Annual Infra/STRUCTURE Summit 2022

NETWORK – LEARN – GET THINGS DONE

The only constant is change.

servicePath™ is looking forward to seeing you on September 14th and 15th, when executives from across the Internet infrastructure ecosystem – cloud, data center, edge and managed hosting – will be coming together under one roof to talk about what’s what. We are looking forward to expanding our networks and talking about the industry’s status and future directions. Attendees can interact with EXECUTIVES OPERATING INFRASTRUCTURE SERVICE PROVIDERS like from Amazon Web Services, Data Bank and many more, EXECUTIVES OPERATING MSPs, VARs including Centrilogic and Ingram, EXECUTIVES OPERATING EDGE PROVIDERS like Lumen Technologies and American Tower, and EXECUTIVES OPERATING INTERCONNECTION PLATFORMS including Ciena and Epsilon, and many many more tech companies.

We’ve already established and are nonetheless constantly reminded that the only constant is change. The past decade has seen the most phenomenal innovation that has transformed our lives.

Hyperscale, cloud, data centers and edge are the present, and the future.

AGENDA:

On Day 1 of the event, attendees will be briefed about SR’s proprietary marketshare numbers and new hyperscale data center self-build tracker, along with a data-heavy look at their deep-dive research into select APAC markets. They will also be included in discussions on where the next tier of hyperscale markets is coming from around the world, particularly Latin America; with analysts from SR and Chief Executives of Layer 9 Data Centers and Transwesters. Next we’ll be meeting with the buyers of data center colocation – a conversation with Cloudflare’s head of data center strategy. They’ll be answering questions around the challenges of buying colocation for an infrastructure provider with global scope and on the verge of a next chapter that looks like hyperscale. 5:00 – 5:30 pm then we’ll be taking a look at the Canadian Market; finding answers to questions like ‘What is the state of the data center market in Canada? How is hyperscale driving it? Where are the new opportunities both geographically and product-wise?’

In Room L3, the attendees will be talking about New edge strategies and deployment models; all things Edge. Senior Analyst SR will be providing a data-oriented overview of SR’s deep-dive research into select Canadian markets, highlighted by new data on Western Canada. Next we will be meeting with Head of Edge Infrastructure and Digital Services GTM Leader at Equinix who will be talking about how edge drove the evolution of Equinix; from colocation to interconnection to digital infrastructure services.

Executives will be answering questions like is the industry progressing when it comes to micro builds at the edge? Is it the location or the workload that is driving things? What is driving connectivity needs at the edge? What are the challenges in building ecosystems in edge locations? On day 1, attendees will be presented with real information about the actual edge scenarios from around the world. Managing Director SR will then be presenting an overview of SR’s proprietary marketshare data numbers spanning the entire ecosystem from colocation to hyperscale to managed infrastructure services.

Executives will be addressing the audience and answering questions related to Cloud in Room L4. Workforce reductions, talent shortages and constant upskilling requires insight and management. Hear ideas on how to solve these challenges from an industry veteran. How has M&A changed with the rise of public cloud? Is there an end on the horizon for consolidation or where is it shifting to? CEO Corero will be highlighting trends in DDoS Services for Hyperscalers, DC Operators, Managed Cloud, Alternate Cloud, Edge and Infrastructure, combined with real-world business models for successful DDoS Services roll-outs. More on how the future of cloud is alternative cloud – quicker to deploy, easier to use, more cost-effective and delivered at the edge by local CSPs and MSPs. In this session, we’ll look at what’s driving the alternative cloud market; how service providers are already benefiting from 35% CAGR for alternative cloud services; how 50% margin is an attainable target for alternative cloud providers; and how collectively, the world’s CSPs and MSPs can deliver Anything-as-a-Service at the edge to provide a more compelling alternative to the hyperscalers. Chief executives from Opus Interactive, Ntirety and Otava will be talking about the evolution of MSP and managed infrastructure market. How does demand look as we move out of the peak pandemic phase? What are the products and services that are seeing success and what is in decline? Some other points of discussion: What will the next wave of M&A look like? What is the state of cloud adoption in Canada and where is it headed?

Day 2 will be all about Hyperscale.

Hyperscale continues to shape the Internet infrastructure landscape and there are no signs of things slowing down any time soon. Hyperscale is consuming colocation in different models, while capacity requirements continue to climb. But it is not all tailwinds. Self-building by hyperscalers could shift the demand profile in certain geographies. Head of Research Jabez Tan presents new self-build statistics, assesses the demand environment and analyzes the various dynamics in play around data center colocation leasing.

In its short history, the M&A sector has been through three disruptive events: the dotcom bubble, the global financial crisis and the COVID-19 pandemic. Each time the sector emerged stronger than before. Internet infrastructure pushed through the pandemic successfully and there are signs that secular tailwinds and growth are accelerating, despite supply chain disruption, an uncertain macroeconomic environment and geopolitical events. Structure Research MD Philbert Shih, in collaboration with Cornerstone Sponsor DH Capital, identifies why the conditions are there for acceleration and provides a temperature check and outlook, while assessing the implications for M&A.

Head of Research SR will be heading the discussion about how serving hyperscale requirements requires a whole new mindset and operating model. What are the challenges and pitfalls and are they consistent on a global basis? What is the state of the lease versus build dynamic? What are hyperscalers looking for from their data center partners?

Next, more on M&A – The pandemic did not slow M&A activity. Capital continued to flow into the sector and new strategic acquirers emerged. Strategic activity has shifted as a result of the long-term horizon and global expansion of hyperscale. Meanwhile, the ecosystem around managed services is flourishing and driving M&A as well. What is the outlook for the rest of 2022 and on?

Speakers will then be talking about how Public cloud is taking an increasingly larger share of the computing infrastructure pie. This session will assess the status of the asset-light revolution and explore where the opportunities are and how MSPs and service providers can tap into it. INFRASTRUCTURE IS DEAD. LONG LIVE …?

Head of Research SR will then talk be discussing amongst the panelists how Colocation has reached a turning point as separation in the market becomes clearer with the panelists. While growth is slowing in certain pockets, other segments are increasingly dynamic. How do we reconcile this and what is the future going to look like?

Managing Director SR and panelists will be answering the big question: WHERE IS THE MONEY HEADED? Hyperscale has created separation in investment circles. But at the same time, decentralization and convergence is expanding the ecosystem and creating new opportunities. Where is the capital headed in this shifting landscape and why?

Next, Head of Research SR along with panelists will be shedding light on how hyperscale expansion and edge builds have made the data center business global. Maturation in the US has made Europe and Asia more strategic. Where are the next frontiers? What are some of the challenges of geopolitics and operating in mutliple jurisdictions? What strategic choices are on the table for operators?

We are aware that network capacity requirements are skyrocketing and interconnection is increasingly at the heart of all computing architectures as end users try to figure out how to move between core and edge. How are operators responding to this challenge and how is hyperscale changing the game?

Hyperscale leads the way, but there is always going to be diversity when it comes to infrastructure. What does that diversity look like and what is driving end users? What is the opportunity for operators and how will the landscape evolve going forward?

The rise of hyperscale has defined the industry for the better part of the last decade. In many parts of the world, it is still early in the game. But when it comes to some of the most developed markets, the next stage of hyperscale expansion – with planning time horizons pushing to a decade and longer – is well underway. The network and compute requirements are pushing to another level and we preview what is in store and already in development.

The event ends at 3:30 with Analyst Keynote. Managing Director SR Philbert will be closing by sharing some more relevant Internet infrastructure numbers.

We are looking forward to meeting, sharing ideas with and learning from experts from the service providers’ industry.

Let us know if you’re attending so that we can chitchat!

You may be interested in these articles next

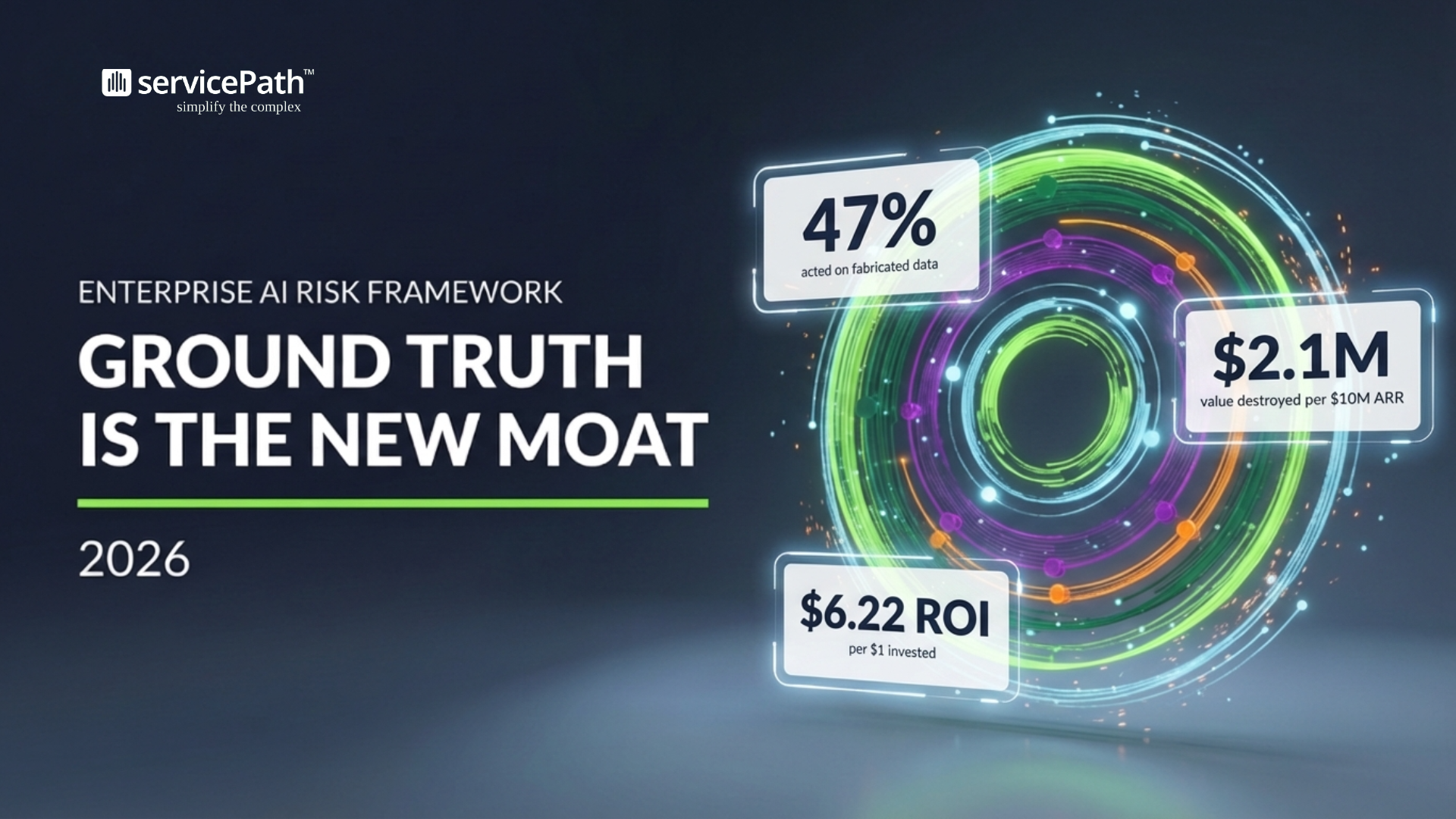

Ground Truth Is the New Moat | CPQ AI Risk Framework 2026

Salesforce CPQ End of Sale: enjoy the rest of summer, but decide before fall planning locks.

The vanity of velocity: speed to quote and the Iteration Toll