price.

That’s the governance gap. Consequently, it’s about to become the defining risk for revenue platforms in 2026.

Why This Matters Now

According to Gartner, by 2028, 90% of B2B buying decisions will be mediated by AI agents. In addition, these agents will move more than $15 trillion in purchasing activity globally.

Goldman Sachs Research forecasts AI agents will account for more than 60% of the software market by 2030. As a result, the profit pool is fundamentally shifting toward agent-centric offerings.

Furthermore, the combined market for customer-service SaaS and AI agents alone could grow 20–45% by 2030 versus a no-AI scenario.

Here’s the competitive reality:

Companies that can answer the board’s question will capture disproportionate value in this agent-driven economy.

In contrast, those that can’t will face margin erosion, valuation challenges, and regulatory scrutiny.

More importantly, the ability to audit AI pricing decisions is no longer optional.

Instead, it’s becoming a standard due-diligence requirement for PE firms, a regulatory expectation for financial services, and a board-level governance mandate across industries.

What Auditors & Boards Will Ask in 2026

Questions for the CFO:

- First, can you provide a full audit trail for our top 20 deals closed last quarter?

- Second, how do you enforce revenue recognition policies (ASC 606, IFRS 15) at the point of quote generation?

- Third, can you detect pricing created outside the CPQ system (shadow quoting in Excel, email, or Slack)?

- Finally, what’s our aggregate margin exposure across all active quotes right now?

Questions for the CRO:

- What’s the average margin variance across similar deals?

- Additionally, how many discount exceptions were granted last quarter?

- Can you prove your AI isn’t systematically varying prices in ways that could raise regulatory concerns?

- Moreover, how long does it take to reconstruct a pricing decision when a customer disputes a quote?

Questions for the Board:

- What’s our exposure if AI pricing decisions are found to be non-compliant during an audit?

- In addition, how long would it take to investigate a pricing dispute?

- Finally, are we audit-ready if regulators or customers demand pricing documentation?

Consequently, if you can’t answer these questions with data and documentation, you have a governance gap.

The Real Cost of Ungoverned AI

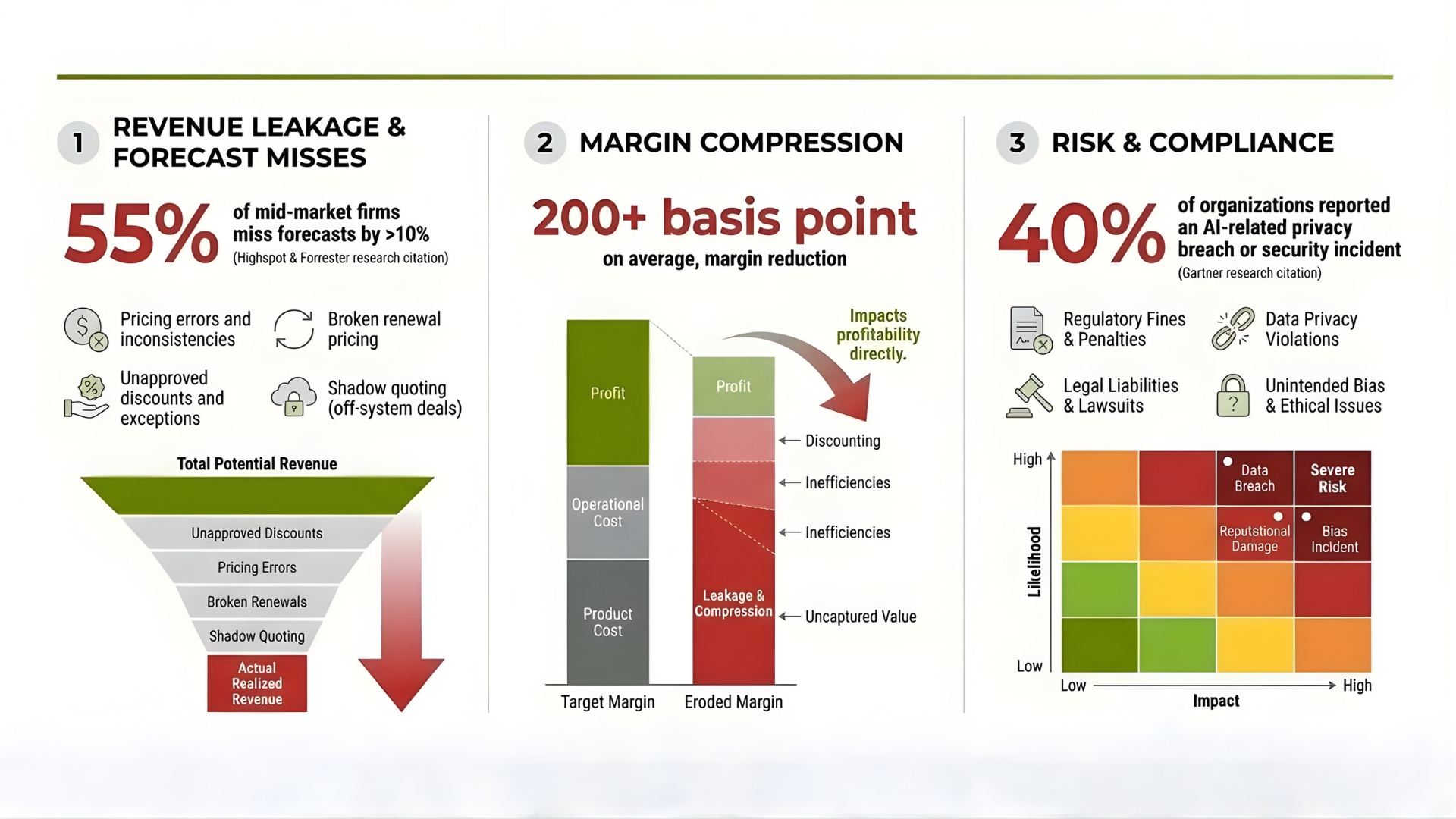

Revenue Leakage and Forecast Misses

Research from Highspot and Forrester shows 55% of mid-market firms miss their forecasts by more than 10%. Specifically, this happens often due to execution gaps in pricing and discounting.

For instance, firms without AI governance experience revenue leakage from:

- Pricing errors and inconsistencies

- Unapproved discounts and exceptions

- Broken renewal pricing

- Shadow quoting (off-system deals)

Margin Compression

Bain & Company (2025) warns that firms pursuing “business as usual” strategies could see margin declines of more than 200 basis points.

Furthermore, revenue erosion could hit 30% or more over five years. Specifically, this happens when firms fail to embed AI governance into their revenue operations.

In contrast, firms that redesign strategy around AI-driven platforms can sustain or expand margins. Additionally, they adopt value-based pricing and invest in governance.

As a result, these firms achieve 8–10% revenue growth.

Due Diligence Complexity

Currently, private equity firms and acquirers include AI governance assessments in tech due diligence.

Consequently, lack of auditable AI pricing creates:

- Extended diligence timelines

- Increased scrutiny of revenue quality

- Potential valuation adjustments

- Post-close integration challenges

Real-World Governance Wins

HPE: “Alfred” AI Platform

HPE partnered with Deloitte to build “Alfred,” an AI-powered finance platform. Notably, governance was baked in from day one.

The results included:

- 40% faster reporting cycle time

- 25% reduction in processing costs

- 90% reduction in manual effort

Why it worked: HPE didn’t bolt governance onto an existing system. Instead, they embedded human-in-the-loop controls, audit trails, and validation checkpoints at every stage. Ultimately, they treated governance as architecture, not an add-on.

McKinsey: 25,000 AI Agents at Scale

McKinsey has deployed approximately25,000 AI agents across its global operations. Notably, these agents handle roughly 40% of routine work for its 40,000+ consultants.

Every agent operates under:

- Built-in audit trails for every decision made

- Quality-control checkpoints before outputs go live to clients

- Escalation protocols for edge cases requiring human judgment

- Continuous monitoring for performance and compliance

Why it works: Governance wasn’t added after deployment. Instead, it was designed into the agent architecture from the start.

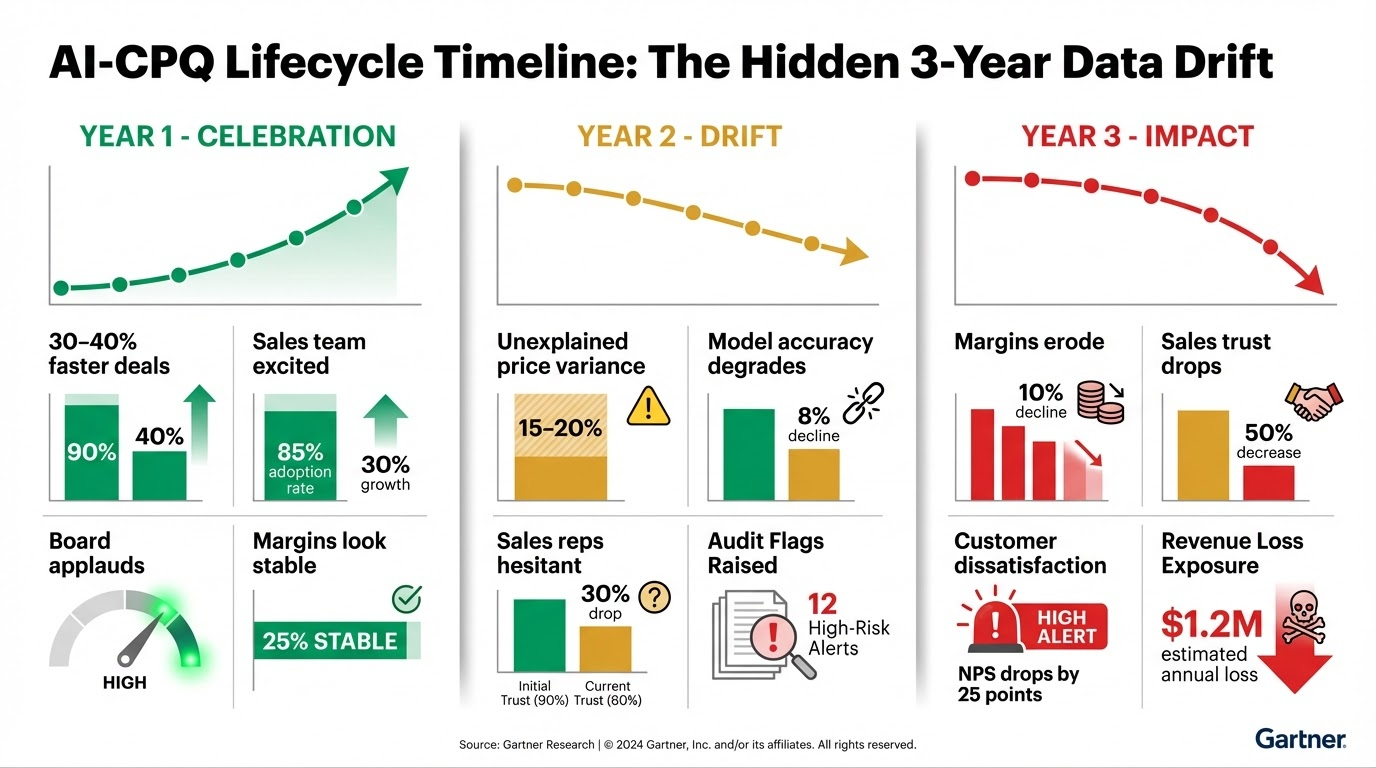

The Three-Year Pattern (And How to Avoid It)

Year 1: Velocity Gains

AI-powered CPQ delivers 30–40% faster deal velocity.

Sales teams embrace it. Early results look promising. Margin appears stable.

Year 2: Hidden Drift

Finance starts seeing unexplained price variance across similar deals.

Reps create “one-off” quotes in Excel to close deals faster.

RevOps struggles to track approvals. Manual overrides increase. Shadow quoting spreads quietly.

Year 3: Discovery

One of several triggers occurs:

- Due diligence uncovers systematic pricing gaps

- Audit flags weaknesses in revenue controls

- Customer dispute demands audit trail you can’t produce

- Board inquiry reveals margin erosion hidden in “strategic discounts”

Result: Revenue quality questions, extended remediation timelines, organizational disruption, and potential valuation impact.

Prevention: Governance built into the architecture from the start prevents the pattern from developing.

Red Flags: Audit This Week

Check your organization for these warning signs.

Importantly, if you check three or more, you have a governance gap that requires attention:

![]()

Consequently, if you can’t audit AI pricing decisions in your organization, these red flags signal immediate risk.

Why Legacy CPQ Can’t Be Retrofitted

The Fatal Assumption

Traditional CPQ was designed on three assumptions:

- Humans make the final decision (AI is only advisory)

- Approvals are sequential and deterministic (linear workflows)

- Controls are applied after the fact (audit, not prevention)

AI breaks all three assumptions:

- AI makes autonomous decisions (not just recommendations)

- Agent behavior is probabilistic and context-aware (not deterministic)

- Controls must be architectural (prevention, not detection)

The Retrofit Challenge

Retrofitting governance onto legacy CPQ creates multiple problems.

It leads to:

- Extended implementation timelines

- Partial coverage and gaps

- Technical debt accumulation

- Higher total cost of ownership

In contrast, AI-native governance platforms deliver:

- Complete coverage from day one

- Lower implementation risk

- Future-proof architecture

- Built-in compliance capabilities

Bottom line: Building governance into the foundation is faster and more effective than bolting it on afterward.

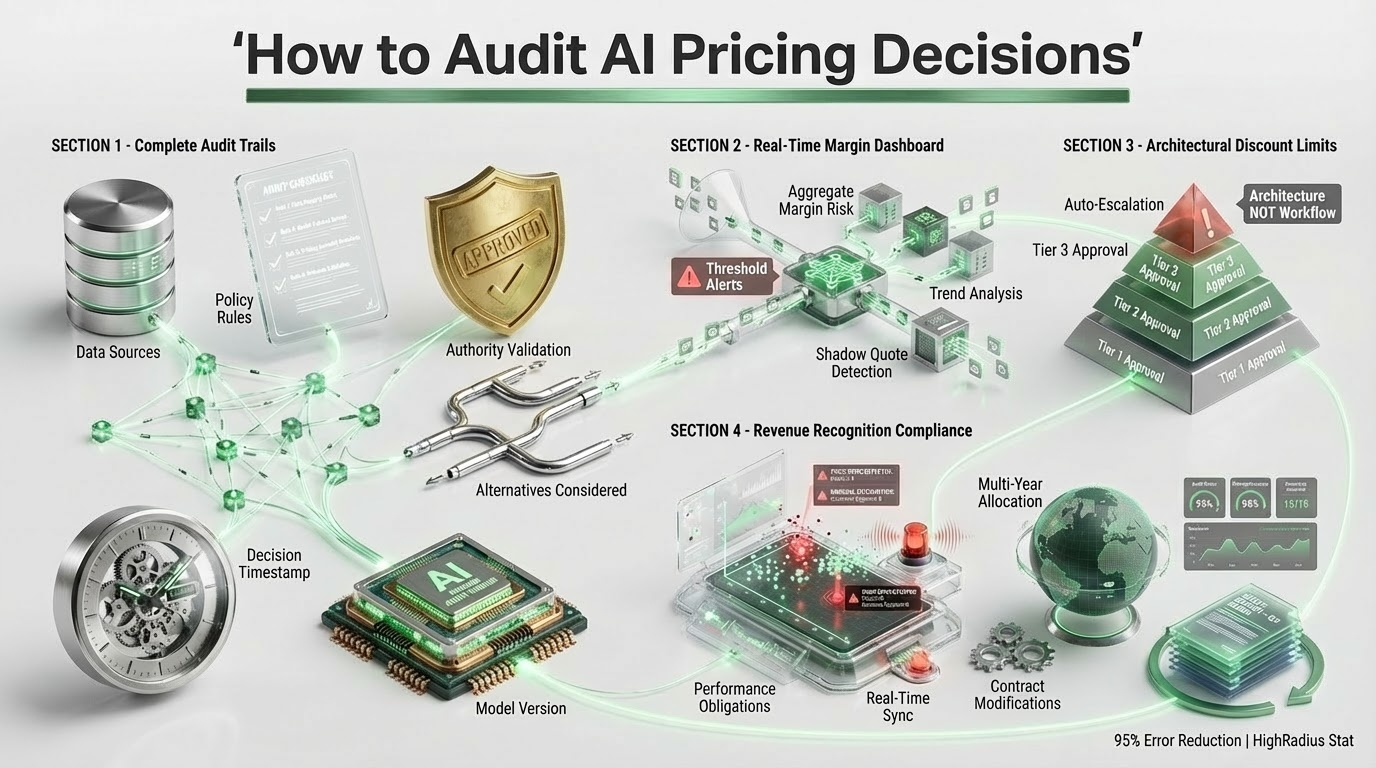

How to Audit AI Pricing Decisions: What Governance Looks Like

Complete Pricing Audit Trails

Every quote captures the following information:

- Data sources used: CRM opportunity data, ERP pricing history, external market data

- Policy rules applied: Discount matrices, margin floor thresholds, competitive positioning rules

- Authority validation: Who approved, at what discount tier, automated vs. manual

- Alternatives considered: Other pricing scenarios evaluated

- Decision timestamp: When each decision node was executed

- Model version: Which AI model version generated the recommendation

Real-Time Margin Exposure Dashboard

Finance teams see at a glance:

- Aggregate margin risk across all active quotes in the pipeline

- Deals approaching margin floor thresholds that require review

- Historical margin trends by rep, region, product line, customer segment

- Shadow quoting indicators

Architectural Discount Limits

Not workflow—architecture:

Discounts beyond approved authority cannot be entered into the system. Additionally, the system enforces tiered approval structures based on deal characteristics.

Furthermore, overrides are logged and escalated automatically. They require documented justification. Finally, unauthorized discount attempts trigger immediate alerts.

This is the difference between asking people to follow policies (workflow) and making policy violations impossible (architecture).

Embedded Revenue Recognition Compliance

ASC 606 / IFRS 15 compliance enforced at quote generation:

Multi-year revenue allocation is calculated automatically. In addition, performance obligations are validated before quote approval.

Moreover, deferred revenue schedules are generated in real time and synced to ERP. Finally, contract modifications are tracked with complete audit trail.

HighRadius research: Firms with architectural compliance reduce revenue recognition errors by 95%. Additionally, they cut monthly reconciliation time by 50%.

Shadow CPQ Detection

The system automatically flags:

- Quotes created in Excel and uploaded later

- Email-based pricing discussions that bypass CPQ workflow

- CRM notes containing pricing commitments not reflected in CPQ

- Unapproved discount codes entered manually

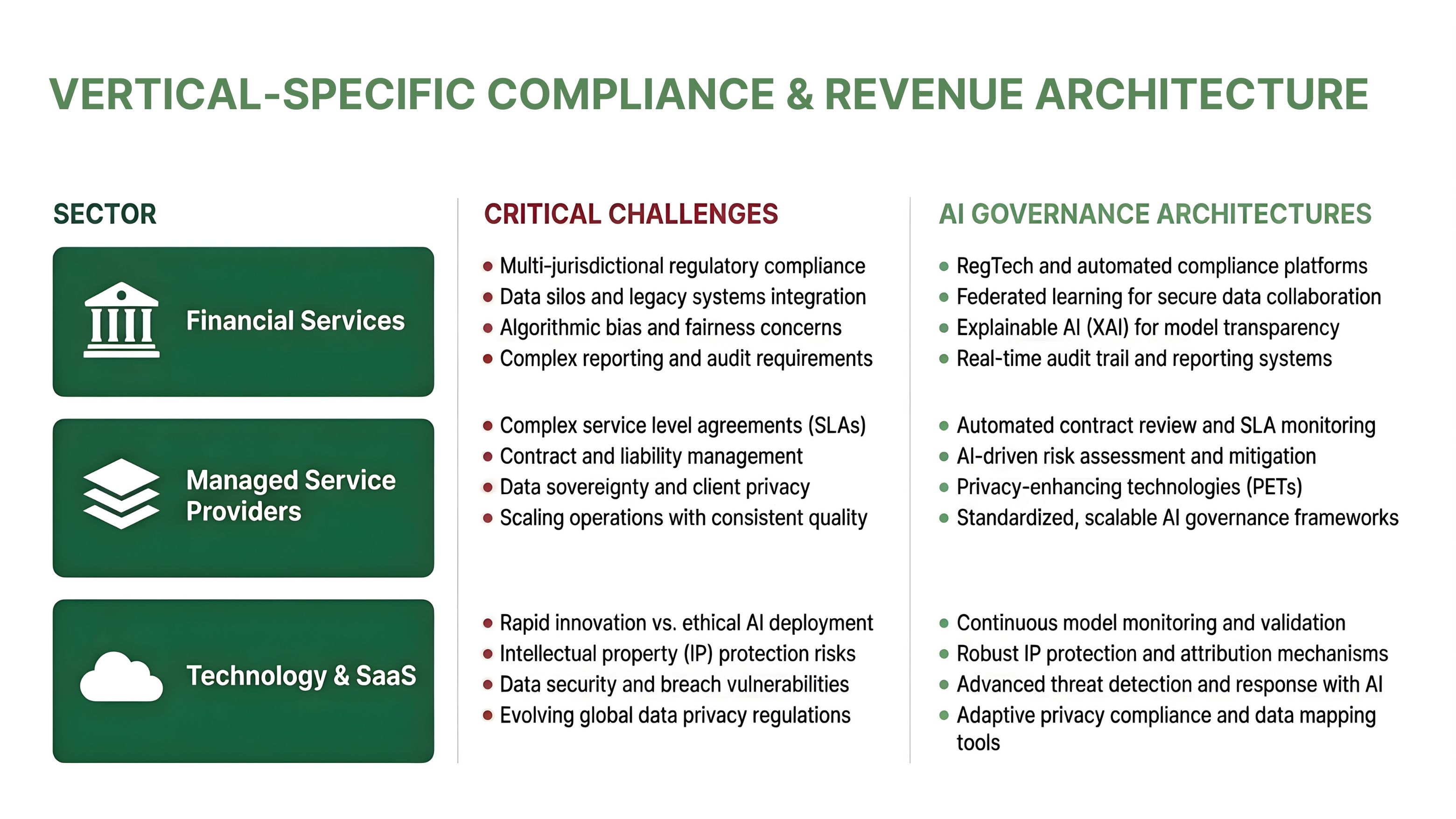

Industry-Specific Governance Imperatives

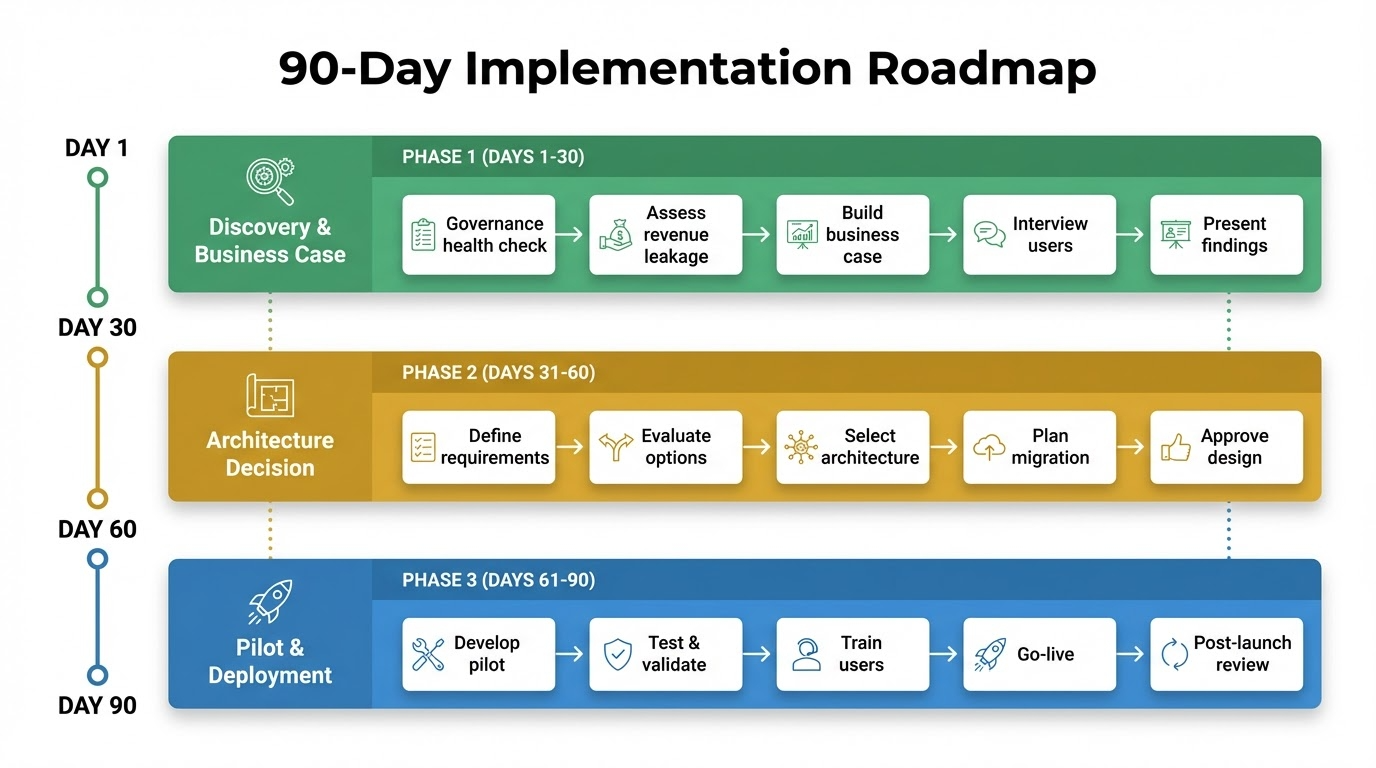

90-Day Implementation Roadmap

Implementing AI pricing governance follows a structured 90-day roadmap.

Days 1–30: Discovery & Business Case

First, run the 5-minute governance health check with CFO, CRO, and RevOps leaders. Next, assess current revenue leakage across categories: pricing errors, unapproved discounts, renewal gaps, shadow quoting.

Then, build business case covering: margin improvement potential, audit cost avoidance, compliance risk reduction. Additionally, interview frontline users to understand current pain points and workflows.

Finally, present findings to executive team with quantified business case.

Days 31–60: Architecture Decision

First, define detailed governance requirements: audit trail specifications, margin visibility needs, compliance enforcement rules.

Next, evaluate governance platform options against requirements. Then, make build-vs-buy decision based on: total cost of ownership, implementation timeline, organizational change management requirements.

Subsequently, select platform based on: proven outcomes, regulatory compliance capabilities, integration flexibility. Finally, secure board-approved implementation plan with budget and timeline.

Days 61–90: Pilot Deployment

First, deploy core audit-trail capability on high-value deals. Then, launch real-time margin exposure dashboard for finance team.

Next, enable shadow CPQ detection with reporting to RevOps. Additionally, train pilot users across sales, finance, and RevOps functions.

Subsequently, measure and document early wins: margin protection, audit time reduction, pricing dispute resolution speed. Finally, collect user feedback and refine workflows before broader rollout.

Post-90-Day Rollout

First, expand organization-wide deployment over 12–18 months. Then, integrate with existing CRM, ERP, and billing systems.

Next, implement continuous optimization based on user feedback and performance data. Finally, establish governance council for policy refinement.

KPMG Q4 2025 AI Pulse Survey: 80% of executives view cybersecurity as the greatest AI barrier. Furthermore, 72% will source agents from trusted vendors with robust governance and security.

Common Implementation Pitfalls (And How to Avoid Them)

Sales Team Resistance

Problem: Reps fear AI governance will slow deals or reduce flexibility.

Solution:

- Show reps how governance protects them when deals are questioned

- Use pilot wins to build credibility

- Involve sales leadership early as co-owners of governance design

- Demonstrate how automated approvals can actually be faster than email chains

Legacy Data Migration

Problem: Historical pricing data is messy, inconsistent, or incomplete.

Solution:

- Start with forward-looking governance rather than waiting for perfect historical data

- Use AI to normalize legacy data over time

- Set a “data quality baseline” date and enforce clean data standards going forward

- Focus on highest-value accounts first

Change Management Fatigue

Problem: Teams are overwhelmed by constant tool rollouts and process changes.

Solution:

- Embed governance into existing workflows rather than adding a new tool

- Use APIs to integrate with CRM/ERP so users stay in familiar interfaces

- Provide role-based training appropriate to each user group

- Create “champions network” of early adopters who can support peers

- Communicate clear benefits relevant to each role

Underestimating Regulatory Complexity

Problem: Financial services and regulated industries have industry-specific compliance requirements.

Solution:

- Work with platforms that have pre-built regulatory templates

- Engage legal and compliance teams early in architecture design

- Run regulatory stress test before go-live

- Map every pricing decision to relevant regulatory requirements

- Build regulatory reporting capabilities into the platform

FAQ Page: Your Four Most Critical Questions

Q1: “We have workflows and approvals. Isn’t that governance?”

Workflows can be bypassed. Architecture can’t.

Workflows are policies enforced by human discipline. For instance, reps can create quotes in Excel, get approvals over email, then upload to CPQ later for “tracking.”

In fact, real governance means you can audit AI pricing decisions end-to-end—not just approve them in a workflow.

Real governance is architectural:

First, discounts beyond approved authority cannot be entered into the system. Second, revenue recognition violations cannot be saved as valid quotes. Third, shadow quotes trigger automatic alerts to RevOps.

Think of it this way: workflows are like speed limits. In contrast, architecture is like speed governors that make speeding impossible.

Q2: “What’s the ROI timeline?”

Most firms see measurable impact within quarters, not years.

Within 90 days: Margin protection becomes visible through better pricing discipline and automated controls.

Within 6–12 months: Benefits accumulate including:

- Reduced margin leakage

- Lower audit preparation costs

- Faster deal cycles through automated approvals

- Reduced RevOps manual work

KPMG’s 2025 AI Pulse Survey shows 76% of executives are willing to pay a 10% premium for AI-skilled talent and governance-ready platforms. Consequently, this reflects growing recognition of governance value.

Q3: “What if we’re planning to exit soon? Is governance worth it?”

Governance has become a standard due-diligence item.

Currently, private equity firms and acquirers include AI governance assessments in tech due diligence.

For example, firms with audit-ready AI pricing face:

- Smoother diligence processes

- Faster deal timelines

- Stronger negotiating position

- Lower integration risk perception

In contrast, those without governance face:

- Extended diligence timelines

- Increased scrutiny of revenue quality

- Potential valuation adjustments

- Post-close remediation requirements

Bottom line: If you’re exiting in 12–24 months, you need governance operational with clean trailing data for diligence. Specifically, start now, not months before you go to market.

Q4: “How does this integrate with our existing tech stack?”

AI-native governance platforms integrate via APIs—you don’t rip and replace.

Integration approach:

- CRM (Salesforce, HubSpot): Bi-directional sync so reps stay in familiar interface

- ERP (NetSuite, SAP, Oracle): Real-time data exchange for product catalogs, cost data, margin calculations

- Billing systems (Zuora, Stripe): Automated handoff of approved quotes with complete audit trail

What users experience:

First, sales reps work in Salesforce (familiar interface). Meanwhile, governance engine runs in background.

Additionally, approvals are automated and faster. Finally, finance gets clean data in ERP without manual reconciliation.

About servicePath™

servicePath™ is building the trust infrastructure for AI-native revenue operations.

Purpose-built for complex enterprise quoting, pricing, and revenue lifecycle management, servicePath™ delivers the governance architecture that modern commercial organizations require as AI transforms every dimension of the quote-to-cash process.

What Makes servicePath™ Different

Unlike legacy CPQ platforms that bolt AI features onto existing workflows, servicePath™ embeds governance at the architectural level—not as an afterthought, but as a core platform capability.

Core Capabilities:

- Complete audit trails: Data sources, policy logic, approvals, confidence scores

- Architectural guardrails: Discount limits and compliance rules enforced by design

- Real-time margin protection: Finance dashboards with live exposure visibility

- Embedded compliance: SOX, SOC 2 compliance and enforcement at quote generation

- Shadow CPQ detection: Automatic alerts for off-system pricing

- Deterministic replay: Reconstruct any pricing decision with full audit trail

Who We Serve

servicePath™ serves enterprise customers across industries where commercial precision, regulatory compliance, and revenue integrity are non-negotiable:

- Financial services firms navigating SOX, MiFID II, and Basel III requirements

- Managed service providers protecting multi-year contract margins from erosion

- Technology and SaaS companies scaling complex, usage-based pricing models

- Private equity-backed consolidators requiring cross-portfolio revenue governance

Learn more: servicepath.co

Take Action: Don’t Wait for the Board to Ask

The governance gap isn’t a technology problem—it’s a business risk. Here’s how to address it.

Step 1: Assess Your Governance Readiness

Answer these five critical questions honestly:

- Can you reconstruct any pricing decision from the past 12 months with complete audit trails?

- Do you have real-time visibility into margin exposure across all active deals?

- Are your discount controls architectural—or just workflow-based?

- Can you detect and prevent shadow quoting (Excel, email, off-system pricing)?

- Is your organization audit-ready for PE diligence, SOX review, or regulatory inquiry?

If you answered “no” or “partially” to two or more questions, your governance architecture has material gaps that will surface during the next board review, audit, or deal.

Step 2: See AI-Native Governance in Action

Watch us reconstruct a deal’s complete pricing decision—data sources, policy logic, approvals, alternatives—with full audit trail capabilities.

Step 3: Review Industry-Specific Governance Outcomes

See how financial services, MSPs, and SaaS companies achieved audit-ready AI governance and recovered margin leakage.

Explore Governance Case Studies →

Step 4: Master the Language of AI Governance

Understand the critical terms—audit trails, architectural controls, shadow CPQ, deterministic replay—that define modern revenue governance.

Review the AI Governance Glossary →

Step 5: Deepen Your Strategic Understanding

Explore why audit trails are becoming a competitive requirement and what PE firms now evaluate in revenue governance.

Start with the 5-Minute Health Check

Not ready for a full assessment? Start by completing the 5-Minute Governance Health Check at the top of this article and share your score with your CFO, CRO, and RevOps leadership.

Score 0–2? Immediate action required—governance gaps are material.

Score 3–5? Moderate risk—start planning upgrades now.

Score 6–8? You’re ahead of most—but don’t stop investing.

The board will ask. The auditors will ask. Buyers will ask.

Be ready to answer.

Appendix: AI Bias and Legal Risk

Q: “What about AI bias and discrimination? Can this create legal risk?”

Yes—and that’s exactly why you need governance with built-in monitoring and explainability.

The legal risk is real:

- U.S. Equal Credit Opportunity Act (ECOA) prohibits price discrimination based on protected characteristics

- EU AI Act (2024) requires explainability for high-risk AI systems

- State-level laws are expanding algorithmic accountability requirements

What unauditable AI creates:

- Litigation exposure: If AI varies prices systematically, you can’t prove it wasn’t discriminatory

- Regulatory risk: Auditors ask “How do you know your AI isn’t biased?” with no answer

- Reputational damage: Public disclosure of discriminatory pricing destroys trust

What AI-native governance provides:

- Bias monitoring: Continuous tracking of systematic price variance across customer segments

- Explainability: Complete audit trail showing data inputs, policy rules, business logic

- Human oversight: Architectural controls requiring human review of edge cases

- Litigation readiness: Defensible documentation if pricing is challenged

All statistics and case studies in this article are sourced from publicly available research:

- Bain & Company (2025)

- McKinsey State of AI (2025)

- Goldman Sachs Research (2025)

- Gartner Strategic Predictions

- Forrester B2B Revenue Operations (2024)

- KPMG AI Pulse Survey (Q4 2025)

- Deloitte CFO Signals (Q4 2025)

- HighRadius Revenue Recognition Research (2025)

- Fortune on HPE AI Platform (2026)

- Business Insider on McKinsey AI Agents (2026)

- Highspot Revenue Operations Research